Kustom Entertainment Reshapes Focus with Video Solutions Divestiture and TicketSmarter Growth

Recent filings reveal Kustom Entertainment's strategic pivot towards entertainment platforms, as it pursues divestiture of its legacy video solutions segment.

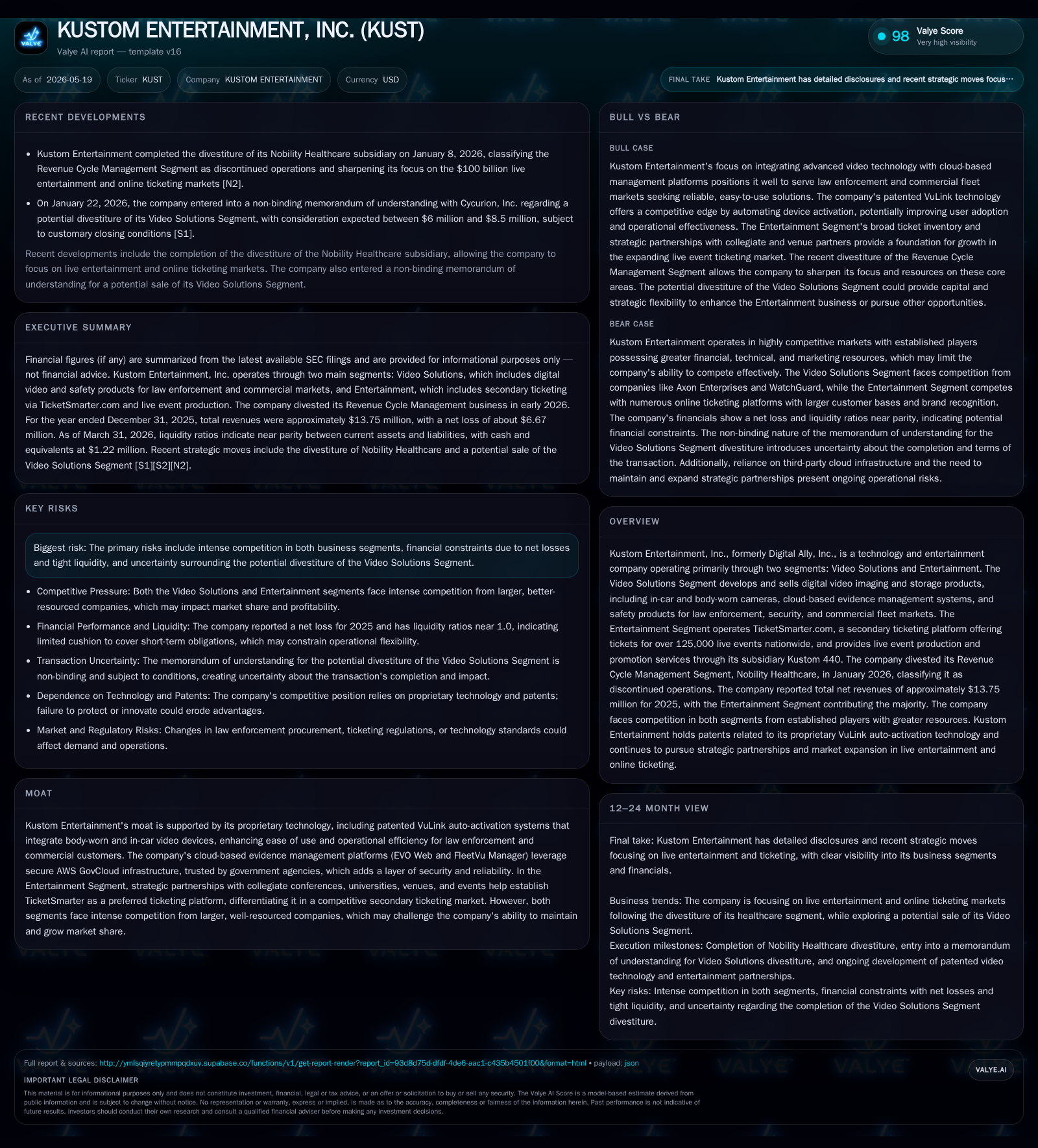

In its latest 10-Q filing dated May 15, 2026, Kustom Entertainment, Inc. continues the transition from its traditional video technology roots toward a concentrated focus on its entertainment operations, especially the TicketSmarter secondary ticketing platform. The company advanced a non-binding agreement to divest its Video Solutions Segment, highlighting a strategic shift amid persistent financial losses. The Entertainment Segment now dominates revenue streams, driven by TicketSmarter's expansive event inventory and live event promotion through subsidiaries like Kustom 440. While competition and liquidity remain risks, the company’s cloud-based technologies and partner networks provide strategic leverage in their respective markets.

Recent Operating Update

Kustom Entertainment’s latest 10-Q filing dated May 15, 2026 firmly reinforces the company's ongoing corporate restructuring and refocus efforts. A pivotal development is the status of a non-binding Memorandum of Understanding (MOU) entered with Cycurion for the contemplated sale of the company’s Video Solutions Segment [S2][S3]. While definitive agreements have yet to be signed, this step signals an imminent transition away from legacy digital video imaging products toward strengthening the entertainment segment portfolio.

This quarter also follows the January 2026 closing of the sale of the Revenue Cycle Management segment (Nobility Healthcare), as previously disclosed [S1]. Consequently, Kustom now reports only two reportable segments: Video Solutions and Entertainment [S1]. Financially, the quarter reflects tight liquidity; cash & equivalents stand at approximately $1.22 million versus current liabilities near $9.46 million, yielding a current ratio around 0.99 [F1]. Although this level approaches short-term balance sheet stress, net debt remains negative due to minimal long-term debt reported [F1].

The company also implemented a reverse stock split alongside a capital stock reduction effective April 22, 2026, reducing authorized shares from over 66 million to approximately 13 million shares—primarily a compliance and market structure move rather than fundamentally dilutive or accretive [S3][S29]

Business Model

Kustom Entertainment operates through two principal segments:

Video Solutions Segment: This legacy business designs, manufactures, and sells end-to-end digital video solutions such as in-car dash cameras (EVO-HD), body-worn cameras (FirstVu series), integrated systems (VuLink auto-activation technology), plus associated software including EVO Web—a cloud-based evidence management system leveraging AWS GovCloud infrastructure targeted at law enforcement agencies and commercial fleets. Revenue arises mainly from hardware sales recognized at delivery supplemented by recurring subscription models for cloud storage and warranty services extending over multi-year contracts [S1][S12][S28]. Additionally, it sells Shield™ branded disinfectant and personal protective equipment products.

Entertainment Segment: Comprising TicketSmarter.com—a secondary ticket marketplace offering tickets for upwards of 125,000 live events including concerts, sports, theatre—and subsidiary Kustom 440 which manages live event production and promotion such as music festivals [S1][S12][S28]. TicketSmarter generates revenues primarily from service fees calculated as percentages of ticket face value during resale transactions together with direct ticket sales from company-held inventory obtained via direct purchase or sponsorship arrangements. Key expenses for this segment entail ticket costs (inventory), payment processing fees, platform maintenance, and administrative overheads

This bifurcation illustrates a hybrid technology-product plus service model with contrasting monetization methods: hardware plus SaaS subscriptions on one side versus marketplace commissions plus promoted live events on the other.

Industry Structure and Competitive Position

Video Solutions Segment:

This sector sits within law enforcement technology and commercial fleet safety markets which demand rugged hardware backed by secure digital data ecosystems compliant with stringent regulatory requirements for evidentiary integrity.

Kustom’s competitive differentiation rests heavily on proprietary technologies like VuLink which enable seamless automatic activation between body-worn devices and vehicles improving operator ease-of-use—a nontrivial switching cost factor fostering customer retention. Moreover, their cloud-based management tools hosted on AWS GovCloud provide trusted security certifications valued by government clients. However, they face competition from larger incumbents offering broader integrated security solutions or cheaper components enabled by scale economies.

Customer concentration risks appear moderate; supply relationships with multiple component vendors limit raw material exposure though rising semiconductor prices and tariffs contribute cost pressures unavoidable industry-wide [S11].

Entertainment Segment:

Secondary ticketing platforms represent a highly competitive landscape dominated by well-funded companies boasting deep venue partnerships and user traffic scale advantages that drive liquidity on both buyer/seller sides.

TicketSmarter differentiates via its expansive live event catalog exceeding 125k events annually across genres complemented by its vertically integrated live event production arm (Kustom 440). This synergy provides cross-promotional channels potentially boosting customer acquisition beyond pure ticket resale margins.

Pricing power stems largely from service charges applied on face value transactions; however, platform competition drives continuous innovation needs to maintain fee structures without alienating users given low switching costs inherent in online marketplaces.

Growth Drivers

Video Solutions Growth Potential hinges on securing new law enforcement contracts adopting next-generation body-worn cameras with enhanced features like full HD streaming (FirstVu Pro), durability standards compliance (MIL-STD-810G), and mobile connectivity integration enabling fleet telematics expansion [S26]. Cloud subscription models offer recurring revenue streams increasing customer lifetime value.

Entertainment Expansion Dynamics center on broadening TicketSmarter’s user base through expanded live event offerings leveraging synergies with Kustom 440’s production capabilities facilitating exclusive event access. Digital innovation improving platform user experience can drive higher conversion rates while partnerships with collegiate conferences and venues create barriers against entrants.

The planned divestiture of Video Solutions would allow reallocation of capital to scale entertainment operations more aggressively either organically or via acquisitions—accelerating growth trajectory aligned with market demand for digital live experiences.

Risks / Watchpoints / Growth Constraints

Divestiture Uncertainty: The MOU with Cycurion is non-binding subject to numerous conditions including due diligence completion; failure or delay could maintain drag from legacy segments impeding simplified corporate focus [S5][S8][S9].

Financial Losses & Liquidity: Continued operating losses pressure cash flow availability restricting investments needed for innovation or marketing expansion; current near-unity current ratio underscores tight working capital [F1]

Intense Competition: Both segments face well-capitalized competitors: established law enforcement tech providers in Video Solutions; major online ticket marketplaces in Entertainment; this threatens pricing power and customer share gains.

Legal Proceedings: Various ongoing lawsuits cover contract disputes affecting subsidiaries that could result in contingent liabilities or distraction for management [S13][S27]

Raw Material Cost Inflation: Semiconductor price volatility combined with tariffs escalates production costs impacting gross margins despite mitigation efforts [S11]

What to Watch Next

Progress toward executing definitive agreements finalizing the Video Solutions divestiture will be critical for clarity on strategic direction and potential capital inflows.

Quarterly performance updates focusing on TicketSmarter’s order volumes, active user metrics, average transaction values, channel expansions into additional event categories or territories provide actionable insights into entertainment segment scalability.

Timing impact analyses regarding operational integration post-Nobility Healthcare sale should clarify cost savings vs incremental investment needs supporting refocused growth.

Legal case resolutions could affect contingent risk profiles or influence management bandwidth allocation away from core business execution.

Financial Profile Summary

As of March 31, 2026 balance-sheet data shows cash & equivalents at approximately $1.22 million juxtaposed against total debt estimated at $141 thousand end-2024 periods based on available data leading to net negative net debt positioning reflecting low leverage levels [F1]. Current assets approximate $9.4 million nearly equal to current liabilities totaling about $9.46 million yielding a current ratio just below one indicating working capital constraints requiring close management attention [F1]. Last full-year results reported net losses nearing $6.7 million consistent with continued operating income deficits signaling persistent profitability challenges amid restructuring efforts [F1].

Disclaimer: This analysis is strictly informational without investment advice or research views. It synthesizes publicly available regulatory filings and related disclosures to outline factual operating contexts along with grounded analytical perspectives respecting company-specific data boundaries stated herein.

Financial position in context

As of 2026-03-31, companyfacts shows $1224321 in cash and equivalents [F1]. Current assets of $9mm and current liabilities of $9mm imply a current ratio near 0.99x for 2026-03-31 [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments