Invitation Homes Builds Scale and Service Edge with Vertical Integration and Strategic In-House Development

Invitation Homes leverages its expansive portfolio, resident-focused platform, and recent acquisition of ResiBuilt Homes to fortify growth amid leverage and market risks.

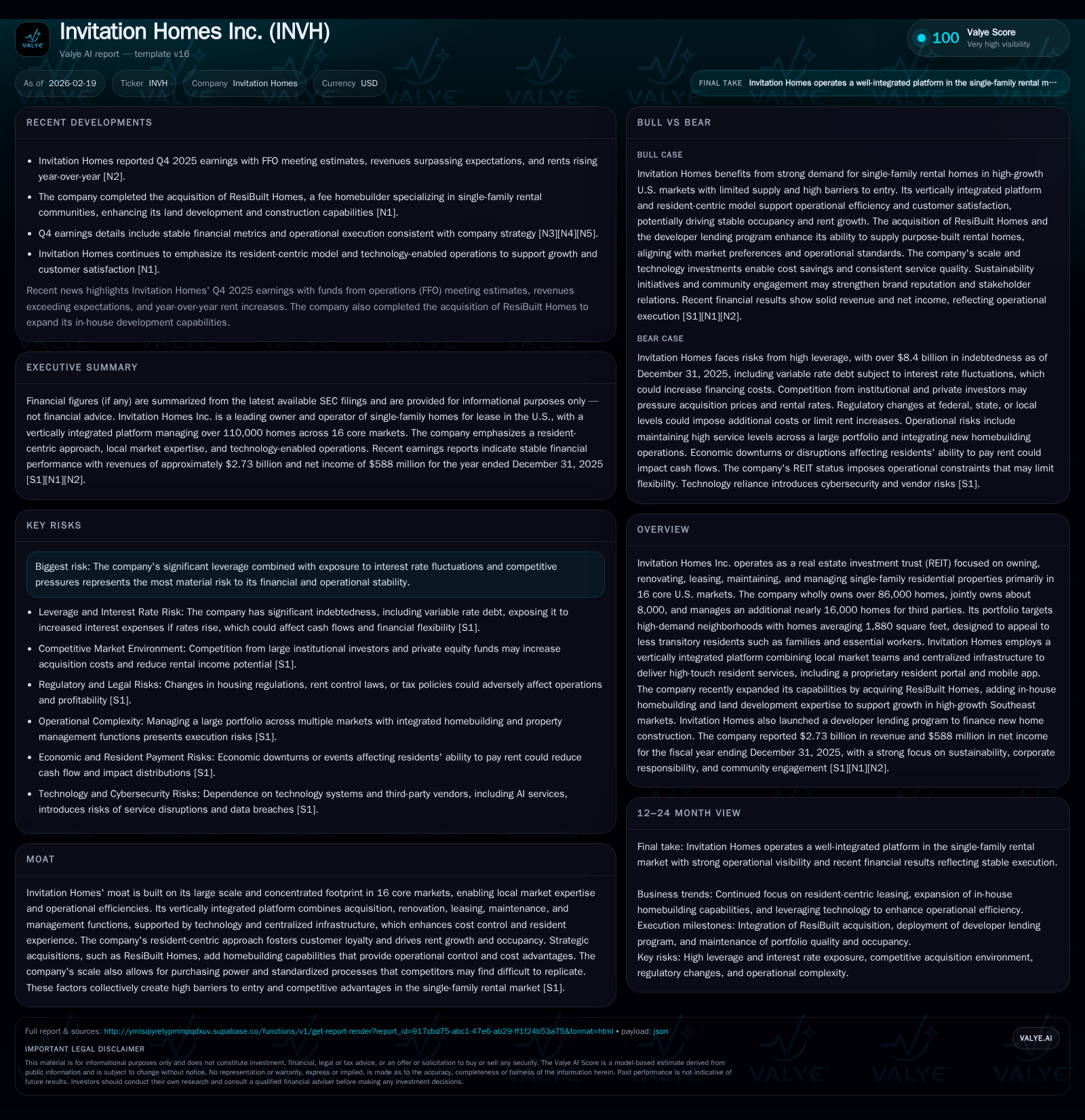

Invitation Homes Inc. operates one of the largest single-family residential rental platforms in the U.S., emphasizing a vertically integrated model that controls acquisition, renovation, leasing, maintenance, and management. Its growth trajectory over recent years has been powered by scale economies across 16 core markets, delivering steady revenue and cash flow expansion. The strategic purchase of ResiBuilt Homes bolsters its in-house homebuilding capabilities, enhancing operational control and cost management. While its resident-centric service model supports rent growth and occupancy stability, Invitation Homes must navigate significant leverage exposure amid ongoing interest rate volatility and evolving regulatory challenges impacting institutional ownership of single-family homes.

Track Record of Growth Driven by Scale and Operational Excellence

Invitation Homes Inc. has cultivated a commanding presence in the single-family rental market through disciplined acquisitions and operational scale concentrated in 16 key U.S. markets. The company's wholly owned portfolio reached over 86,000 homes as of fiscal year-end 2025, primarily located in markets characterized by high employment density and demand drivers such as quality schools and essential services including healthcare and public safety sectors [S1]. This focus has engendered a resident base with longer median tenancy than traditional multifamily units.

Financially, Invitation Homes has demonstrated robust expansion trends over the past four years with revenues climbing from approximately $2.24 billion in FY2022 to nearly $2.73 billion in FY2025. This reflects a CAGR near 4.2%, indicative of both organic rent escalations in established assets as well as accretive acquisition activity [F1]. Net income exhibited more pronounced year-over-year acceleration to $588 million in FY2025—up almost 30% from the prior year—on the back of improved operating efficiencies associated with portfolio density and integration synergies.

Operating cash flows have likewise grown steadily to surpass $1.2 billion by FY2025, demonstrating solid cash conversion given substantial upfront capital expenditures earmarked for renovations aimed at improving asset quality and lowering maintenance demands [F1][S17]. Given the scale averaging roughly 5,000 homes per core market area, local market teams benefit from economies of scale enabling more tailored asset management approaches compared to fragmented owners.

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|

| 2025 | 2.7 | 588 | 1206 | +4.2% | +29.5% |

| 2024 | 2.6 | 454 | 1082 | +7.7% | -12.6% |

| 2023 | 2.4 | 519 | 1107 | +8.7% | +35.5% |

| 2022 | 2.2 | 383 | 1024 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): OpInc, Capex, Buybacks, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | ROE% |

|---|---|---|

| 2025 | 713 | 6.2 |

| 2024 | 689 | 4.7 |

| 2023 | 638 | 5.1 |

| 2022 | 539 | 3.7 |

Source: SEC companyfacts cache [F1].

Note: Capex data is not available from provided tags for recent years; ROE is approximated using latest equity data where available.

Expanding Capabilities: The Strategic Acquisition of ResiBuilt Homes

A pivotal development shaping Invitation Homes’ future trajectory is its January 2026 acquisition of ResiBuilt Homes—a fee homebuilder specialized in single-family rental communities [N10]. This vertical integration initiative extends Invitation’s operational perimeter into land development and home construction domains previously outsourced or handled via partnerships.

Incorporating ResiBuilt’s expertise is expected to confer multiple strategic benefits: tighter control over homebuilding pipelines allows synchronization with market demand signals derived from proprietary leasing data; direct oversight over construction timelines mitigates delays common in third-party contracting; enhanced purchasing power over building materials reduces input costs amid inflationary pressures; finally, purpose-built rental homes can be designed to optimize maintenance costs while aligning closely with resident preferences for modern layouts equipped with energy-efficient features [S11].

This move complements Invitation Homes’ existing renovation-focused strategy by adding a new dimension—organic supply generation—that could prove critical given persistent national housing shortages impacting acquisition opportunities.

Resident-Centric Platform as a Competitive Advantage

Invitation Homes maintains a differentiated tenant experience model grounded in localized asset management melded with centralized technology platforms—a dual approach that enhances rental rate realization while driving tenant retention metrics superior within the single-family rental sector.

Each core market is overseen by a Vice President of Operations managing cross-functional teams responsible for leasing, property management, maintenance scheduling, and customer service responsiveness [S12]. Leveraging proprietary AI-powered pricing algorithms analyzing publicly available market data alongside occupancy trends enables dynamic rent setting tailored to neighborhood-specific factors including school rankings, employment accessibility, and competitive listings [S13]. Resident interactions are supported through a comprehensive mobile application facilitating online rent payments, scheduling maintenance requests, and providing transparent communication channels.

This service intensity supports lower turnover rates versus peers leveraging asset-light third-party management models—critical given the higher average unit size (~1,880 sq ft) predominantly configured as family residences rather than short-term rentals or multifamily units which tend toward greater churn [S1]. Moreover, the "ProCare" vertically integrated service platform standardizes maintenance response times and preventive upkeep schedules anchored by negotiated vendor agreements ensuring consistent quality while controlling cost inflation within renovations and repairs [S17].

Capital Structure Dynamics: Managing Leverage in a Complex Market

As of December 31, 2025, Invitation Homes carried total aggregate indebtedness approximating $8.46 billion secured primarily through non-recourse mortgage loans tied directly to specific pools of owned properties [S4][S5][S7][S8]. This financing architecture offers capital efficiency but simultaneously escalates risk profiles given potential foreclosure events triggered by covenant breaches or cash flow decrements at underlying collateral levels.

Approximately $2.62 billion bears variable interest rates exposing earnings streams to fluctuations stemming from macroeconomic interest rate movements even though the REIT employs swaps, caps, and other derivatives instruments aimed at mitigating these exposures within prescribed REIT qualification constraints [S8][S21]. The company highlights potential adverse scenarios including refinancing difficulties or restricted access to securitization markets secondary to political or regulatory scrutiny affecting asset-backed securities issuance patterns frequently utilized for such portfolios [S9].

Additionally, covenants linked to debt instruments may limit strategic flexibility particularly regarding dispositions or new acquisitions if minimum debt yield or service coverage thresholds are jeopardized leading to accelerated principal repayment requirements or restrictive excess cash sweep mechanisms beneficial chiefly to lenders rather than equity holders [S7][S8].

Market Positioning Across Core U.S. Geographies

Invitation Homes’ portfolio is deliberately concentrated within select high-demand corridors across the Western United States (including California and Arizona), Florida, and Southeastern states such as Georgia and North Carolina where demographic expansion drives robust rental demand fundamentals bolstered by strong labor markets [S6][S14].

This geographic density—achieving portfolio sizes upwards of ~5,000 homes per core market—facilitates deep local knowledge on micro-market factors such as neighborhood-level occupancy dynamics or amenity appeal allowing more precise underwriting versus broadly diversified portfolios sacrificing granularity for scale alone. Conversely, the scale also enables centralized procurement frameworks on renovation inputs yielding unit cost savings unavailable to smaller regional owners.

State legislative environments range widely but Invitation Houses actively navigates these through local compliance teams ensuring alignment with jurisdictional eviction laws, tenant rights statutes, and emerging rent control policies which have intensified scrutiny on large institutional landlords impacting operational margins across some regions [S24].

Navigating Risks: Interest Rate Sensitivities and Regulatory Environment

Leverage remains a double-edged sword for Invitation Homes; while fueling portfolio expansion it exposes the company’s earnings stability to volatility from rising interest rates particularly on floating-rate instruments net of hedges potentially squeezing distributable cash flow owed investors as dividends mandated under REIT tax qualification rules.

Moreover, increased political attention directed at institutional ownership concentration within single-family housing markets threatens regulatory headwinds including potential caps on acquisition volumes or enhanced reporting requirements designed to preserve affordability for end consumers—a factor shaping lobbying efforts among real estate industry groups currently underway [S1][S18][S22][S24]. Tenant protection ordinances encompassing eviction moratoriums or rent hike restrictions entered variably across states impose operational challenges limiting landlords’ ability to optimize income streams given fixed mortgage obligations offsetting rising expenses particularly insurance premiums driven by climate-related risk increases noted by management discussions highlighting exposure analysis frameworks aligned with national climate resilience standards [S25].[...] Cybersecurity safeguards emerge increasingly crucial given dependence on digital leasing applications; data privacy regulations such as CCPA enhance compliance costs though proactive investments mitigate material breach risks comparatively low relative to sector peers documenting security incidents damaging reputations or incurring regulatory penalties [S23].[...]

Financial Performance Snapshot: Revenue, Earnings, Cash Flow, and Capital Returns

Invitation Homes’ trailing financial results portray steady improvement in top-line revenue spurred primarily through rent escalations combined with selective accretive acquisitions completed through disciplined underwriting standards leveraging local market intelligence pools [F1][S26]. Net income improvements disproportionately outpace revenue driven partly through operating leverage benefits afforded by highly centralized administration reducing duplicative costs common among fragmented smaller operators.

Operating cash flow reached approximately $1.21 billion for FY2025 reflecting strong collections consistency coupled with effective capital expenditure controls targeting critical renovation outlays while avoiding excess discretionary spend typical within transitioning portfolios.[F1][S17] Capital expenditures remain focused centrally around upfront capital reinvestment yielding longer-term expense reductions rather than reactive repairs indicative of legacy cyclicality dependency seen among smaller-scale owners.[...] Dividends paid rose correspondingly supporting shareholder expectations consistent with REIT distribution norms totaling $713 million during FY2025 supplemented only modestly via share repurchases totaling $53 million reflecting conservative balance sheet prioritization amidst uncertain refinancing environments.[F1] Return on equity calculated around mid-single digits (~6.2% in FY2025) aligns reasonably given the combination of heavy leverage structures paired with stable recurring income source although incremental improvement hinges on achieving enhanced margin performance partly via vertical integration gains realized from recent acquisitions.[...]

Future Outlook and Emerging Growth Catalysts to Monitor

Going forward Invitation Homes’ ability to capitalize on its expanded vertical integration platform including land development activity will likely be a critical driver differentiating it from competitors predominantly reliant on external supply sources dependent on fluctuating local inventory conditions.[N10] Success factors include streamlining permitting cycles leveraging local relationships augmenting digital tools for pre-construction resident demand aggregation coupled with supply chain procurement innovations realizing material savings projected into margin expansion opportunities beyond traditional renovation focused approaches. Rent trajectory sustaining positive momentum supported by tailored pricing algorithms combined with high-touch community engagement initiatives focusing on retention will equally shape near-term top-line stability against broader macroeconomic headwinds influencing affordability metrics affecting demand elasticity.[...] Simultaneously managing debt maturities prudently amidst evolving interest rate cycles along with engaging proactively on regulatory developments curtailing institutional single-family ownership will remain key governance priorities balancing growth ambitions against risk mitigation imperatives inherent within sizeable leveraged real estate platforms. The company’s technology-enabled leasing models augmented by smart-home feature rollouts also represent incremental ancillary value propositions contributing favorably toward resident satisfaction scores potentially translating into sustained occupancy gains relative to broader market benchmarks.[...] Investors should watch closely quarterly results commentary for updates on integration progress post-ResiBuilt acquisition alongside maintenance capex variability reflecting shifts toward newly constructed inventory versus legacy renovation-driven expenditures which may recalibrate cash flow dynamics widely followed by REIT analysts.

Disclaimer: This analysis is for informational purposes only based on publicly available sources cited herein as of February 19, 2026; it is not an investment recommendation nor does it offer forecasts beyond documented company disclosures.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments