Ladder Capital Corp: Resilience and Adaptability in U.S. Commercial Real Estate Finance Entering 2026

Ladder Capital blends credit discipline with capital flexibility to navigate complex market dynamics amid evolving commercial real estate finance conditions.

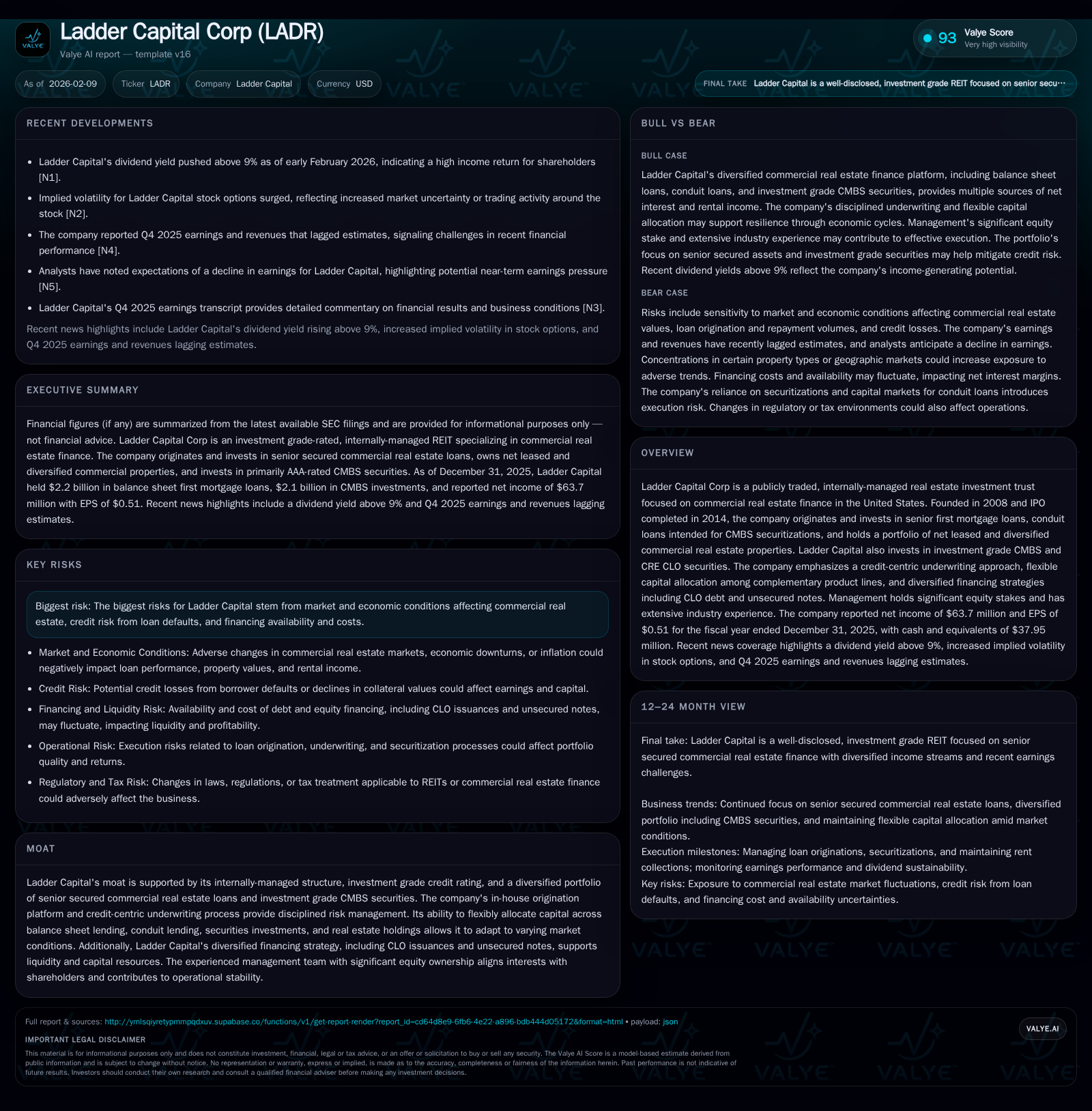

Ladder Capital Corp operates as an investment grade-rated, internally-managed REIT specializing in commercial real estate (CRE) finance, with a diversified asset portfolio spanning loan origination, conduit loans for CMBS securitization, securities investments, and net leased properties. While its Q4 2025 earnings fell short of expectations, the company maintains a robust credit-centric underwriting philosophy combined with versatile capital deployment strategies. Ladder’s diverse financing mix, experienced management team with significant equity stakes, and adaptive capital reallocation position it to address credit and market volatility risks inherent in the CRE cycle. Market signals such as heightened dividend yields and rising implied volatility underscore investor caution amidst shifting sector fundamentals.

Inside Ladder Capital: An Integrated Commercial Real Estate Finance Platform

Founded in 2008 and publicly listed since 2014, Ladder Capital Corp describes itself as an investment grade-rated internal management REIT focused squarely on U.S. commercial real estate finance [S1]. The firm's business model hinges on originating senior first mortgage loans — both fixed and floating rates — along with conduit loans intended for packaging into commercial mortgage-backed securities (CMBS). Complementing these lending activities are strategic investments in predominantly investment grade-rated CMBS securities secured by similar first mortgage loans, alongside ownership of net leased commercial real estate assets.

This diversified approach allows Ladder to combine balance sheet lending stability with fee-generating conduit origination volume and recurring income from owned properties. Since inception through end-2025, Ladder has originated over $31 billion in commercial real estate loans while acquiring $16 billion in loan-secured securities and about $2 billion in net leased properties [S1]. Notably, it has cemented its status as one of the largest non-bank originators into U.S. CMBS pools by volume.

The in-house origination platform paired with credit-centric underwriting practices distinguishes Ladder from many market participants who may rely heavily on external pipeline sourcing or less detailed credit screening. The internalized control over loan approval standards enables nimble risk assessments tailored to current market realities.

Financial Performance Review: Earnings, Dividends, and Market Reactions

For fiscal year ended December 31, 2025, Ladder reported a net income of approximately $63.7 million equating to diluted EPS of $0.51 [F1]. While these figures reflect profitable operations amidst volatile CRE markets, the Q4 quarter notably missed analyst estimates on earnings and revenues [N2]. During the February earnings call transcripts [N1], management acknowledged macroeconomic headwinds impacting transaction volume yet reaffirmed confidence in their underwriting rigor.

Market responses have been telling: Ladder’s dividend yield recently surged past the 9% threshold [N4], a figure attracting income-seeking investors but simultaneously signaling elevated risk perceptions. Further adding to investor caution is a spike in options implied volatility post-earnings release [N5], pointing to heightened uncertainty around near-term price trajectories.

These financial outcomes reflect a balancing act — sustained profitability through core lending offset by pressures such as slower deal flow and wider credit spreads affecting valuation adjustments across its securities portfolio.

Decoding Ladder's Credit-Centric Underwriting and Risk Management

Central to Ladder’s positioning is a disciplined underwriting framework designed to mitigate loan default risk amid cyclical commercial real estate headwinds [S1]. Their process utilizes proprietary financial models blending borrower creditworthiness analysis, property income streams evaluation, location-specific market data, and underlying asset collateral quality. This meticulous scrutiny fosters conservative risk appetite reflected in selective origination of senior secured loans often accompanied by flexible structuring options.

Moreover, active monitoring protocols enable early intervention on troubled credits through restructurings or increased provisions where necessary. While provisioning remains intrinsically challenging — especially under volatile market conditions impacting asset valuations — Ladder maintains reserves calibrated to evolving portfolio risk metrics as disclosed in its filings [S1].

Notably absent are excessive exposures to subordinated or mezzanine tranches which carry heightened loss probabilities; instead Ladder focuses largely on senior notes enhancing recoverability prospects.

Capital Allocation: Balancing Loan Originations, Securities, and Net Leased Properties

Ladder’s asset deployment strategy reflects agility refined over economic cycles — balancing capital allocation among direct balance sheet loans, conduit channels destined for securitization sales, investment-grade CMBS securities purchases for yield enhancement, and ownership of select net leased properties producing stable rental income [S1]. This mix dampens sensitivity to any single revenue stream's performance downturn.

The conduit loan segment functions not only as an originations driver but also as a recycling mechanism where completed loans are sold into securitizations enabling capital redeployment into fresh opportunities or sectors showing better risk-adjusted returns. Concurrently holding investment grade securities provides stable coupon income less exposed to borrower renegotiation risks.

Net leased real estate holdings add a layer of diversification with long-term lease structures tethered to established tenants mitigating cash flow volatility relative to pure loan portfolios.

This fluid capital reallocation capability underpins their resilience amid shifting interest rate environments or sector demand patterns typical within multifamily versus office or industrial submarkets.

Financing Mosaic: CLOs, Unsecured Notes, and Liquidity Strategies

Underpinning Ladder’s investment activity is a sophisticated financing structure relying on varied instruments tailored for cost-efficiency and liquidity stability [S1]. Collateralized Loan Obligations (CLOs) provide non-recourse debt backed by pools of commercial mortgages offering competitive funding pricing absent mark-to-market volatility impact traditional in many borrowing vehicles.

Complementing CLO issuances are senior unsecured notes that broaden the capital base beyond project-level secured borrowing enhancing structural flexibility. Additionally, committed term financing arrangements via leading financial institutions ensure access to liquidity buffers critical during periods of dislocation or tightened credit markets.

This mosaic enables Ladder not only to support new loan originations or security purchases but also ameliorates refinancing risks while maintaining compliance with regulatory capital requirements.

Management’s Alignment with Shareholders: Experience Meets Equity Skin in the Game

A standout attribute is the management team’s substantial personal equity ownership exceeding 11% of total shares outstanding coupled with an average industry experience upwards of 29 years per executive [S1]. This combination inherently aligns leadership incentives closely with shareholder interests fostering disciplined decision-making oriented toward sustainable value creation rather than short-term gains.

Chief Executive Officer Brian Harris alongside President Pamela McCormack exemplify this dynamic through transparent communication during earnings calls emphasizing both caution around macro uncertainties and confidence in underlying portfolio quality [N1].

Such alignment can serve as a stabilizing force especially in periods where external conditions test sector-wide assumptions around credit risk tolerance or capital deployment pace.

Risks in Focus: Market Dynamics, Credit Challenges, and Regulatory Pressures

Despite its diversified platform and prudent underwriting culture, Ladder faces multifaceted risks inherent in CRE finance as detailed extensively in recent SEC filings [S1]. Primary concerns encompass concentrated exposure within real estate sectors sensitive to shifts in tenant demand or geographic economic disruptions.

Credit risk remains pertinent given that loan repayments depend on factors including legal frameworks around bankruptcy protection limiting recovery avenues; property operating expenses influenced by inflationary pressures; tenant lease renewals contingent on broader economic health; and exposure to subordinate loan classes albeit limited.

Additionally influential are government policy shifts—both monetary via Federal Reserve actions around interest rates affecting borrowing costs—and political uncertainties potentially impacting market liquidity or securitization functioning. Inflation specifically compounds risks by stressing both property valuations eroding collateral cushions and increasing operating costs potentially weighing on cash flows backing loans.

Loan securitization activities bring complexity related to timing mismatches between loan sales and new originations influencing quarterly earnings noise which requires investor discernment.

Comparative Landscape: Ladder Capital Versus Peers in Value and Yield

Within the commercial real estate finance REIT space Ladder Capital is often juxtaposed against peers like Apollo Commercial Real Estate Finance (ARI). Recent analyses underscore that despite trading at a discount relative to book value multiples common among peers [N6][N7][N9], Ladder offers an attractive dividend yield exceeding 9% [N4].

This divergence highlights differing market views: some see value opportunities given resilient portfolio quality and cautious underwriting while others remain wary due to earnings misses or sector outlook uncertainties reflected partly through wider implied volatilities [N5].

Such comparative context is essential for appreciating marketplace sentiment nuances influencing share price behavior beyond headline fundamentals.

Technical Market Signals: Navigating Price Trends and Volatility Spikes

From a technical standpoint recent trading patterns evidence growing investor caution surrounding LADR shares. Breaching below key moving averages signals weakened near-term momentum [N8], while surging option implied volatilities point toward expectations of increased price swings possibly tied to ongoing macroeconomic uncertainty or event-driven investor repositioning [N5][N8].

These technical cues complement fundamental reviews by highlighting how market psychology may amplify reaction intensity when future earnings visibility dims further due to cyclical factors or regulatory developments impinging upon leveraged CRE lenders broadly.

Conclusion: Adaptive Positioning Amid Evolving CRE Finance Conditions

Navigating volatile commercial real estate finance terrain into 2026 demands more than scale — it requires integrative platforms coupled with rigorous credit assessment frameworks capable of flexibly allocating capital across complementary product lines. Ladder Capital exhibits these attributes through its internal management REIT structure combining loan origination prowess with strategic conduit selling into CMBS sectors alongside aligned leadership deeply invested personally.

While recent earnings softness triggered valuation compression visible in elevated dividend yields/phased stock volatility signals, the company’s multifaceted financing schemes underpin operational liquidity preserving optionality against tightening credit spread backdrops. Nonetheless comprehensive acknowledgment of persistent risks—credit cycles, inflationary impacts, geopolitical unpredictability—is imperative for balanced understanding going forward.

Disclaimer: This report is for informational purposes only. It does not constitute investment advice nor an offer or solicitation to buy or sell any securities. Information cited herein reflects sources available as of February 2026 but may evolve. Readers should perform their own due diligence before making any financial decisions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments