Imperial Oil's Q1 2026 Results Reflect Market Volatility and Strategic Investment in Low-Emission Technologies

Imperial Oil reported Q1 financials below estimates, underscoring commodity price pressures and regulatory costs alongside progress in oil sands development and energy transition initiatives.

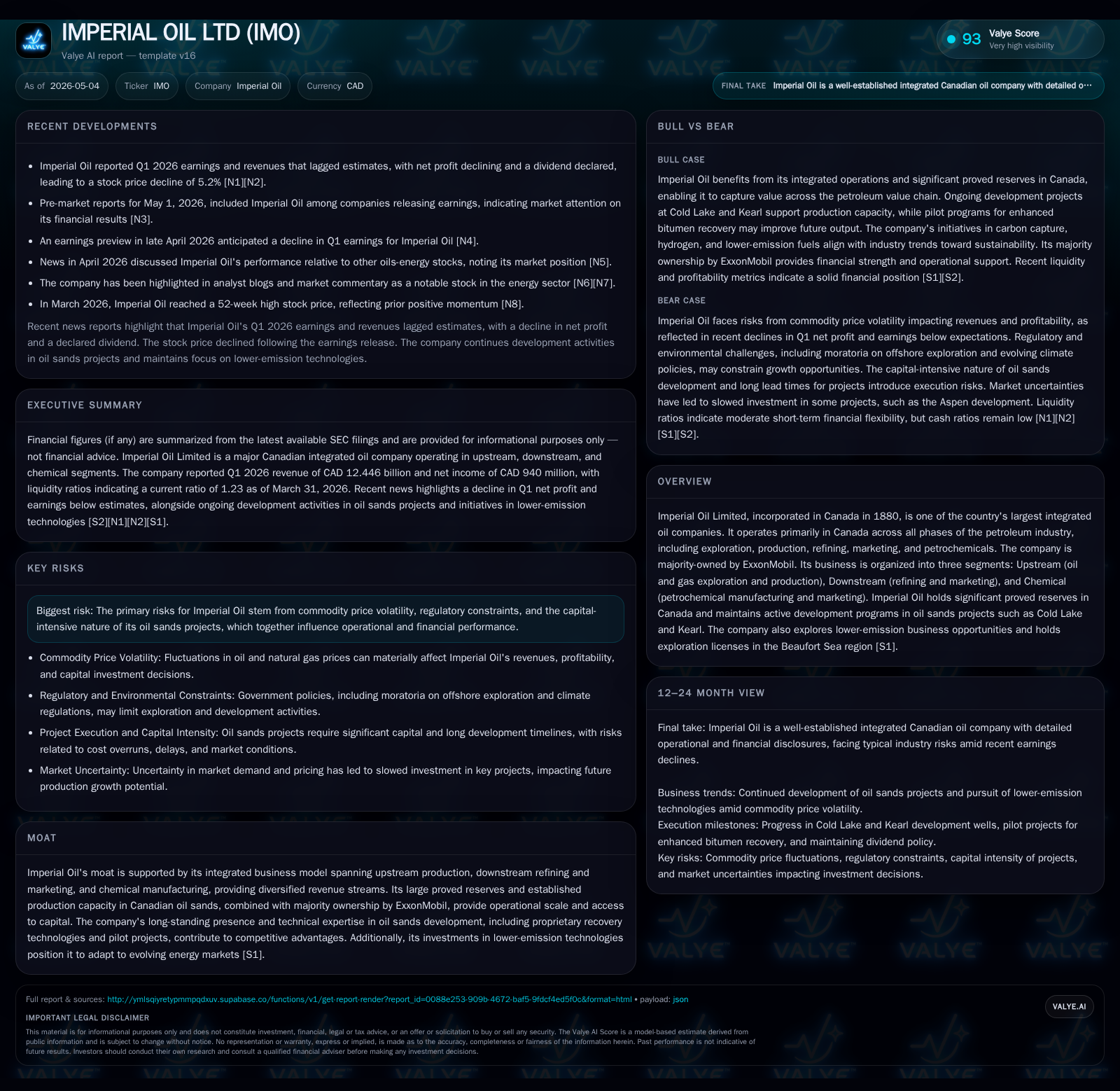

In its latest 10-Q filing for Q1 2026, Imperial Oil Ltd faced revenue and earnings softer than anticipated amid a challenging commodity price environment and inflationary cost pressures. The company continues to lean on its integrated operating model with strong footholds in Canadian oil sands production, refining, and chemicals segments. It is advancing investments in environmental protection and lower-emission technologies, including carbon capture, hydrogen, and lithium projects. However, regulatory constraints, especially around production limits and environmental compliance, remain key risk factors. The firm's robust asset base supported by ExxonMobil’s majority ownership provides scale, but near-term earnings will fluctuate with market dynamics and government policies affecting the Canadian energy sector.

Recent Operating Update

Imperial Oil's first quarter 2026 results disclosed in the May 4th 10-Q reveal a modest miss on both revenues and earnings relative to market estimates [S2][N1]. The company cited a challenging pricing environment marked by crude oil volatility alongside inflation-driven increases in operating expenses. Despite these pressures, Imperial continued steady production at its Canadian oil sands assets like Cold Lake and Kearl while also advancing capital investments targeting emissions reduction technologies. Press coverage also highlights a modest share price reaction following the earnings release indicating cautious investor sentiment [N6]. This quarterly disclosure provides the primary lens to assess Imperial's near-term operational resilience before considering broader annual strategic context from its February 2026 Form 10-K [S1].

Business Model

Imperial Oil operates as one of Canada's largest integrated oil companies with operations spanning upstream exploration and production (notably heavy crude oil from oil sands), downstream refining and marketing of petroleum products, and chemical manufacturing via its petrochemicals segment [S1]. Its upstream portfolio centers primarily on bitumen extraction from established sites such as Cold Lake and Kearl—with synthetic crude conversion capabilities that enhance product value.

Revenues derive largely from crude oil sales priced against international benchmarks but converted into Canadian dollars; this currency exposure can add volatility to reported financials [S20]. Downstream operations earn margins through refining capacity utilization, product blending, distribution networks, and branded marketing—a segment crucial for capturing value beyond raw hydrocarbon extraction. Chemical segment revenues stem from petrochemical product manufacturing designed for plastics and industrial feedstocks.

The integrated nature provides diversification across commodity cycles; however, the upstream division remains capital intensive with upfront expenditures for extraction technologies suited to Canada's unique oil sands geology. Long-term competitiveness benefits from proprietary recovery methods developed over decades alongside ExxonMobil's ownership providing technological and financial support [S1].

Industry Structure and Competitive Position

Imperial occupies a strategic position within the Canadian petroleum value chain as a major producer, refiner, marketer, and petrochemical manufacturer. The Canadian upstream sector is regulated tightly by provincial governments imposing production quotas or curtailments during periods of oversupply to stabilize markets—a factor that affected Imperial historically though curtailments were repealed in Alberta at the end of 2021 [S28]. Export controls further necessitate federal approval for long-term contracts affecting supply flexibility.

Competitively, Imperial benefits from significant reserve bases—net proved reserves surpassing two billion barrels of oil equivalent—and longstanding operational expertise in oil sands development. These assets create substantial barriers to entry given high capital intensity, technology complexity, environmental compliance demands, and Indigenous community engagement requirements [S1][S28].

However, emerging competition arises not only from other Canadian producers but increasingly from alternative energy providers supported by government incentives that challenge hydrocarbon demand growth [S21]. Additionally, global energy transition pressures introduce competitive risks related to carbon-intensive operations typical of oil sands.

Growth Drivers

Key growth levers include:

- Development of Oil Sands Reserves: Ongoing investment at Cold Lake and Kearl projects aims to sustain or increase bitumen output leveraging proprietary enhanced recovery methods enhancing resource recovery rates [S1].

- Downstream Margin Expansion: Refining capacity optimization coupled with marketing strategies targeting Canadian fuel demand supports stable cash flows less sensitive to upstream commodity swings.

- Petrochemical Expansion: Focus on higher-value chemical products aligned with growing markets for plastics alternatives may diversify revenue streams.

- Lower-Emission Initiatives: Substantial capital allocation (~$2 billion forecasted environmental expenditures in 2026) directed at carbon capture projects, hydrogen production capabilities, lower-emission fuels introduction (e.g., renewable diesel blending), and lithium mining/distribution signals a strategic pivot anticipating decarbonization trends [S28][S20].

- Operational Efficiency Gains: Management emphasizes controlling costs amid inflationary environments including supply chain optimization.

These elements together aim to balance traditional oil business risks against emerging opportunities within evolving energy landscapes.

Risks and Watchpoints

- Commodity Price Volatility: Fluctuations in global crude prices remain the foremost financial risk impacting revenues directly given price-indexed contracts [S14].

- Regulatory Constraints: Alberta’s past use of production curtailment authority—albeit currently repealed—alongside federal export licensing requirements creates operational flexibility uncertainty. Accelerating environmental regulations around tailings management and carbon emissions add cost burdens [S19][S28].

- Capital Intensity & Cost Inflation: Oil sands projects require substantial upfront investment with long payback periods; inflationary pressures erode margins if not offset adequately [S7][N1].

- Competitive Threats from Energy Transition: Growing adoption of renewables and electrification policies challenge fossil fuel demand forecasts reducing long-term reserve valuations [S21].

- Environmental & Social Governance Risks: Litigation or public opposition related to greenhouse gas emissions profiles or Indigenous land rights pose reputational and project risk factors [S11][S29].

- Currency Exposure: Majority of commodity pricing benchmarks are USD-denominated whereas Imperial reports in CAD exposing it to exchange rate swings negatively affecting reported earnings [S20].

What to Watch Next

- Monitoring Alberta provincial policies for any return or modification of production curtailment mechanisms remains imperative due to their direct impact on volume realizations.

- Advancement timelines for low-emission technology deployment such as commercial-scale carbon capture projects or hydrogen facility expansions will serve as KPIs regarding strategic evolution.

- Pipeline capacity announcements especially related to exports influence marketing access conditions impacting realized pricing differentials.

- Quarterly updates on operating expenses vis-à-vis inflationary trajectories will reveal cost-control effectiveness.

- Regulatory approvals for new or expanded exploration/development leases particularly in sensitive regions like the Beaufort Sea could signal growth opportunities or hurdles.

Financial Profile (Q1 2026 Snapshot)

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | 1,029,000,000 CAD | |

| 2026-03-31 | ||

| Total debt | 3,974,000,000 CAD | |

| 2026-03-31 | ||

| Net debt | 2,945,000,000 CAD | |

| 2026-03-31 | ||

| Current assets | 11,519,000,000 CAD | |

| 2026-03-31 | ||

| Current liabilities | 9,348,000,000 CAD | |

| 2026-03-31 | ||

| Current ratio | 1.23x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

As of March 31st, 2026 Imperial Oil demonstrated solid liquidity metrics supportive of ongoing capital programs:

| Metric | Value (CAD) | Period End |

|---|---|---|

| Cash & Equivalents | $1.03 billion | |

| 2026-03-31 | ||

| Total Debt | $3.97 billion | |

| 2026-03-31 | ||

| Net Debt | $2.95 billion | |

| 2026-03-31 | ||

| Current Assets | $11.52 billion | |

| 2026-03-31 | ||

| Current Liabilities | $9.35 billion | |

| 2026-03-31 | ||

| Current Ratio | 1.23 | |

| 2026-03-31 |

The net debt level remains manageable relative to asset base given the company’s scale while the current ratio above one indicates coverage capacity for short-term liabilities without liquidity stress [F1][S2]. Capital investments continue accompanied by strategic dividend payments reflecting stable cash flow expectations despite near-term market headwinds.

Conclusion

Imperial Oil retains a structurally strong position through its integrated business model bolstered by Canada’s sizable oil sands resources. The recent quarterly results underscore ongoing challenges notably from price volatility and rising costs but also reaffirm commitment towards sustainability-oriented technology integration that could support resilience over longer time horizons. Regulatory environments will continue shaping operational latitude while commodity markets dictate financial outcomes near term. Investors monitoring Imperial should focus on execution against decarbonization goals alongside traditional performance metrics as indicative markers of adaptive capacity within an evolving industry landscape.

This analysis is based on publicly filed SEC documents including the Q1 2026 Form 10-Q (May 4), recent Form 8-K filings (May 1), annual Form 10-K (February 18), supplemented by market news reports dated April-May 2026. All financial figures cited are supported by respective filings or companyfacts as indicated.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments