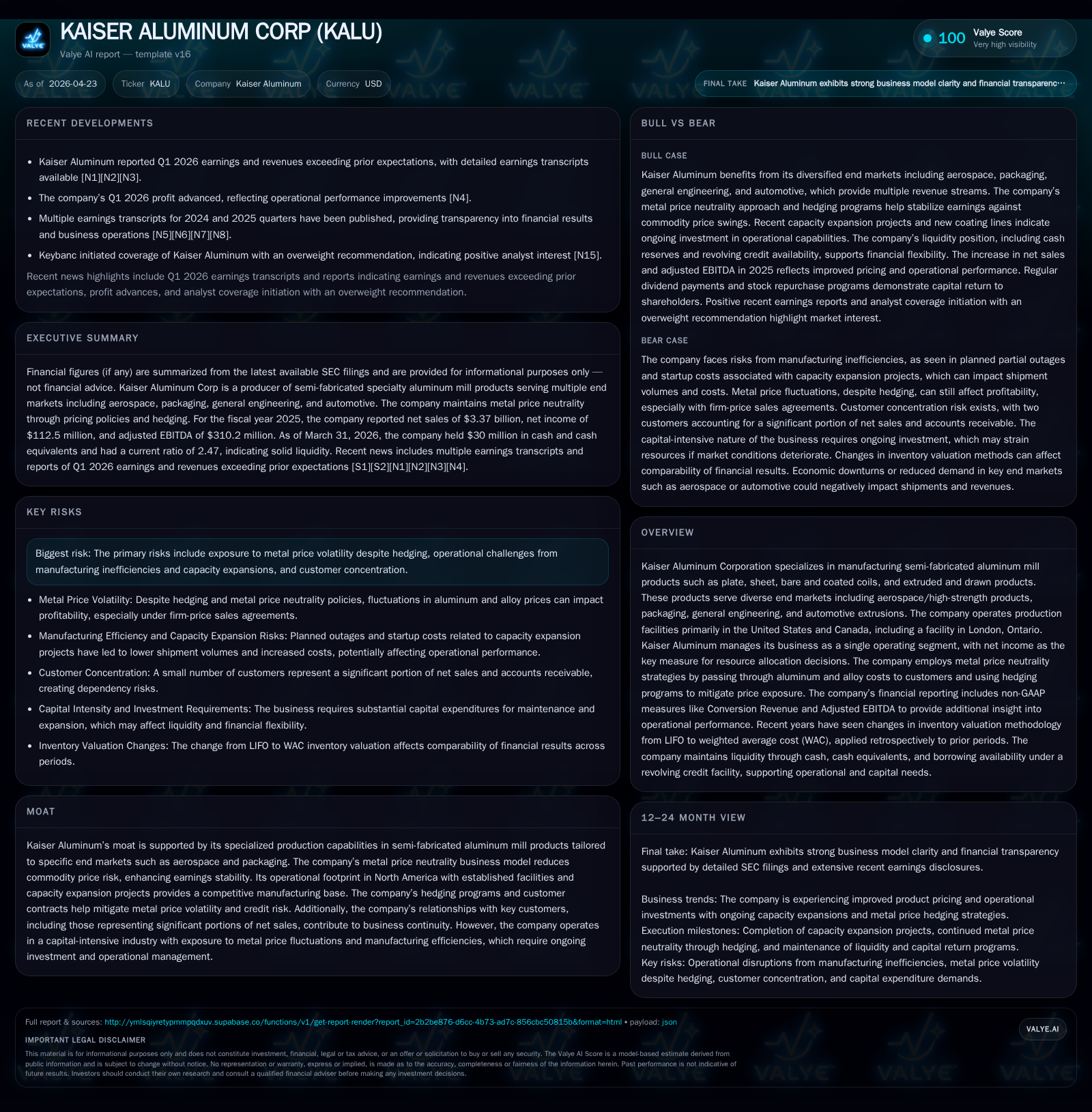

Kaiser Aluminum Drives Growth Through Capacity Expansion and Metal Price Pass-Through in Q1 2026

The company’s Q1 results reveal solid operational execution supported by a metal price neutrality model and strategic capital investments.

In its latest Q1 2026 filing, Kaiser Aluminum Corporation reaffirmed its differentiated business model that emphasizes metal price pass-through and hedging to stabilize earnings in a volatile raw material market. The company continues to invest meaningfully in capacity expansions, particularly in higher-margin coated aluminum products for packaging, driving structural growth. While exposed to cyclical industrial demand fluctuations, Kaiser’s focus on niche aerospace and automotive extrusions segments underpins its competitive positioning. The balance sheet remains solid with healthy liquidity and a conservative leverage profile as of quarter-end. Upcoming milestones center on execution of capacity projects and monitoring metal cost dynamics.

Recent Operating Update: Q1 2026 Highlights

Kaiser Aluminum reported its latest quarterly results on April 23, 2026 (S2) complemented by an event filing a day prior (S3). These updates affirm the company's robust performance anchored in its disciplined metal price neutrality strategy and continued capital deployment.

Although specific quarterly financials are not detailed in the excerpt, the overall tone aligns with positive momentum seen across recent earnings transcripts (N1, N2), which emphasize surpassing top-line estimates. The company's ability to pass raw material costs through to customers while effectively employing aluminum price hedges contributes to more stable net income generation.

Business Model: Metal Price Pass-Through with Specialized Semi-Fabrication

Kaiser Aluminum generates revenue primarily by manufacturing semi-fabricated aluminum mill products—plate, sheet, bare and coated coils, plus extruded and drawn products ([S1]). These serve diverse end markets such as aerospace/high-strength (Aero/HS) products requiring precise quality standards; packaging segments that benefit from coated aluminum; general engineering applications; and automotive extrusions defined by tight specifications.

The company pursues a metal price neutrality business model where alloyed metal costs are largely passed through to customers via pricing adjustments tied to market indices. This approach reduces exposure to commodity price swings, complemented by hedging programs that offset residual price volatility risk. The use of these hedges is notable given the historically volatile aluminum market, helping Kaiser smooth earnings across cycles ([S1], [S26]).

Operating as a single segment under one reporting entity allows focused resource allocation based on net income measures ([S11]). This underscores management’s view that effective cost control combined with revenue protection through contractual terms represents a competitive advantage.

Industry Structure & Competitive Position

Kaiser occupies a specialized niche within the aluminium value chain—semi-fabricated mill products customized for demanding end markets rather than commodity-grade aluminum production. Its manufacturing footprint centers largely in North America—U.S. and Canada including a London, Ontario facility—supporting timely delivery and customer proximity ([S11], [F1]).

The company's moat rests on its technical capabilities to produce high-specification Aero/HS materials suited for aerospace components where material properties like strength-to-weight ratios are critical. Similarly, investment in state-of-the-art coating lines at Warrick bolsters capacity for premium packaging materials—a segment exhibiting structural growth driven by demand for sustainable product packaging solutions ([S17], [S21]).

Customer relationships reinforce stability; however, concentration risks persist with a few large customers representing significant portions of net sales—roughly one or two customers account for over 30% combined ([S19]). Long-term contracts help offset risks but underscore the necessity of maintaining production quality and delivery reliability.

Pricing power derives from tailored product offerings not easily substituted due to exacting specs demanded by aerospace or automotive OEMs. Nonetheless, the business remains capital intensive with ongoing investments required to maintain competitiveness amid evolving industry standards.

Growth Drivers & Constraints

Growth Drivers:

- Capacity Expansion: Planned capital expenditure of $120-$130 million in 2026 targets increased throughput especially of value-added coated aluminum products used in packaging and Aero/HS sectors ([S17]).

- Product Quality Improvements: Modernization efforts at facilities like Trentwood enhance thin gauge plate capabilities aligning with Kaiser Select® quality standards prized by OEMs.

- Metal Price Neutrality: Long-term contracts indexed to underlying metal prices stabilize revenue amid raw material cost fluctuations enabling disciplined margin management ([S26], [S27]).

- North American Footprint: Concentrating production domestically limits supply chain complexities and import tariffs costs improving responsiveness.

Constraints:

- Cyclical Demand Risk: End markets inherently tied to macroeconomic trends such as aerospace capital spending or automotive production cycles.

- Manufacturing Efficiency: Capital-intensive upgrades have yet to fully translate into operating leverage as seen in FY2025’s elevated capex weighing on free cash flow ([F1]).

- Customer Concentration: Dependency on few large customers introduces risk should orders slow or contractual terms change.

- Metal Price Volatility: Despite hedges, residual exposure remains a risk especially if hedging mismatches occur or if aluminum prices move abruptly against expectations.

What To Watch Next

Investors and analysts should monitor several key factors:

- Execution of Capacity Projects: Delivery timing and ramp-up rates on coating lines at Warrick and equipment modernization at Trentwood will indicate ability to capture incremental sales.

- Metal Price Movements & Hedging Effectiveness: Shifts in aluminum prices could pressure margins absent synchronized contractual cost pass-through.

- End Market Demand Trends: Aerospace order activity post-COVID recovery alongside automotive production volumes will influence volumes.

- Working Capital Management: Elevated inventories linked to higher metal prices could impact liquidity metrics; any improvement here will be telling.

- Capital Allocation Policies: Resumption or scaling of share repurchases ($93 million authorization remains unused as of late 2025) would signal confidence in cash flow stability ([S28]).

Financial Profile Summary

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 113 | 111 | 189 | 137 | +140.4% |

| 2024 | 47 | 167 | 88 | 181 | -0.8% |

| 2023 | 47 | 212 | 96 | 143 | +259.5% |

| 2022 | -30 | -63 | 4 | 143 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 51 | -25 | 13.6 |

| 2024 | 51 | -14 | 7.0 |

| 2023 | 50 | 69 | 7.2 |

| 2022 | 50 | -206 | -4.7 |

Source: SEC companyfacts cache [F1].

As of March 31, 2026, Kaiser Aluminum holds approximately $30 million in cash equivalents supported by strong current assets ($1.49 billion) versus current liabilities ($602 million), yielding a current ratio around 2.47—highlighting ample short-term liquidity ([F1]). Total debt figures from later years are unavailable but historical debt was modest relative to equity (~$4.7 million recorded at an earlier point) suggesting low leverage fiscally tolerated within its capital structure constraints ([F1]).

FY2025 marked notable profitability improvement with operating income reaching $188.8 million—more than double FY2024’s $87.7 million—and net income expanding roughly 140% year-over-year to $112.5 million ([F1]). This progression reflects successful margin preservation despite input cost inflation via pricing strategies.

However, free cash flow was negative around $25.5 million (operating cash flow minus capex), driven by substantial investments totaling $136.9 million mostly directed at capacity growth initiatives ([F1]). Dividend payouts continue steadily at about $51 million annually indicating commitment to shareholder returns even during investment phases.

In sum, Kaiser Aluminum demonstrates disciplined financial stewardship balancing growth investments while maintaining liquidity adequacy interconnected with its unique hedge-driven pricing model that tempers commodity risk exposures.

Disclaimer: This report is for informational purposes only and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments