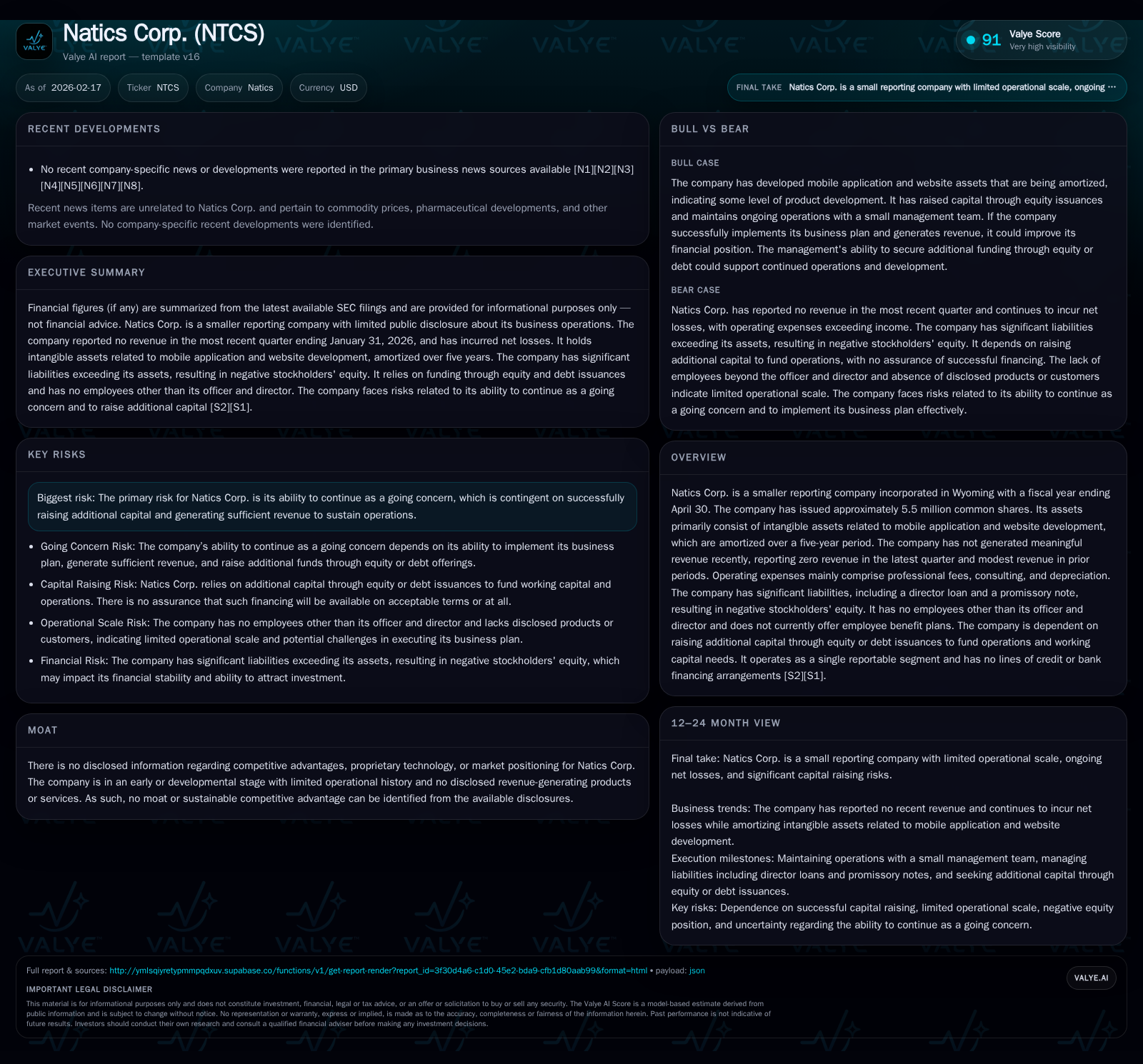

Natics Corp. Financial Fragility and the Quest for Operational Viability

Natics Corp. grapples with an absence of revenue, negative equity, and dependence on external capital amid developmental-stage asset composition.

Natics Corp., a microcap company primarily invested in mobile app and website development intangible assets, has yet to establish consistent revenue streams and operates with a very lean team. The firm's financials reveal a working capital deficit and significant liabilities including director loans and promissory notes, underscoring its fragile liquidity position. Continued operations hinge on securing additional funding while navigating dilution risks and the absence of any discernible competitive moat.

Intangible Assets at the Core: Valuing Natics’ Developmental Footprint

Natics Corp.’s asset base is notably weighted toward intangible assets, principally linked to mobile application and website development activities. As reported in the latest quarter ending January 31, 2026, these intangibles stand at approximately $15 million net of accumulated amortization [S16]. The firm employs straight-line amortization over a five-year horizon which commenced in April 2022 upon declaring the assets fully operational [S16]. This approach results in annual amortization charges diluting reported earnings but better matches the expense recognition to hypothesized product utilization periods.

This concentration of intangible assets without corresponding tangible production or revenue-generating physical infrastructure flags valuation complexity. Unlike conventional tech firms where software capitalizations align with active deployments or license streams, Natics appears in a developmental phase lacking repeated contract wins or product monetization . Consequently, these assets are more akin to capitalized development costs rather than proven revenue drivers.

Revenue Stagnation Amid Rising Operating Costs

Revenue generation remains subdued for Natics Corp., with the most recent quarterly report registering zero sales [F1]. Historical data show sporadic modest revenue recognition (e.g., $20,400 during nine months ended January 31, 2026), suggesting nascent client engagements or limited contract activity [S16,S13]. This pattern underscores the challenge many early-stage software developers face: balancing upfront R&D investment against protracted commercial traction timelines.

Meanwhile, operating expenses are nontrivial and have escalated due chiefly to professional fees, consulting services, and depreciation/amortization expenses related to intangible assets [S16,S13]. This cost structure—typical for developmental tech firms—leads to sustained operating losses (net loss -$7,212 as of January 2026) that erode shareholder value given minimal offsetting revenues.

The net operating cash burn trend intensifies liquidity concerns especially when coupled with fixed contractual interest payments owing on debt instruments such as promissory notes at a high effective rate (10% annually) [S18,S16].

Capital Structure Review: Debt Weight and Dilution Risks

Natics’ balance sheet reveals signficant long-term liabilities dominated by a director loan amounting to nearly $25,600 and a $43,000 promissory note subject to 10% annual interest payments [S16]. These borrowings signal constrained access to traditional credit markets often faced by microcaps lacking robust collateral or credit profiles.

Total liabilities surpass total assets resulting in negative stockholders’ equity—a red flag indicating solvency challenges absent near-term capital infusion [F1]. The lack of banking facilities such as lines of credit compounds this fragility.

Management openly acknowledges reliance on future equity or convertible debt financing rounds to sustain operations beyond three months from report dates [S3,S5]. Such issuances inevitably dilute existing shareholders’ stakes, especially problematic when accompanied by rights or preferences senior to common stock.

With no agreements finalized for new financing nor binding arrangements with directors for further loans, the capital raising process remains uncertain posing heightened execution risks [S3,S5,S23].

Governance and Operational Capacity: A Lean Team Model

Only one individual occupies the officer/director role at Natics Corp., with no additional employees or formal benefit plans implemented [S24]. While efficiency through minimal staffing can conserve cash during early phases, it entails operational brittleness given concentrated responsibilities. Execution risk rises when innovation pipelines and fundraising efforts depend heavily on this infrateam setup without distributed managerial layers.

This model is not uncommon among microcap developmental-stage companies emphasizing consultant engagements for technical work rather than building internal headcount. However, it inherently restricts speed and capacity for scaling until expanded organizational resources emerge.

Liquidity Cruncher: Short-Term Survival and Funding Plans

Current assets stood at roughly $5,667 against current liabilities exceeding $16,125 as of January 31, 2026 yielding a current ratio around 0.35—significantly below healthy benchmarks typically above 1 for sustaining short-run obligations comfortably [F1]. This working capital deficit indicates statutory liquidity pressures necessitating prompt capital inflows.

Management states existing funds are expected sufficient only for three months of operation without confirming committed funding sources beyond informal director loans or anticipated securities issuances [S3,S10,S16]. The absence of bank credit lines narrows flexibility in addressing unforeseen expenses or bridging gaps caused by slower-than-expected revenue ramp-up.

Strategic uncertainty regarding timing and terms of new financing crystallizes into an acute survival imperative aligned with investor caution flags common in early-stage public entities reliant on external funding cycles .

Risks Embedded in the Going Concern Assumption

Natics explicitly discloses that its financial statements are prepared assuming continuation as a going concern; nonetheless this assumption hinges critically on successful implementation of business plans involving incremental capital raises and revenue generation [S12,S21,S22].

Failure to obtain adequate financing or accelerate sales may compel asset write-downs or accelerated liability settlements impacting recoverable values adversely. No legal contingencies appear currently [S1,S21], but insolvency risk heightens given persistent negative net worth conditions.

Given these dynamics, stakeholders should be mindful of volatility triggered by liquidity shortfalls typical in tech startups operating under thin capitalization structures.

Market Positioning Void: The Absence of a Definable Moat

Valye’s assessment confirms Natics lacks any disclosed sustainable competitive advantage or proprietary technology from available regulatory filings—an important consideration in assessing long term viability .

In mobile application development sectors characterized by intense competition and low entry barriers from global developers leveraging scalable cloud infrastructure, standing out requires unique IP portfolios or entrenched client relationships neither documented nor evidenced here.

This absence raises allocation prudence flags as it diminishes prospects for defensible pricing power or recurring income underpinning valuation beyond speculative investment tied solely to potential growth trajectories.

Outlook: Strategic Options in an Ambiguous Growth Environment

Looking forward, Natics Corp.’s immediate priority involves securing adequate financing while refining operational focus possibly through partnerships or strategic pivots enhancing monetization pathways. Traditional startup playbooks suggest leveraging convertible securities as stopgap instruments though these enhance dilution risks facing shareholders already undercapitalized.

Absent fresh capital injections aligned with accelerated product commercialization schedules, existential threats escalate alongside scale limitations imposed by lean organizational design. Market realities necessitate balancing growth ambitions against cash runway preservation—potentially constraining aggressive expansion until foundational stability is re-established.

Investors tracking such developmental entities should monitor funding announcements closely given that execution success depends heavily on sequencing capital access with tangible revenue generation milestones underpinned by improved organizational bandwidth.

This analysis is intended solely for informational purposes reflecting facts as disclosed through SEC filings and Valye News proprietary research up to February 2026. It does not constitute investment advice or recommendations but aims to provide an analytical framework around Natics Corp.’s financial condition and strategic positioning as gleaned from publicly available data.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments