Intuit Streamlines Operations with AI Restructuring and Maintains Strong Financial Base

Latest quarter highlights Intuit’s strategic workforce reduction and continued focus on AI-driven growth within its established financial software ecosystem.

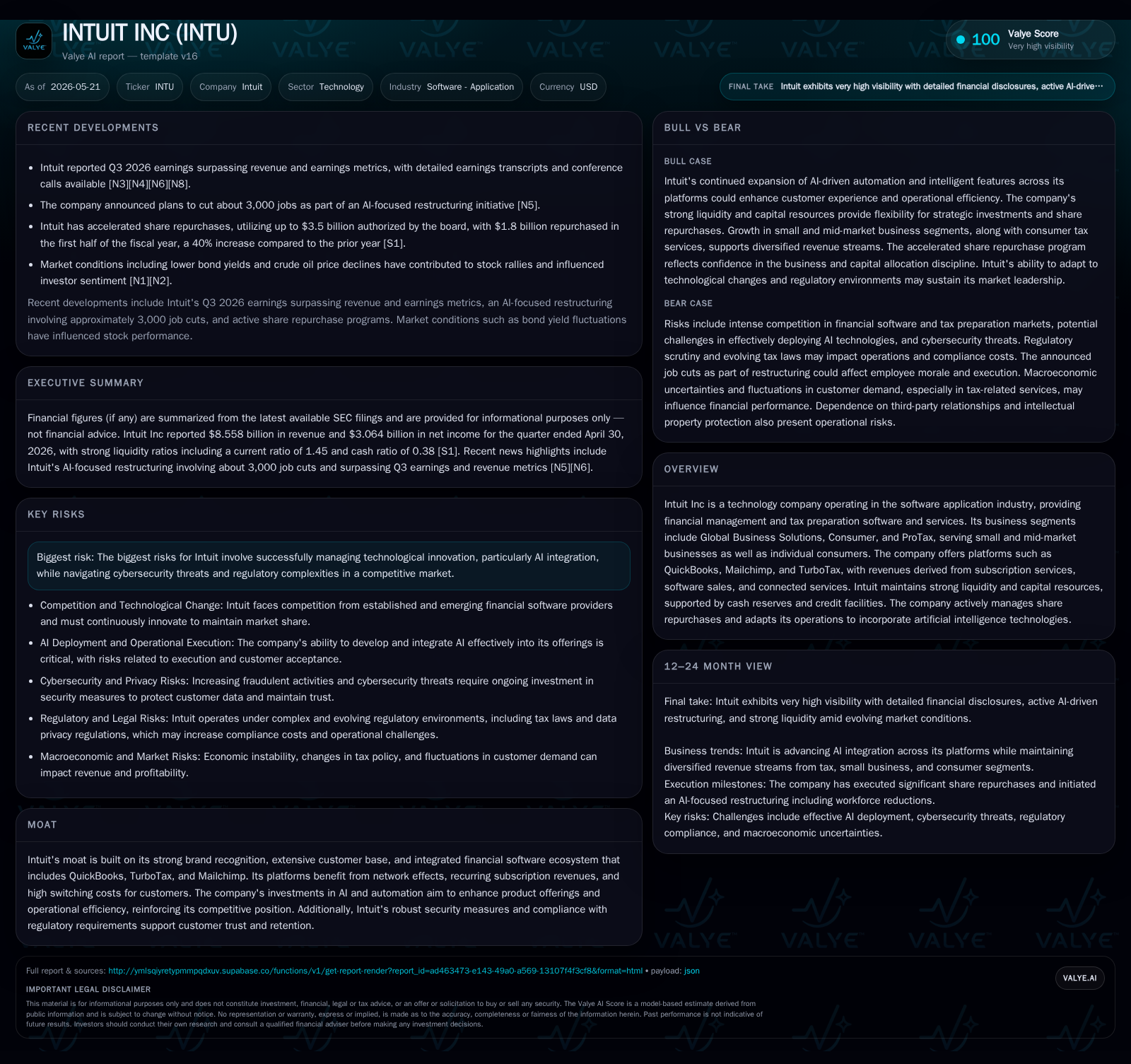

Intuit Inc reported its fiscal third-quarter results for 2026, unveiling a significant organizational restructuring including a planned workforce reduction of approximately 17%. This move aims to simplify the company’s structure and sharpen focus on AI-enhanced product development. Intuit continues to leverage its suite of financial management platforms, maintaining robust liquidity and capital resources as it adapts to evolving competitive pressures and technological innovation in the software application space. The company’s broad-based subscription revenue model anchored by QuickBooks, TurboTax, and Mailchimp underpins its resilient growth trajectory despite macroeconomic uncertainties.

Recent Operating Update

Intuit's latest quarterly filing for Q3 fiscal 2026 dated May 20, 2026 [S2] details a substantial strategic reset aimed at streamlining operations and catalyzing innovation through artificial intelligence. The company disclosed plans to reduce its full-time workforce by approximately 17%, roughly translating to about 3,000 positions according to supplementary news filings [N6]. These headcount cuts are part of an initiative to simplify the organizational structure and prioritize faster execution focused on core technology capabilities.

The related costs associated with this plan are anticipated between $300 million and $340 million; predominantly severance payments and employee benefits expected to hit the books mainly in the fourth quarter ending July 31, 2026 [S3]. Management signaled completing most actions related to this restructuring by the first quarter of fiscal year 2027 ending October 31, pending legal consultations globally.

Besides cost containment measures, the company reiterated ongoing investment in AI technologies integrated within its financial software platforms—efforts that underscore its ambition to sustain competitive differentiation through automation and data-driven analytics. This update marks an inflection where legacy scale meets nimble technology repositioning aimed at enhancing product relevance amid shifting market demands.

Business Model

Intuit's revenue generation is fundamentally subscription-driven across diversified financial solutions targeting both individual consumers and business customers. The company operates three primary segments: Global Business Solutions (including QuickBooks), Consumer (TurboTax), and ProTax (professional tax services) [S1]. Subscription fees form the backbone of recurring revenues supported by one-time software sales and connected services such as payment processing or marketing automation via Mailchimp.

The importance of network effects is pronounced given intertwined customer sets—small businesses using QuickBooks often rely on TurboTax for tax filing while employing Mailchimp for marketing campaigns—creating multi-product attach rates that enhance switching costs. Customers pay for access frequency or volume based on plan tiers; thus revenue increments are driven by user base expansion, seat scaling within enterprises, subscription renewals supported by continuous product improvements including AI features, and expanding service attachments.

This operating mix affords margin resilience owing to high gross margins typical in cloud-based SaaS offerings combined with scalable support infrastructure. Product innovation cycles tied to AI deployment enhance value propositions through process automation for bookkeeping or personalized tax advice thereby potentially reducing churn.

Industry Structure & Competitive Position

Within software applications focused on financial management and tax preparation, Intuit stands as a dominant incumbent fortified by strong brand equity—QuickBooks dominates SMB accounting platforms while TurboTax commands a significant share of consumer tax filings [S1]. Its integrated ecosystem spanning financial operations distinguishes it from fragmented peers who may specialize narrowly in either payroll or single-purpose tax solutions.

Competition includes smaller niche product vendors targeting micro-businesses or DIY consumers but Intuit's broad portfolio combined with consistent platform investments like advanced analytics represents formidable barriers. Its adoption challenges stem from regulatory complexity inherent in tax services requiring rigorous compliance frameworks alongside data security standards—areas where Intuit has invested heavily.

Meanwhile emerging tech disruptors leveraging AI pose competitive threats but also opportunities for partnerships or acquisitions—the company’s recent emphasis on developing internal AI prowess is thus both defensive and expansionary. The customer base’s stickiness is reinforced by increasing SaaS consumption models where integrated workflows lower customers’ incentive to switch or mix disparate vendors.

Growth Drivers

Several factors underpin Intuit’s growth trajectory:

- AI Integration: Embedding machine learning-driven automation accelerates task efficiency for users—from automated bookkeeping detection patterns in QuickBooks to predictive analytics guiding tax savings in TurboTax—improving product stickiness [S1].

- Subscription Expansion: Continued growth in recurring revenue fueled by upselling new functionality tiers or adding seats within existing business customers supports top-line durability.

- Platform Synergies: Cross-selling among QuickBooks, TurboTax, Mailchimp creates bundled solutions attractive especially for small-to-medium enterprises seeking simplified vendor relationships.

- Market Penetration: Increasing digital transformation across small businesses globally expands addressable market size beyond traditional domestic confines despite regulatory hurdles.

- Capital Allocation: Active share repurchase programs enhance per-share metrics providing shareholder returns while maintaining liquidity for R&D investment [S5].

These drivers collectively create a favorable compound growth environment presuming effective change management around ongoing organizational adjustments.

Risks / Watchpoints / Growth Constraints

Despite solid fundamentals, risks persist:

- AI Adoption Risks: Scaling artificial intelligence requires sustained R&D expenditures with uncertain time to impact; flawed implementation risks alienating users accustomed to human advisory roles.

- Cybersecurity Threats: As a custodian of sensitive financial data across millions of users, any breach could severely damage reputation and invite regulatory penalties.

- Regulatory Complexity: Tax reforms or governmental encroachment could shift compliance burdens unfavorably affecting cost structures.

- Operational Disruptions: The ongoing restructuring bears execution risk including potential talent loss that may temporarily impair product development velocity.

- Macroeconomic Conditions: Inflationary pressures or economic slowdowns might tighten client budgets limiting willingness to pay premium subscription fees [S24]

Close monitoring of these factors alongside disciplined execution will be vital for sustaining momentum amid competitive intensification.

What to Watch Next

Key upcoming milestones include observing quarterly progress on workforce reduction initiatives expected completion by early FY27 Q1 [S3], rollout cadence and user adoption metrics tied to new AI enhancements highlighted during earnings conference calls [N2], as well as subscription renewal rates signaling customer retention strength under evolving pricing or feature changes.

Additionally tracking capital deployment signals via announced dividend schedules—with July 17 dividend payment—and buyback activity remains essential inputs into overall financial health assessment [S14]. Market reception to restructuring announcements alongside macroeconomic headwinds will further shape visible demand patterns into the next reporting periods.

Financial Profile Context

Intuit reported cash & equivalents of approximately $4.68 billion as of April 30, 2026 alongside total debt near $6.2 billion resulting in net debt around $1.52 billion—a modest leverage profile supporting capital flexibility [F1]. Current assets were about $17.84 billion versus current liabilities near $12.28 billion, yielding a current ratio of roughly 1.45, consistent with satisfactory short-term liquidity cushioning operational needs [F1].

Operating income last reported was $4.92 billion illustrating strong earnings capacity underpinning robust free cash flow potential conducive to funding share repurchase programs actively executed over recent periods [F1] without compromising balance sheet integrity.

This analysis is based exclusively on publicly filed disclosures from Intuit Inc’s SEC submissions dated through May 2026 alongside verified news reports without incorporating non-public information or investment research views.

Financial position in context

As of 2026-04-30, companyfacts shows $4.7bn in cash and equivalents and $6.2bn of total debt [F1]. The same snapshot implies net debt of roughly $1.52bn, keeping balance-sheet context relevant but secondary to the operating story [F1]. Current assets of $17.8bn and current liabilities of $12.3bn imply a current ratio near 1.45x for 2026-04-30 [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments