OneWater Marine’s Q2 2026 Results Highlight Challenges in Sustaining Profitability

The latest quarterly filing reveals a return to net losses for OneWater Marine, underscoring operational headwinds amid cyclicality in marine retail demand.

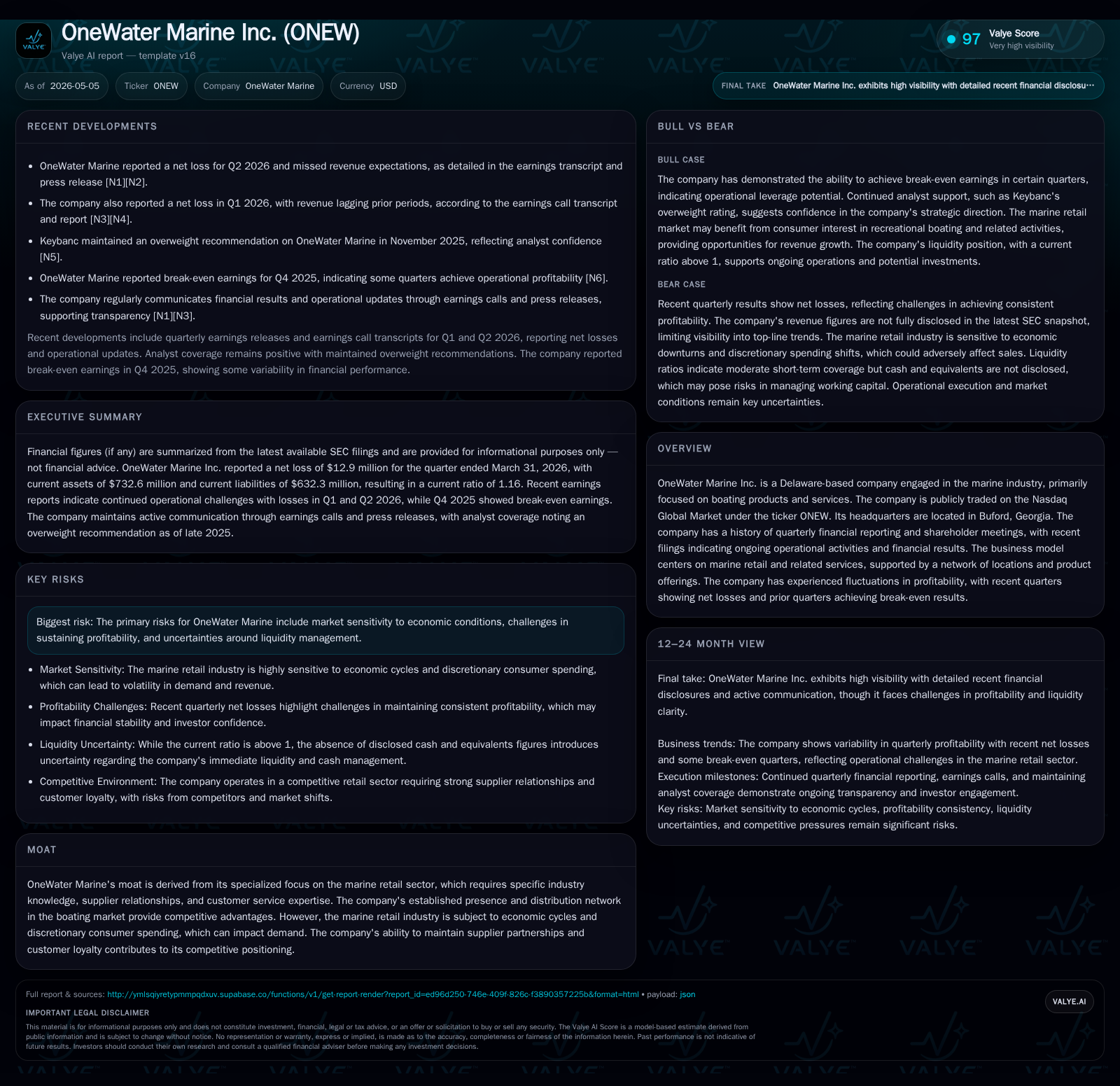

OneWater Marine reported a net loss in its Q2 2026 results, reversing prior quarters of break-even or modest profitability. This performance reflects continued demand sensitivity in the discretionary boating market and structural pressures on margins. The company’s business model, centered on retailing marine products and services through a network of physical locations, benefits from specialized supplier relationships but remains exposed to economic cycles. Growth hinges on expanding service offerings and aftermarket penetration, while liquidity and profitability sustainability remain key watchpoints.

Latest Q2 2026 Operating Update and Implications

OneWater Marine’s Q2 2026 financial disclosure via its 10-Q filing dated May 4, 2026, signals a challenging near-term operating environment. The company reported a net loss for the quarter ending March 31, 2026. After periods of approaching break-even results in prior quarters, this loss underscores renewed softness in demand within its core marine retail segment [S2]. According to the April 30 earnings transcript and press release, revenue fell short of analyst expectations primarily due to lower unit sales volumes and sustained pricing pressure amid competitive dynamics in the recreational boating market [N1][N2][S3].

Management commentary highlighted ongoing macroeconomic uncertainties affecting discretionary consumer spending patterns—a critical demand driver for OneWater’s product portfolio. Seasonal effects compounded by broader economic headwinds have led to cautious inventory positioning and tighter cost controls. Despite initiatives to optimize operations, the operational leverage inherent in the physical retail footprint intensified margin compression during the quarter [N1][S3]. This Q2 setback marks a critical juncture where prior resilience gives way to cost-revenue imbalances that challenge sustainability without further strategic recalibration.

Business Model and Product Portfolio Overview

OneWater Marine operates predominantly as a specialized retail platform focused on selling new and pre-owned recreational boats, along with an array of marine products including parts, accessories, and services designed for boat ownership lifecycle support [S1][S13]. The company leverages a network of geographically dispersed physical dealerships that facilitate direct customer engagement and access to regional boating markets. This bricks-and-mortar presence underpins OneWater’s competitive moat by fostering strong supplier relationships—particularly with leading boat manufacturers—and enabling expertise-driven customer service tailored to boating enthusiasts.

Revenue generation stems from multiple streams: core boat sales accounting for majority volume; aftermarket parts and accessories providing recurring revenue; and service operations offering maintenance, repair, and financing solutions. Pricing power varies across these lines—with new boat sales more susceptible to market price competition while aftermarket services bear higher margins owing to specialized labor and proprietary knowledge [S13]. The company’s strategic strength lies in this integrated product-service mix that cultivates switching costs through comprehensive ownership experiences.

However, reliance on seasonal selling windows paired with high fixed costs associated with dealership operations creates inherent volatility. Additionally, inventory management complexity—balancing new boat models’ introduction pace against aging used-boat stock—adds margin risk.

Industry Structure and Competitive Positioning

The marine retail industry is characterized by pronounced cyclicality linked closely to consumer discretionary income trends, recreational spending patterns, and broader economic conditions affecting leisure activities [S1][S10]. This commoditized-but-narrow segment presents barriers centered on supplier exclusivity agreements and geographic reach rather than broad scale economies. Competition includes regional independent dealerships as well as vertically integrated manufacturers that sell directly or control dealer networks.

OneWater’s competitive advantage arises partly from its scale among U.S. marine retailers and specialized knowledge enabling diverse product offerings. Nonetheless, pricing pressures stem from both competitor discounting during off-peak seasons and fluctuating input costs affecting boat manufacturing pricing structures. Supply chain disruptions can also raise acquisition costs or delay inventory refresh cycles, which directly impacts sales pacing.

Given the industry's susceptibility to economic slowdowns impacting high-ticket discretionary purchases like boats, demand volatility remains elevated. Consumer preference shifts toward more affordable vessels or rental alternatives could also reshape competitive dynamics going forward.

Growth Drivers: Opportunities amid Sector Dynamics

Despite cyclical headwinds, OneWater Marine has avenues for growth hinged on several strategic initiatives highlighted in filings and recent commentary [S1][N3]. Expanding geographic footprint enables capture of underpenetrated markets with latent boating interest. Penetration into emerging boating segments—such as smaller electric or entry-level models—could diversify revenue beyond traditional premium boats.

Another key driver is deepening aftermarket revenue streams through enhanced service offerings aligned with growing boat ownership durations. This includes maintenance packages, financing products tailored to repeat customers, and improved parts accessibility leveraging technology-driven inventory management.

Customer retention strategies centered around loyalty programs or digital engagement platforms may increase lifetime value per user amid rising customer acquisition costs. Scaling these services could improve margin profiles given their lower capital intensity relative to new boat sales.

Nonetheless, execution risk persists as these initiatives require investment ahead of tangible returns against an uncertain cycle backdrop.

Risks and Constraints Impacting Future Performance

An explicit risk identified involves OneWater Marine's vulnerability to economic conditions shaping discretionary spending patterns for recreational boating purchases. This susceptibility affects volume visibility quarter-to-quarter impacting inventory management efficacy and operating leverage outcomes [S4][S10]. Additionally, sustained inability to generate operating profits exerts strain on liquidity reserves potentially complicating debt servicing given approximately $358 million total debt reported at quarter-end [F1].

The company’s current ratio of approximately 1.16 indicates moderate short-term liquidity cushion but leaves limited room for material cash flow disruption [F1]. Furthermore, fluctuations in wholesale cost inputs or unforeseen supply chain constraints pose cost risks that erode already compressed margins.

Legal proceedings disclosed historically do not indicate material changes recently but remain a monitored area given sector regulatory environments [S11]. Finally, intensifying competition from alternative leisure activities or shifting consumer tastes may lengthen sales cycles reducing turnover velocity.

What to Watch Next: Key Milestones and Market Signals

Near term observers should focus on OneWater’s quarterly revenue trends for signs of stabilization or recovery relative to recent declines [S2][N1]. Margin trajectory will be similarly critical amid cost control efforts balanced against volume challenges.

Updates on supplier relationships may indicate inventory availability or pricing flexibility shifts that impact competitiveness or product mix favorability [S3]. Monitoring progress toward stated aftermarket service expansion goals or new dealership openings offers insight into growth strategy traction.

Macroeconomic indicators influencing discretionary income levels such as employment data or consumer confidence indices may serve as external markers affecting demand outlooks.

Finally, any guidance revisions explicitly provided will offer directionality regarding management’s expectations on navigating the current operational environment.

Latest Financial Snapshot: Balance Sheet and Liquidity Insights

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Total debt | $358mm | |

| 2026-03-31 | ||

| Net debt | $358mm | |

| 2026-03-31 | ||

| Current assets | $733mm | |

| 2026-03-31 | ||

| Current liabilities | $632mm | |

| 2026-03-31 | ||

| Current ratio | 1.16x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

At quarter-end March 31, 2026, OneWater Marine reported total debt approximating $357.9 million against current assets valued at $732.6 million resulting in a current ratio near 1.16—indicative of moderate immediate liquidity buffer [F1]. Despite this balance sheet positioning providing some resilience capacity-wise, the challenge remains sustaining positive cash flow generation given ongoing operating loss pressures seen in recent quarters [S2]. Prudence surrounding working capital management alongside careful capital allocation toward growth investments will be pivotal going forward.

This analysis is based exclusively on publicly available SEC filings dated through May 4, 2026 ([S1], [S2], [S3], etc.), supported by contemporaneous news reports ([N1]-[N3]) without forward-looking presumptions beyond disclosed information. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments