Summit Hotel Properties’ Revenue Stall and Strategic Financial Controls in 2025

Summit Hotel Properties maintained near flat revenue in 2025 while managing declining operating income through disciplined covenant compliance and capital allocation.

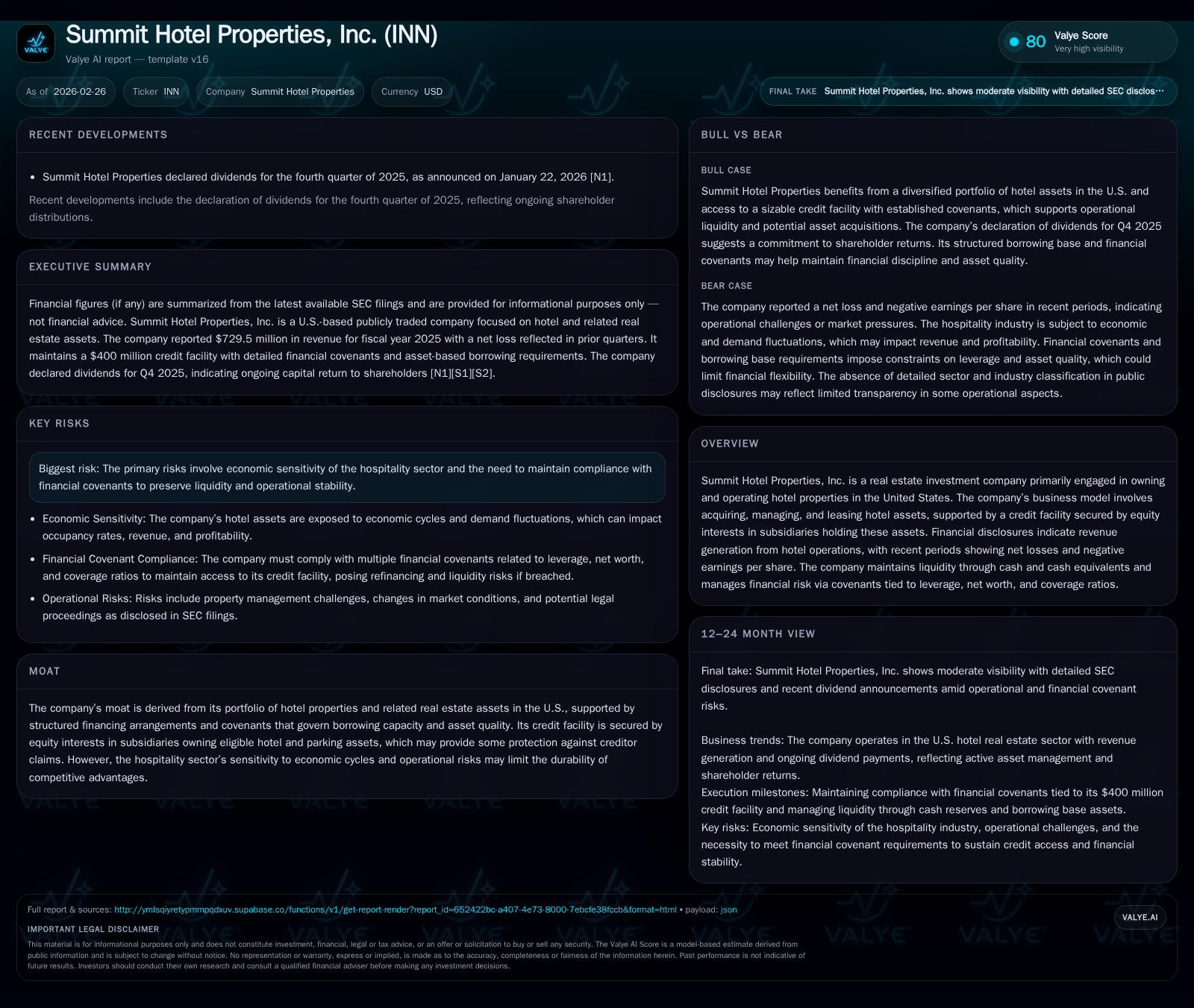

In fiscal year 2025, Summit Hotel Properties reported revenues of approximately $729.5 million, a slight decline of 0.3% versus 2024, while operating income decreased by 36.5%, reflecting margin pressures amid a challenging hospitality environment [F1]. The company’s portfolio consists primarily of leased U.S.-based hotel properties secured as borrowing base assets under a $400 million credit facility maturing in 2028, with strict covenants that reinforce financial discipline [S4][S7]. Despite negative net income trends in prior years, Summit sustained positive operating cash flows exceeding $149 million and declared dividends in Q4 2025 [F1][N1]. Capital expenditures remain minimal relative to cash flow generation [F1]. Key considerations include covenant compliance, refinancing strategies around term loan maturity, and monitoring hospitality market recovery metrics such as occupancy and average daily rate trends.

Revenue and Operating Income: Trends Reflecting Market Dynamics

Historical performance (annual)

| FY | Rev ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY |

|---|---|---|---|---|

| 2025 | 729 | 149 | 66 | -0.3% |

| 2024 | 732 | 166 | 103 | -0.6% |

| 2023 | 736 | 154 | 59 | +8.9% |

| 2022 | 676 | 170 | 68 |

Source: SEC companyfacts cache [F1].

Summit Hotel Properties reported revenues for fiscal year (FY) 2025 of approximately $729.5 million, representing a marginal decline of about 0.3% from the prior year’s $731.8 million [F1]. This near-stagnation reflects a mature portfolio facing limited top-line growth amid prevailing economic conditions impacting the hospitality industry.

Operating income contracted significantly to approximately $65.7 million in FY2025 from $103.5 million the previous year — a decrease of about 36.5% [F1]. The divergence between stable revenues and falling operating profits suggests margin pressure likely due to increased operational costs or downward lease yield adjustments inherent in Summit's leasing structure. Inflationary pressures on labor, utilities, and maintenance expenses may have further compressed margins.

Portfolio Composition and Leasing Model: Foundations of Stability

Summit's business model centers on owning a diversified portfolio of U.S.-based hotel properties leased to third-party operators through taxable REIT subsidiaries (TRS) [S4][S7][S11]. These TRS entities operate the hotels, insulating property ownership from direct operational risks while generating predictable lease income streams.

The company's $400 million credit facility is secured primarily by equity interests in subsidiaries holding eligible hotel assets—referred to as borrowing base assets—which must meet criteria including U.S. location, lack of liens or material defects, and leasing under approved operators [S4][S7]. This borrowing base underpins lending capacity and imposes discipline on asset quality.

While this leasing approach provides stability by decoupling ownership from direct hotel operations risk, it also limits upside during favorable market cycles due to fixed contractual rents.

Financial Covenant Compliance: Maintaining Leverage Discipline

Summit is bound by stringent financial covenants designed to safeguard liquidity and creditworthiness amid market fluctuations [S4][S12][S14]. These include:

- Maximum leverage ratio capped at 55%

- Minimum consolidated fixed charge coverage ratio of 1.50x

- Secured indebtedness limited to no more than 40% of total asset value

- Borrowing base asset utilization capped at 55%

Additionally, minimum tangible net worth requirements plus unencumbered net operating income thresholds help ensure lender protections are maintained [S4]. Compliance with these covenants is critical for continued access to liquidity and debt service capability.

Liquidity Profile and Capital Structure: Credit Facility Details

The company's principal debt instrument is a $400 million term loan initiated in July 2025 with maturity set for July 24, 2028, extendable up to two years subject to conditions [S7][S13]. Interest rates float based on daily or term SOFR with floors plus margins ranging from approximately 1.35% to 2.35%, consistent with current credit market conditions.

An accordion feature allows Summit to increase borrowings up to $600 million if financial covenants and asset eligibility requirements are met [S7].

At December 31, 2025, Summit held about $36.1 million in cash and equivalents alongside strong operating cash flow exceeding $149 million despite reduced operating profits [F1]. Capital expenditures remain low relative to cash flow generation historically [F1], supporting free cash flow availability.

Dividend Policy: Shareholder Returns Amid Earnings Volatility

Despite historical net losses reported in recent years [F1], Summit declared dividends for Q4 2025 as announced in January 2026 [N1]. This reflects the REIT sector norm where dividends prioritize cash flow availability over accounting earnings impacted by depreciation and non-cash charges.

The ability to sustain dividends amid earnings volatility underscores strong underlying cash generation but raises questions about long-term dividend growth absent improved profitability or portfolio enhancements.

Outlook and Risk Factors: Navigating Market Cyclicality and Refinancing Needs

Company disclosures highlight risks related primarily to cyclical sensitivity of hotel demand driven by macroeconomic factors such as recessions or travel disruptions [S5][S6][S8]. Geographic concentration within borrowing base assets adds portfolio risk requiring ongoing diversification efforts.

Covenant constraints on leverage and secured indebtedness limit aggressive growth via acquisitions or higher leverage usage [S4]. Adjustments to borrowing base asset composition remain strategic levers influencing growth potential.

Refinancing the term loan upon maturity in mid-2028 presents both challenges and opportunities dependent on interest rate environments and capital markets appetite for hospitality-backed debt.

Key Monitoring Points Moving Forward

Although no formal forward guidance has been provided [N1], stakeholders should closely monitor:

- Hotel occupancy rates and average daily rates influencing lease revenue sustainability;

- Refinancing progress related to the term loan maturing in July 2028;

- Covenant compliance trends amid shifting asset valuations;

- Broader hospitality market recovery dynamics that could relieve margin pressures observed through FY2025.

These factors will shape Summit's path toward restoring growth momentum balanced with measured financial discipline.

Disclaimer: This analysis is based solely on publicly available filings and disclosures from Summit Hotel Properties as of February 26, 2026. It does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments