SCI Engineered Materials: Unpacking Financial Resilience and Strategic Ambiguities

SCI Engineered Materials exhibits notable financial solidity while operating under a veil of limited operational transparency.

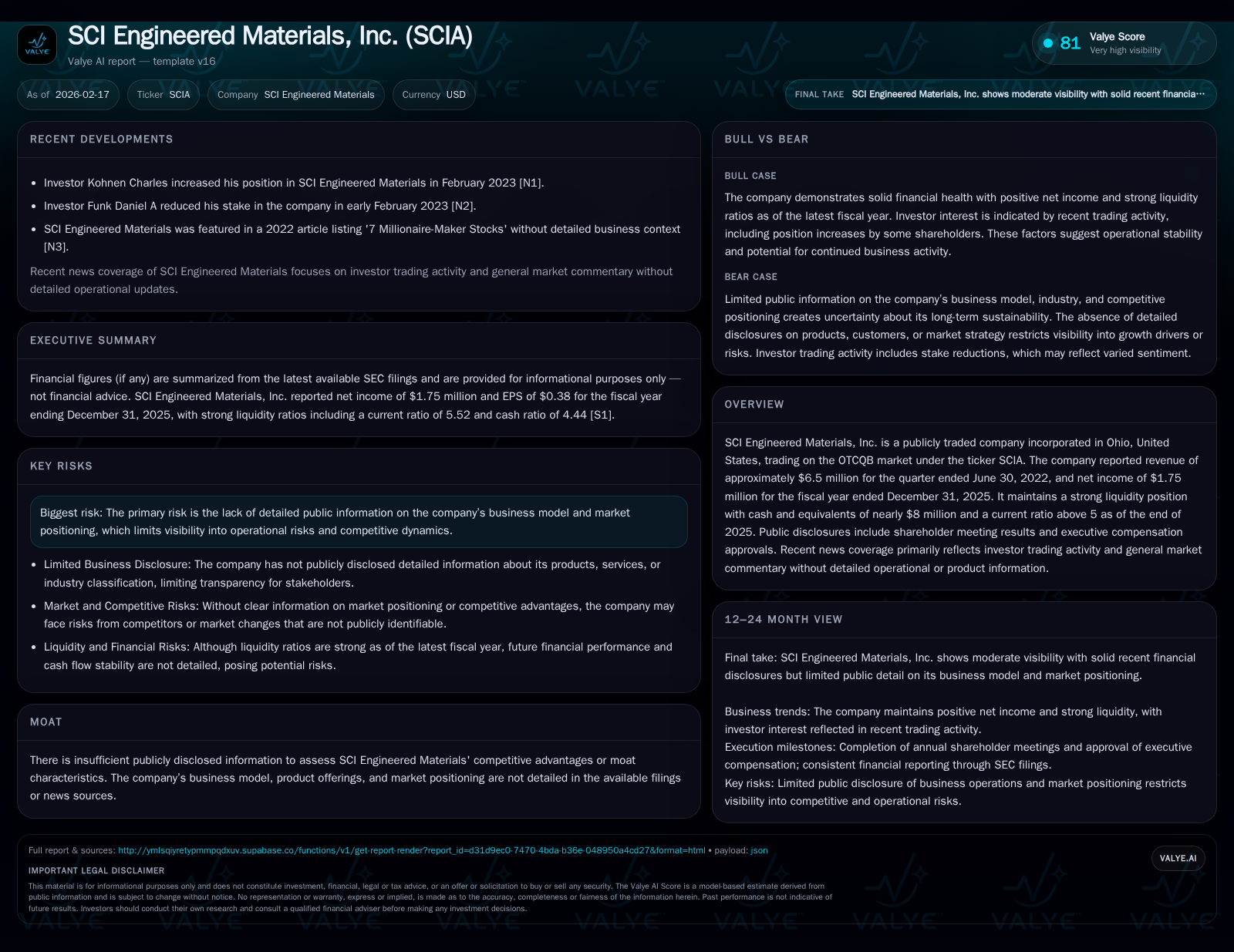

SCI Engineered Materials, trading on OTCQB under SCIA, reported $6.5 million revenue as of mid-2022 and $1.75 million net income by end-2025. The company maintains strong liquidity with nearly $8 million in cash and a current ratio exceeding 5, reflecting a conservative balance sheet approach. However, its business operations and market positioning remain largely opaque, complicating comprehensive risk and moat assessments. A significant recent bank fraud event added scrutiny to its risk controls, though management’s response indicates robust governance.

A Snapshot of SCI Engineered Materials’ Financial Health

SCI Engineered Materials recorded revenues near $6.5 million as of Q2 2022, progressing to a net income figure of approximately $1.75 million by the end of fiscal year 2025 [F1][S1]. These figures denote a modestly profitable enterprise navigating competitive pressures possibly associated with specialized engineered materials markets.

Balance sheet metrics confirm a conservative financial posture: current assets tally roughly $10.25 million against current liabilities around $1.86 million, yielding a current ratio—an indicator of short-term liquidity—exceeding 5.5 [F1]. This level surpasses typical industry norms where ratios closer to 2–3 are average for manufacturing-intensive sectors, suggesting substantial liquidity buffers.

Liquidity Strength: Navigating With High Current Ratios and Cash Reserves

The company’s near $8 million in cash and equivalents at year-end 2025 provides operational flexibility uncommon for OTC-listed small caps [F1]. Such reserves cushion against market cyclicality and enable nimble responses absent high leverage or external financing burdens. Although detailed debt structure disclosures are minimal, multiple contemporaneous SEC filings affirm no material indebtedness impairing liquidity [S10][S11][S12].

High current ratios can sometimes reflect inventory buildup or sluggish receivables; however, absent granular disclosures about working capital constituents prevents conclusiveness here. Still, the conservative liquidity position underscores prudent balance sheet management amidst uncertain business clarity.

The Elusive Business Model: Piecing Together Operational Clues

Public filings offer scant detail on SCI’s exact product portfolio or client base beyond classifying itself within engineered materials [S1][S5]. Common segments in this space include specialty coatings, composites, advanced adhesives, or polymeric compounds tailored for industrial applications — yet no affirmation is present here.

This opacity challenges third-party investors’ ability to discern end markets served or technology differentiation, raising questions on scalability and competitive positioning. In engineered materials sectors generally, differentiation often hinges on intellectual property or customer integration depth; such traits remain unsubstantiated for SCI.

Risk Factors and Legal Hurdles: What the Filings Reveal

SCI discloses relatively limited litigation threats but flags material concerns around regulatory compliance risks typical for smaller public companies [S4][S6]. Notably, the firm confronted an external imposter scam resulting in an $898,325 loss linked to bank fraud uncovered in early February 2026 [S3][S17].

Although management acted swiftly—engaging law enforcement via the FBI IC3 portal and activating insurance remedies—the incident spotlights vulnerability to external financial risks despite internal controls. The ongoing investigation maintains focus on strengthening anti-fraud defenses without operational disruption.

Capital Strategy in a Thinly Disclosed Environment

In November 2025, SCI’s board authorized a share repurchase program capped at $1 million over one year beginning December 1 [S12][S16]. Execution plans involve employing Caldwell Sutter Capital as agent for potential block trades aligned with SEC Rule 10b-18 safe harbor provisions.

This move signals judicious use of excess liquidity towards shareholder value enhancement rather than expansion capex or debt servicing—consistent with the company’s disciplined financial stewardship amid opaque growth vectors.

Corporate Governance: Shareholder Engagement and Executive Oversight

The June 2025 annual meeting confirmed election of six directors serving through the next cycle with strong affirmative votes (>80%) from shares outstanding [S14]. Executive compensation proposals received non-binding endorsement but showed minority dissent (~20%), reflecting some shareholder sentiment concerns but overall governance stability.

Noteworthy is Vice President & CFO Gerald S. Blaskie’s retirement announcement scheduled for April 2026 [S18], prompting succession planning ahead of transition—a prudent governance practice mitigating key person risks.

Fraud Incident Implications and Risk Management Response

The reported imposter scam illustrates a rare but impactful financial crime occurrence [S3][S17]. SCI’s rapid detection and engagement with federal authorities plus insurer cooperation suggests matured risk management infrastructure on par with peer small-cap issuers attempting to contain evolving cyber-finance threats.

Importantly, there is no indication that proprietary data systems suffered unauthorized breaches nor operations were disrupted materially—a critical safeguard in maintaining investor confidence despite adverse events.

Market Presence and Trading Realities on OTCQB

SCIA’s listing on the OTCQB marketplace inherently limits liquidity and broad institutional access compared to national exchanges. OTCQB stocks carry ‘grey market’ nuances including sporadic trade volumes, diminished analyst coverage, and occasional quotations disparity—all complicating valuation accuracy for market participants.

These factors contribute to wider bid-ask spreads and deferred information flow; thus careful vigilance is warranted when interpreting price action given informational asymmetry common to smaller public engineering-materials entities.

Evaluating Moat Potential Under Public Information Constraints

With no detailed disclosures on proprietary processes, customer contracts, or patented technologies [S1], SCI’s moat status remains unquantifiable externally. Typical forms of sustainable competitive advantage in engineered materials rely on technical know-how embedded into supply chains or product uniqueness—areas unaddressed by current regulatory filings.

Consequently, while positive net income performance intimates operational competence, it does not confirm defensible market positioning necessary for long-term moat claims. Investors must weigh financial resilience against strategic ambiguities given this paucity of qualitative insight.

Disclaimer: This memorandum synthesizes publicly available information from SEC filings without extrapolating beyond verified data points. It does not constitute investment advice but serves to present grounded analysis suitable for professional institutional consideration. Readers should perform supplemental due diligence commensurate with their mandates before forming opinions about SCI Engineered Materials’ prospects or risks.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments