Kodiak AI Sets Autonomous Trucking Milestones Despite Intensifying Losses

Kodiak AI advances its autonomous trucking deployments and Driver-as-a-Service model amid sharply widening losses and operational cash flow challenges.

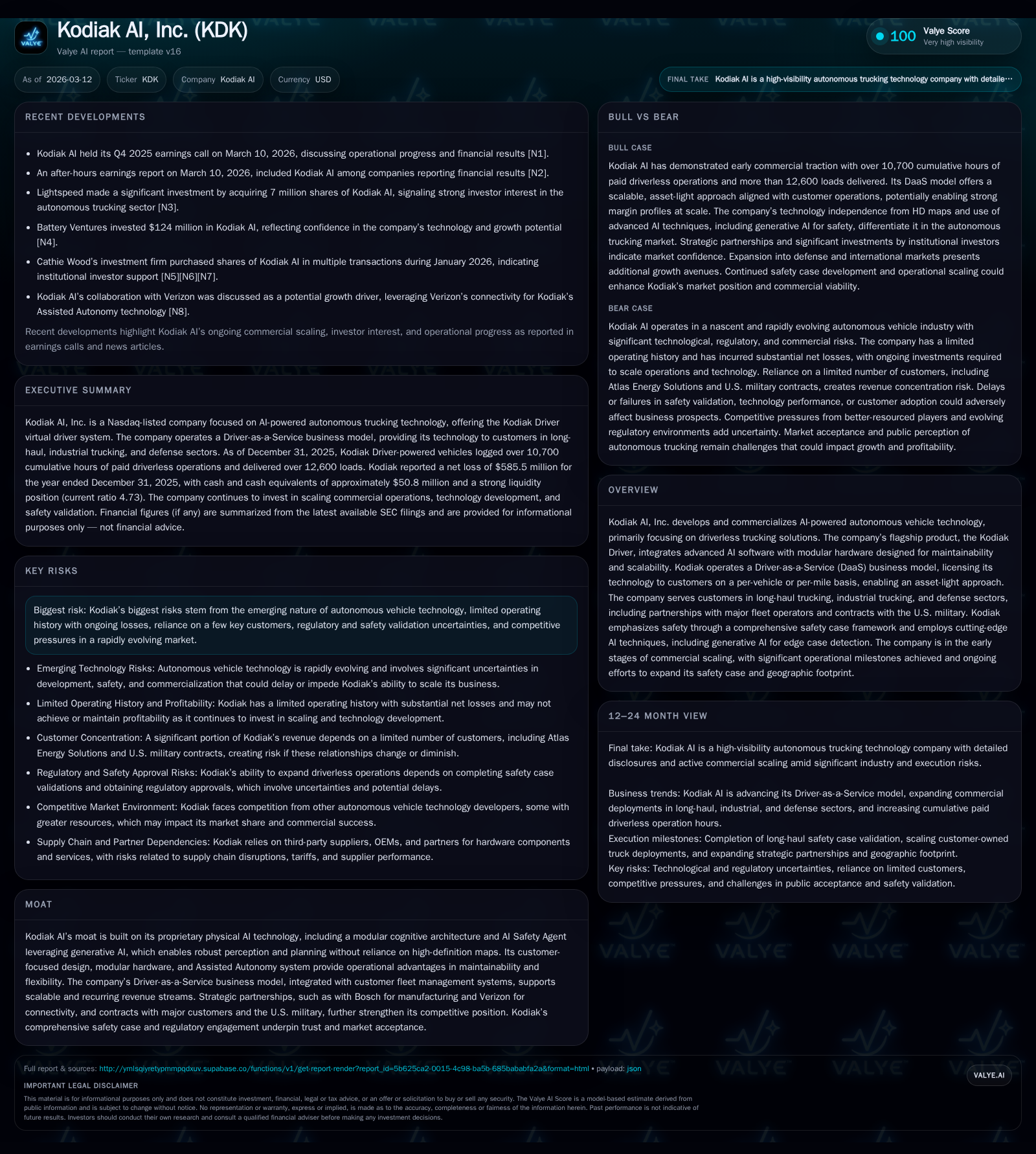

Kodiak AI has achieved significant operational milestones in commercializing its autonomous trucking technology, with over 10,700 paid driverless operation hours and more than 12,600 loads delivered by year-end 2025. The company's proprietary physical AI architecture differentiates it in the AV space through modular hardware and generative AI-based safety systems, enabling scalable deployment without reliance on high-definition maps. Kodiak’s asset-light Driver-as-a-Service business model targets recurring revenue via per-mile or per-vehicle licensing for customer-owned fleets. However, these advances coincide with escalating financial pressure, including a net loss of $585.5 million and operating cash flow deficit near $94.4 million in 2025, reflecting the capital-intensive early stage of scaling. Continued customer concentration, regulatory uncertainty, and heavy R&D investment pose risks as Kodiak strives to maintain momentum toward profitability.

Growth Trajectory: From Early Promise to Rapid Operational Expansion

Kodiak AI marked an important milestone by deploying customer-owned and operated autonomous trucks commercially starting December 2024, with its Kodiak Driver powering vehicles across long-haul and industrial trucking sectors. As of December 31, 2025, these trucks cumulatively logged over 10,700 hours of paid driverless operations and delivered upwards of 12,600 freight loads [S1][S2]. This represented a robust increase from about 5,200 cumulative hours reported as of September 30, 2025 [N1][S2], underscoring accelerating operational traction. The company also reported surpassing three million autonomous miles driven across deployments.

However, this rapid operational expansion comes alongside steep financial deterioration. Operating income plunged from -$1.78 million in FY2024 to -$38.7 million in FY2025—a year-over-year drop exceeding 2,000% [F1]. Meanwhile net income swung from positive $25.99 million in FY2024 to a net loss of $585.5 million in FY2025 (a decline exceeding 2300%) largely due to significant non-cash losses tied to financing activities [F1][S19]. Such dynamics illustrate that while Kodiak is scaling use cases and deployments swiftly, cost structures remain weighted heavily toward continued development investment.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -586 | -94 | -39 | -2353.2% |

| 2024 | 26 | -1 | -2 | +53.6% |

| 2023 | 17 | -1 | -1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 206.9 |

| 2024 | -117.9 |

| 2023 | -83.5 |

Source: SEC companyfacts cache [F1].

Operating income and net income show drastic declines due to intensified scaling and fair value accounting effects; negative cash flow reflects ongoing ramp-up expenses.

Technology Edge: Physical AI Without HD Maps Driving Flexibility

Kodiak’s core technological advantage lies in its proprietary physical AI platform termed the "Kodiak Driver," which combines advanced AI software powered by multiple parallel neural networks with modular vehicle-agnostic hardware [S1][N1]. Crucially distinctive is Kodiak's independence from industry-standard high-definition mapping—a common bottleneck for scalability—enabling flexible deployment across diverse truck models without reliance on pre-mapped routes.

This "virtual driver" system integrates an AI Safety Agent that leverages generative AI techniques for edge case detection—critical for safe operation amid unpredictable driving scenarios [S1]. Modular hardware design ensures improved vehicle uptime via maintainability enhancements compared to competitors relying on monolithic stacks. Taken together with remote assistance capabilities within an Assisted Autonomy framework [N1], Kodiak’s physical AI architecture fosters vehicle-agnostic adaptability and operational resilience.

DaaS Business Model: Aligning Customer Operations with Recurring Revenue

Kodiak operates predominantly under a Driver-as-a-Service model initiated in late 2024 through its partnership with Atlas Energy Solutions [S1][S2]. This approach licenses the Kodiak Driver technology via flexible fee arrangements—either on a per-vehicle or per-mile basis—embedded directly into customers’ fleet management systems.

By focusing on customer-owned vehicles rather than capital-intensive fleet ownership by Kodiak itself, this asset-light model enhances capital efficiency while aligning revenues directly with operational utilization rates [S1]. This structure targets predictable recurring revenue streams supporting scalable growth as customers expand autonomous-enabled fleet deployments. The integration within partner-operated logistics workflows also facilitates smoother adoption curves across complex freight networks [S2].

Financial Performance Review: Escalating Losses Amid Scaling Efforts

Financially, Kodiak manifests classic early-stage scaling characteristics alongside unusual magnitude of losses stemming from substantial investment activities tied to becoming public and expanding operations.

Operating income fell sharply to a deficit of $38.7 million for full-year 2025 from a negative $1.78 million the previous year [F1], impacted by increased R&D expenditure targeting innovation around physical AI software and hardware advancements [S19][S20]. Net loss widened ominously to $585.5 million primarily attributable not only to operating deficits but also accounting charges including large changes in the fair value of financial instruments issued during capital raises [F1][S19].

Operating cash flow was deeply negative at nearly $94.4 million in FY2025 versus just under $0.93 million negative in FY2024—reflective of growing headcount-related costs and higher overheads needed for DaaS commercial deployment infrastructure support [F1][S19].[N1]

Approximately computed ROE appears anomalous due to negative equity base but signals extreme losses absorbing invested capital quickly (approximate ROE at negative ~207%) [F1].

Capital Allocation and Balance Sheet Health: Cash Position vs Burn Rate

At December-end 2025 Kodiak held cash and equivalents totaling roughly $50.8 million alongside current assets near $126 million against current liabilities near $26.7 million yielding a conservative current ratio of approximately 4.73x [F1], indicating short-term liquidity adequacy.

However, the company's balance sheet reflects a large accumulated equity deficit near -$283 million after losses accumulated over recent years—highlighting persistent funding needs amid heavy operating cash consumption [F1][S4][S6].

Kodiak has not initiated dividends or share repurchases as expected given its early commercialization stage and sustained multi-hundred-million-dollar losses [F1][S6]. Instead capital allocation continues prioritizing R&D investments alongside scale-up expenditures linked to product deployment capacity expansion.

The company’s credit facilities impose restrictive covenants limiting certain corporate actions including dividend payments or additional indebtedness without lender consent , reinforcing prudent liquidity management imperatives.

Market Demand and Customer Concentration Risks

Kodiak's business currently centers on long-haul trucking as well as industrial trucking and defense sectors where autonomous solutions promise enhanced safety and efficiency [S1][S18]. Its first major commercial customer is Atlas Energy Solutions operating oilfield logistics vehicles powered by the Kodiak Driver deployed since December 2024—the inaugural customer-owned autonomous trucks under their operational control globally.

Additionally, the company holds contracts supporting U.S. military applications leveraging ground autonomy technologies aligned with national security objectives [S1][N4].

Such specialization concentrates revenue dependency among few critical customers increasing counterparty risk exposure should contract terms change or renewal delays arise impacting top-line visibility [S18][N4]. This limited diversification remains a material risk factor during this nascent scaling phase.

Regulatory and Safety Frameworks: Foundations for Trust and Scale

Safety underpins Kodiak’s commercial strategy reflected through an extensive safety case framework that incorporates multi-layered validations centered on their physical AI-enabled Safety Agent leveraging generative AI algorithms for proactive issue detection [S27][N1].

The regulatory landscape remains fluid for autonomous trucking requiring sustained engagement with authorities addressing liability allocation, safety validation standards, and compliance pathways before achieving broad market certification [S27]. By emphasizing transparent safety demonstration data tied closely with their operational deployments, Kodiak aims to cultivate regulatory trust facilitating incremental expansions across jurisdictions.

This is critical given potential reputational damage inherent to AV technology failures broadly acknowledged within the sector.

Competitive Set and Differentiators in Autonomous Trucking

Kodiak competes mainly against other AV technology providers focusing on freight transportation domains though most rivals rely extensively on costly high-definition mapping techniques potentially limiting cross-platform adaptability [S17][N3].

Partnerships formed such as manufacturing alliance with Bosch leverage established OEM processes enhancing unit production economy-of-scale prospects while Verizon collaboration ensures enhanced real-time connectivity integral for remote monitoring critical to their Assisted Autonomy framework [S17][N1].

Technological differentiation stems from Kodiak's multi-modal physical AI integrating neural nets capable of dynamic edge case detection reducing latent risk profiles vis-à-vis competitors reliant on map-centric navigation stacks.

Outlook and Key Milestones to Monitor

Explicit forward guidance remains limited beyond ongoing intentions articulated around scale-up initiatives including:

- Increasing paid driverless operation hours beyond current >10k thresholds;

- Expanding load deliveries while onboarding new commercial customers beyond Atlas;

- Progression toward profitable unit economics through improved operating leverage;

- Continuous product evolution enhancing modularity and safety agent functionality;

- Navigating evolving regulatory environments supportive of wider deployment;

- Managing liquidity runway potentially supplemented by equity or debt financings advised by recent financings totaling over $170M at IPO plus strategic investment injections like Battery Ventures’ recent bets amounting over $124M reported earlier this year [N4][N1]; and greater recurring revenue emergence within DaaS offerings integrating deeply into customer ecosystems. Monitoring execution against these milestones will provide critical signals regarding Kodiak's trajectory toward commercial viability balanced against structural financial risks outlined here.

Disclaimer: This report is prepared for informational purposes only; it does not constitute investment advice nor a solicitation to buy or sell securities. All data used herein are sourced exclusively from publicly available filings and verified disclosures as cited.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments