James River Group Sharpening Specialty Insurance Strategy with Delaware Domestication

Recent corporate governance shifts via domestication to Delaware and steady underwriting discipline frame James River's focused specialty insurance growth.

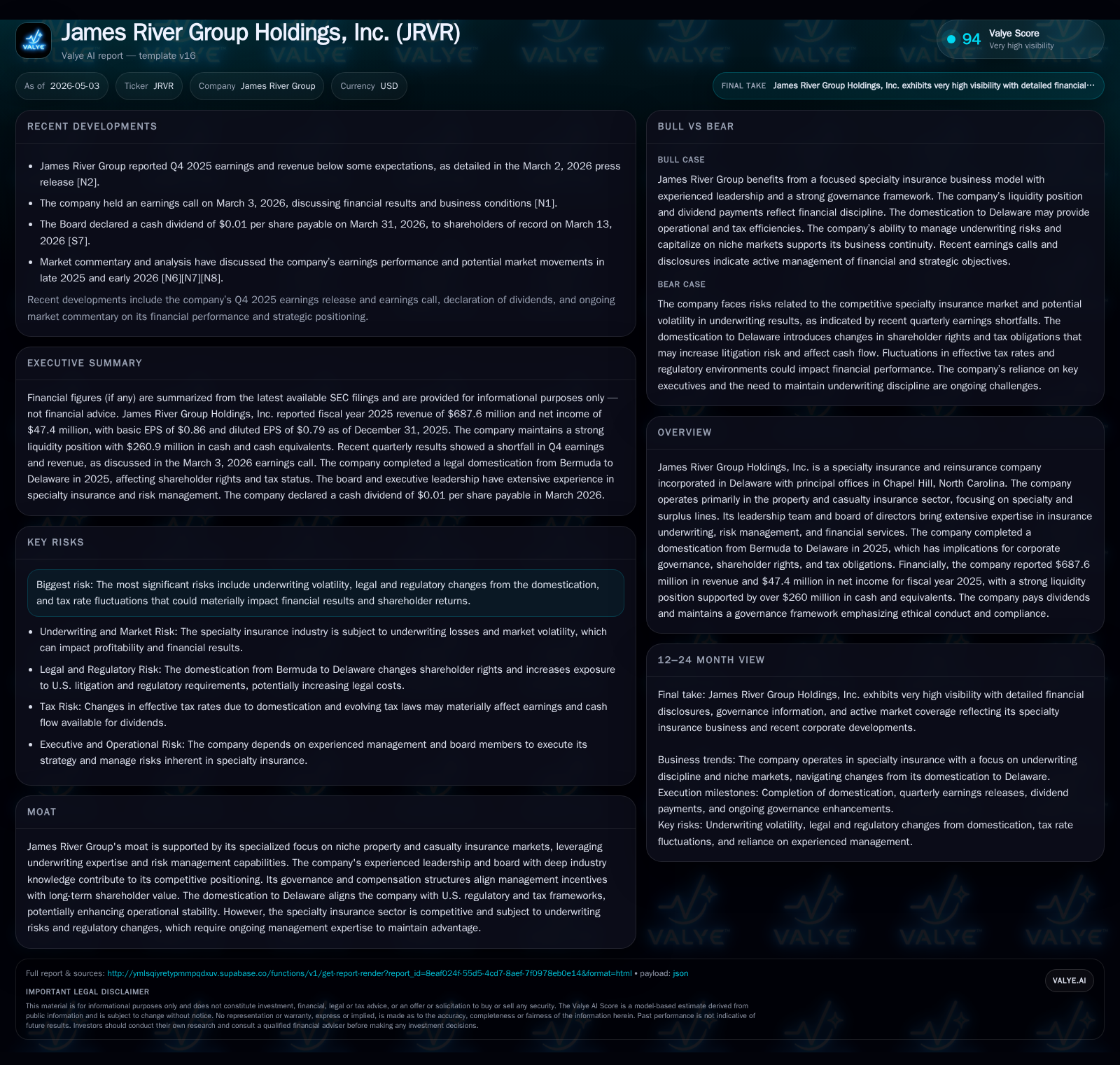

James River Group Holdings, Inc. finalized its corporate domestication from Bermuda to Delaware in late 2025, altering shareholder rights and regulatory frameworks while maintaining stable specialty property and casualty underwriting performance through the third quarter of 2025. This domestication introduces legal nuances, including increased exposure to shareholder litigation and potential tax rate changes, necessitating close monitoring. The company's concentrated strategy in niche surplus lines, supported by underwriting expertise and disciplined risk management, remains its competitive foundation amid a complex insurance landscape. Key leadership changes and governance enhancements further position James River for measured growth within evolving U.S. insurance market structures.

Operational Highlights from Latest Quarterly Filing

James River Group’s Q3 2025 10-Q filing confirmed no material changes in risk exposures compared to prior disclosures, underscoring stable underwriting operations during the transition period of corporate domestication from Bermuda to Delaware effective November 7, 2025 [S2][S25]. Notably, this jurisdictional change reshaped shareholder rights by subjecting the company to Delaware General Corporation Law (DGCL), which permits the board greater authority to amend bylaws without prior shareholder approval—a departure from the former Bermuda bylaws requiring dual approval [S2].

A consequential governance development was the April 2026 announcement that director Dennis J. Langwell will not seek re-election at the upcoming annual meeting, signaling a moderate board refreshment without operational discord [S3]. These governance evolutions reflect James River’s strategic intent to align its legal domicile with U.S. standards while preserving continuity in its disciplined underwriting culture.

Business Model and Product Focus in Specialty Property & Casualty Insurance

James River operates fundamentally as a specialty insurance and reinsurance entity focused on niche property and casualty (P&C) segments within the surplus lines space—markets characterized by unique or higher-risk coverage needs not served adequately by standard insurers [S1]. Revenue derives primarily from written premiums on specialty policies where pricing power is tempered by assessed risk profiles and competitive pressures.

The company’s underwriting expertise serves as a moat, demonstrated through sustained profitability with industry-standard performance metrics such as the Adjusted Combined Ratio and Adjusted EBIT guiding compensation plans for executives—a clear alignment of risk awareness and financial outcome emphasis [S1]. This focus allows James River to select risks conservatively, adjust pricing proactively, and deploy sophisticated claims management processes to contain loss ratios.

Industry and Competitive Positioning in Niche Surplus Lines Insurance

Within the highly fragmented specialty insurance marketplace, James River distinguishes itself through governance enhancements post-domestication that aim to streamline decision-making under DGCL while managing increased shareholder litigation risk typical of Delaware-incorporated firms [S1][S2]. The transition requires navigating elevated legal complexity but may yield greater operational stability over time versus offshore Bermuda incorporation.

Competitively, barriers-to-entry remain chiefly technical—expertise in underwriting specialties where standard insurers lack appetite—and regulatory navigation that varies by domicile. James River’s experienced leadership team combined with updated codes of conduct and incentive frameworks underpin its ability to maintain disciplined underwriting margins despite external challenges [S15][S1].

Growth Catalysts Shaping Demand and Underwriting Profitability

Expansion opportunities center on growing penetration in surplus lines sectors benefiting from market dislocations where insured entities seek tailored coverage solutions beyond commodity products [S1]. The company’s emphasis on calibrated risk selection is designed to exploit these niches while leveraging margin improvements via tighter reserve controls disclosed in filings.

Internal operational enhancements related to governance stability post-domestication provide an ancillary growth lever by supporting a consistent strategic direction amidst shifting insurance regulation regimes [S2]. Additionally, incremental product innovations or segment expansions facilitated by the firm's stewardship can diversify revenue streams without diluting underwriting rigor.

Risk Factors and Potential Constraints to Future Performance

Principal risks remain anchored in inherent underwriting volatility common to specialty P&C lines, where claims severity can be unpredictable due to catastrophic events or sector-specific exposures [S1][S2]. Furthermore, the domestication introduced heightened legal risks—Delaware law broadens class action availability and removes certain shareholder remedies available under Bermuda law—which could increase costly litigation frequency impacting operating results.

Tax-related uncertainties also present a material watchpoint; post-domestication effective tax rates may increase significantly given U.S. federal taxation compared to prior Bermuda arrangements, potentially reducing distributable cash flow for dividends or reinvestment [S2][S26]. Regulatory changes could compound these effects unpredictably over intermediate horizons.

Key Developments in Corporate Governance and Shareholder Rights Post-Domestication

The shift from Bermuda to Delaware incorporated status enacted November 7, 2025 materially altered shareholder rights frameworks: class actions previously unavailable became accessible while annulment rights over memorandum amendments were removed under DGCL [S2][S25]. These dynamics introduce additional layers of corporate legal scrutiny but may enhance board agility since bylaws can now be amended solely at board discretion.

Board composition remains relatively stable though evolving—the announced voluntary departure of Director Dennis J. Langwell in April 2026 without disagreement implicates routine refreshment rather than governance tension [S3]. Complementary amendments to the company’s Code of Conduct enhance ethical compliance requirements across all officers and employees reinforcing cultural integrity amid structural transitions [S15].

What Investors Should Monitor Next

Key near-term catalysts include the outcomes of the Company's 2026 Annual Meeting of Shareholders where director nominations and governance proposals will be decided reflecting recent strategic shifts [S3]. Management guidance updates focusing on adjusted combined ratio targets will serve as important signals regarding underwriting trends amid shifting taxation burdens.

Subsequent quarterly filings should be scrutinized for early indications of realized tax expense impacts post-domestication as well as any liability fluctuations linked to increased litigation activity stemming from expanded shareholder action rights under Delaware law. Regulatory developments particularly within surplus lines statutes or federal oversight represent additional latent variables worth tracking.

Financial Snapshot: Revenue, Profitability, and Liquidity Overview

No recent updates on debt levels were disclosed beyond historical approximations; however, net debt position reflects significant cash cushioning relative to any outstanding liabilities enhancing balance sheet flexibility amid evolving business conditions [F1].

Disclaimer: This analysis is based solely on publicly available information including SEC filings up to May 2026. It does not constitute investment advice or recommendations. Investors should consider all relevant factors before making decisions related to James River Group Holdings, Inc.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments