InvenTrust Properties Corp.: Navigating Sun Belt Retail with Inflation-Linked Stability

How InvenTrust leverages its specialized retail footprint and judicious capital management to deliver resilient income amid macroeconomic volatility.

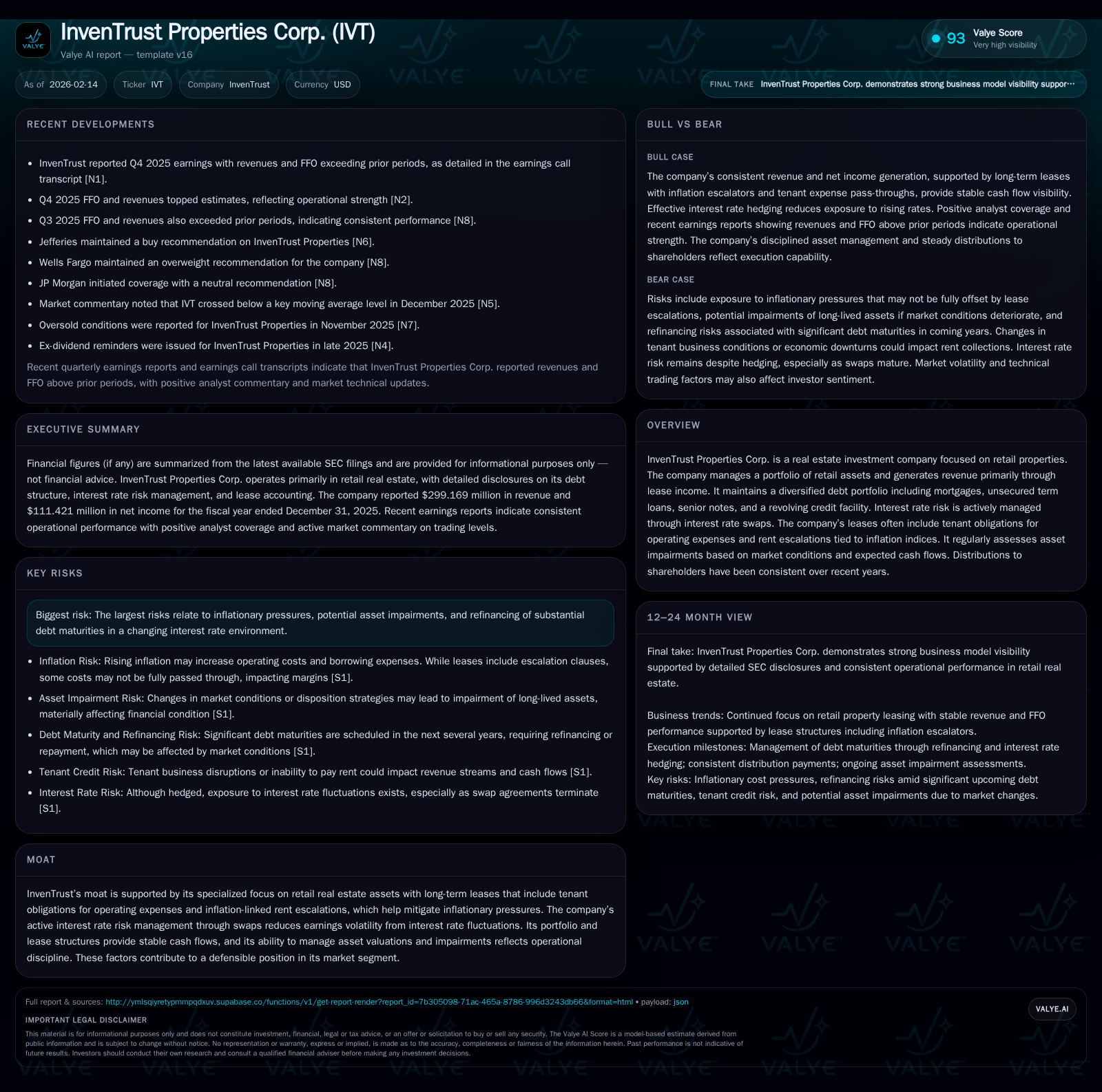

InvenTrust Properties Corp. has carved a niche as a premier Sun Belt retail-focused REIT, concentrating on grocery-anchored centers in demographic-rich regions that support steady demand growth. The company’s leasing approach includes inflation-indexed rent escalations and tenant-covered operating expenses, buffering cash flows from rising costs. Their disciplined capital structure, including staggered debt maturities and active use of interest rate swaps, mitigates refinancing and interest rate risks. While external pressures like inflation and debt reset timelines pose challenges, InvenTrust’s portfolio quality, strategic acquisitions, and consistent dividend record underpin its competitive positioning.

Sun Belt Strategy: Geography as a Competitive Advantage

InvenTrust's deliberate focus on Sun Belt markets is more than geographic preference; it's an essential ingredient in its competitive recipe. These regions boast population, employment, income, and educational attainment growth rates that outpace national averages [S1]. This demographic vitality sustains robust demand for essential retail services—particularly grocery-anchored centers that form the backbone of InvenTrust’s portfolio.

The company’s locally embedded field offices are critical in maintaining close tenant relationships and market intelligence—enhancing responsiveness to micro-market dynamics. This hands-on strategy not only strengthens occupancy levels but also positions InvenTrust to capitalize on anticipated rent escalations driven by favorable economic undercurrents in these fast-growing corridors.

Retail Portfolio Composition: Grocery Anchors and Necessities

InvenTrust’s portfolio is distinguished by its grocery-anchored assets—a strategic bet on necessity-based retail that generally withstands economic cycles better than discretionary shopping centers [S1]. Anchors such as Whole Foods Market, Trader Joe's, Sprouts Farmers Market, Wegmans, Harris Teeter, and Publix dominate the center landscapes across key markets including Charlotte-Gastonia-Concord (NC), Phoenix-Mesa-Chandler (AZ), Charleston (SC), San Antonio (TX), Richmond (VA), Asheville (NC), Cape Coral-Fort Myers (FL), Tucson (AZ), and Savannah (GA) [S1].

These grocers draw consistent shopper traffic which sustains smaller inline tenant sales and supports high occupancy. This tenant mix diffuses risk by avoiding vulnerability solely to discretionary spending trends, offering a defensive moat as consumers continue prioritizing necessities—even during economic uncertainty.

Leasing Dynamics: Inflation-Linked Rents and Tenant Obligations

A notable feature of InvenTrust’s leasing agreements lies in their embedded rent escalations tied to consumer price indices alongside comprehensive tenant obligations to cover operating expenses [S1]. This lease architecture effectively shifts inflation-related cost burdens away from the landlord toward tenants.

Management’s narrative during recent earnings notes the efficacy of this structure in preserving cash flow margins amid rising input costs — an advantage not universally found in retail REITs [N1]. Tenants' responsibility for common area maintenance, property taxes, insurance, and utilities fortifies NOI resilience even as headline inflation pressures persist.

Such contractual inflation linkage also projects upside potential if sustained consumer price inflation continues. This rental framework aligns well with the Sun Belt's ongoing economic expansion where upward pressure on rents can be realized over time without sacrificing occupancy.

Capital Structure: Managing Debt Maturities and Interest Rate Risks

Prudent financial stewardship is manifest in InvenTrust’s layered debt portfolio. Mortgages spread out maturities through 2030 with substantial principal outstanding beyond 2026 — approximately $27 million due in 2027 alone — allowing measured refinancing timing [S1]. Unsecured term loans totaling $400 million mature mostly between August 2030 and February 2031 with low fixed coupon rates locked via interest rate swaps expiring late 2026 or early 2027 [S1].

The $500 million revolving credit facility with flexible terms extending potentially into mid-2029 provides liquidity headroom with $445 million available as of December 2025 [S1]. Critically, the company employs interest rate swaps to hedge floating rate exposure — converting variable rates to fixed rates near 2.6% until swap expirations. Post-swap expiry will likely expose the company to higher borrowing costs approximately at current market spreads around mid-2026 through early 2027 [S1].

This staggered debt maturity ladder coupled with hedged interest expense reflects a conscious buffer against looming refinancing risks amid an overall rising rate environment—a key consideration given future interest cost uncertainty.

Recent Acquisition and Disposition Activity: Strategic Capital Recycling

Throughout 2025, InvenTrust invested roughly $465 million acquiring ten properties predominantly anchored by high-quality grocers across high-growth Sun Belt submarkets such as Tucson (Trader Joe's Plaza Escondida), Charleston-West Ashley Station (Whole Foods), Richmond-West Broad Marketplace (Wegmans), Cape Coral-Daniels Marketplace (Whole Foods), among others [S1]. Many acquisitions were unencumbered by debt or had mortgages assumed at reasonable valuations.

Simultaneously, the company divested a sizable California portfolio—five properties totaling 746k square feet—for $306 million realizing gains near $91 million [S1]. Additionally, it sold Custer Creek Village in Dallas area following condemnation settlements.

This tactical recycling sharpens the portfolio toward core Sun Belt markets where demographic fundamentals reinforce long-term value while crystallizing profits from premium west coast assets no longer fitting strategic priorities. Such disciplined asset management underscores flexibility amid shifting retail real estate conditions.

Operating Performance: Cash Flow Stability Amid Market Flux

In Q4 2025 earnings release and call transcripts reveal solid operating trends despite uncertain macro backdrops [N1,N3]. Net Operating Income (NOI) has advanced steadily reflecting healthy same-property performance bolstered by new acquisitions [S1]. Core Funds From Operations (Core FFO) topped consensus estimates comfortably signaling underlying cash flow robustness.

Leased occupancy remains elevated with minimal disruption in leases rolled over—an indication of resilient tenant retention within necessity-based categories despite broader sector turbulence [N3]. Rent collection metrics remain sound benefiting from leases indexed to inflation and tenant expense pass-throughs that limit margin compression.

Such stable operating results emanate directly from the interplay of geographic strategy favoring growing Sun Belt hubs combined with defensive asset composition highlighted earlier—in sum producing reliable income streams for shareholders.

Risk Assessment: Inflation, Refinancing, and Market Volatility

Despite strengths outlined above, InvenTrust faces material risks that warrant attention. Inflationary environments increase operating expenses which even after tenant reimbursements may pressure cash flows if escalation caps or vacancy rises occur [S1,S2]. Persistent or accelerating inflation remains a wild card impacting property valuations through increased cap rates or impairment tests.

On refinancing fronts, substantial mortgage principal ($around $62 million) matures by end-2029 alongside unsecured term loans due in 2030–2031 requiring proactive capital planning especially as interest rate swaps protecting low borrowing costs expire primarily by late 2026–early 2027 exposing cost resilience vulnerability [S1]. Adverse macroeconomic shifts or credit market tightening could amplify refinancing challenges.

Additionally, retail real estate continues navigating secular consumer behavior changes posing residual occupancy or leasing risk especially for centers lacking compelling anchors or facing local market oversupply though InvenTrust’s focus mitigates this relative to more cyclical peers.

Dividend Track Record: Consistency for Investors

One cornerstone of InvenTrust’s shareholder appeal is its disciplined distribution policy demonstrated over recent years. Distributions declared grew consistently from roughly $55.7 million in 2021 up to nearly $73.8 million in 2025 despite volatile macro conditions [S1]. These payouts have been matched closely by payments evidencing reliable cash flow backing distributions.

For income-focused investors seeking yield stability within real estate equities, this uninterrupted distribution growth trend—supported by stable operating cash flows—enhances confidence. It also reflects management’s balanced approach between growth reinvestment opportunities and returning capital to shareholders.

Valuation Considerations: Balancing Growth and Defensive Attributes

While exact valuation levels depend on market dynamics beyond public filings alone [F1], an analytical lens suggests InvenTrust merits distinct consideration among retail REITs due chiefly to its concentrated high-quality Sun Belt holdings coupled with leasing structures insulating against inflation shocks.

Investors may weigh these defensive characteristics against challenges posed by refinancing timelines coinciding with possible higher-rate regimes in mid-decade periods. The company’s demonstrated ability to recycle capital into accretive acquisitions further supports growth prospects within attractive demographic corridors.

Ultimately valuation assessments need integration of qualitative moats—regional demographic favorability plus lease terms—with quantitative financial health measures relative to peer benchmarks reflecting broader sector rotation affecting retail real estate sentiment.

This analysis is provided solely for informational purposes based on publicly available data as of February 14, 2026. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments