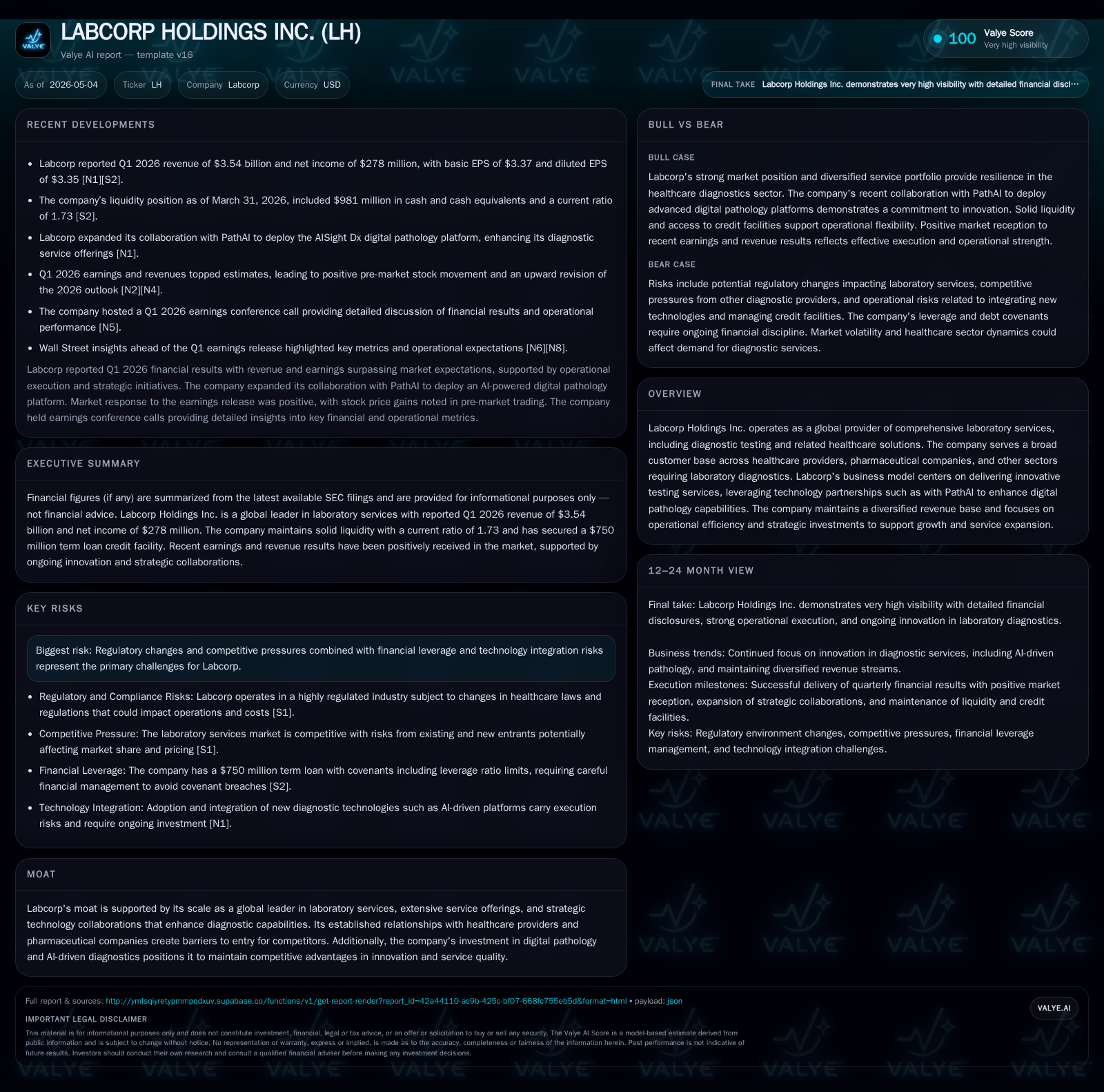

Labcorp Holdings Reports Strong Quarter as Diagnostic Innovation Drives Growth Trajectory

Labcorp’s Q1 2026 results underscore robust revenue growth and operational efficiencies fueled by strategic AI partnerships and diversified service expansion.

Labcorp Holdings delivered a solid first quarter in 2026 with revenue exceeding expectations and margin stability despite industry reimbursement pressures. The company’s ongoing investments in AI-driven digital pathology via its PathAI partnership and broad diagnostic assay portfolio reinforce its competitive moat. While regulatory and competitive pressures remain watchpoints, Labcorp’s scale, technology integration, and strong pharma collaborations underpin its growth outlook. Its financial position supports continued innovation and capacity investment.

Q1 2026 Performance Highlights

In the quarter ended March 31, 2026, Labcorp Holdings reported revenue surpassing analyst estimates, driven largely by volume increases across both its core lab testing services and pharmaceutical development segments [S2][N1]. The uplift was underpinned by a favorable shift in test mix towards more complex assays, particularly those tied to oncology and genetic diagnostics, which carry higher margins. Despite ongoing headwinds from payer reimbursement adjustments—a common industry challenge—Labcorp managed to sustain operating margins through improved operational efficiencies and cost discipline [S2][N1].

The company also highlighted progress in integrating advanced digital pathology capabilities following its strategic alliances, notably with PathAI. This integration supports faster turnaround times and enhanced diagnostic accuracy, contributing positively to customer retention and new contract acquisition [S3]. Management signaled confidence in sustaining top-line momentum supported by pipeline growth and expanded assay offerings.

The April 30 event filing reinforced these operating themes while providing additional color on the acceptance trajectory of AI-driven diagnostic solutions across Labcorp's network [S3]. Market reaction was favorable, with shares advancing on pre-market trades reflecting investor approval of the stronger-than-expected earnings release [N2][N4].

Labcorp’s Business Model and Service Portfolio

Labcorp operates at the forefront of global laboratory services, providing comprehensive diagnostic testing solutions spanning routine blood work to specialized genetic assays. Its clientele encompasses healthcare providers seeking reliable diagnostics for patient care, pharmaceutical companies requiring clinical trial support, and other sectors dependent on laboratory data [S1][F1]. Revenue is generated primarily through fee-for-service arrangements where customers pay for individual tests or bundled service agreements.

A significant strength lies in Labcorp’s diversified service portfolio that balances high-volume routine testing with specialized service lines such as oncology diagnostics and companion diagnostics linked to drug development partnerships. The company's investment in AI-powered digital pathology through its collaboration with PathAI advances differentiation by enhancing test accuracy and workflow automation—critical factors for client retention in a market where switching costs are elevated due to certification requirements and integration complexity [S1].

Customer reliance on Labcorp stems from its scale-enabled nationwide laboratory network ensuring sample processing speed and quality alongside a breadth of test menus that are difficult for smaller competitors to replicate. The company strategically reinvests in technological innovations that improve diagnostic precision while expanding into emerging fields like molecular diagnostics, which offer better pricing power than commoditized assays.

Competitive Dynamics and Industry Positioning

The clinical laboratory industry remains moderately fragmented but dominated by a few large players like Labcorp whose scale confers substantial cost advantages and influence over payer negotiations. Labcorp's entrenched contracts with health systems, insurers, and pharmaceutical companies create meaningful barriers to entry for regional or niche competitors [S1].

Pricing pressure persists industry-wide due to regulatory reforms tightening reimbursement rates, increasing the need for operational efficiency gains. However, Labcorp's extensive service offering coupled with proactive adoption of new testing modalities—including advanced genomic assays—positions it well amid shifting demand profiles.

Regulatory compliance imposes ongoing complexity; however, Labcorp's experience navigating FDA oversight for test approvals provides an advantage compared to newer entrants. The company's active role in co-developing diagnostics alongside pharma clients further reinforces its market stature through collaborative innovation partnerships rather than pure price competition.

Drivers Accelerating Growth and Innovation

Key growth drivers identified include expanding AI-driven digital pathology use cases via the PathAI alliance delivering enhanced diagnostic workflows that appeal to health systems aiming to upgrade lab infrastructure [S2][N1]. Additionally, increasing demand for high-margin specialty tests aligned with personalized medicine trends fuels volume expansion.

Labcorp's R&D investments target the launch of new assays meeting evolving clinical standards while broadening pharma services offerings supporting drug development pipelines. These efforts generate incremental revenue from contract wins reflective of stronger industry outreach capabilities demonstrated in recent quarters.

Volume growth is complemented by pricing improvements within specialty segments where payers accept premium fees linked to demonstrably better patient outcomes — a shift from commoditized tests under standard reimbursements. Operational efficiencies materialized through centralized automation also contribute to margin enhancement prospects.

Risks and Constraints Impacting Future Momentum

Despite favorable trends, Labcorp faces headwinds from regulatory revisions potentially affecting reimbursement methodologies that could depress test pricing or increase compliance burdens [S1][S2]. Heightened competition from emerging labs leveraging novel business models or aggressive pricing strategies may weigh on volume gains if incumbent relationships weaken.

Another critical risk involves execution challenges integrating sophisticated AI technologies smoothly across decentralized labs without causing operational disruptions or escalating costs beyond projections.

Key Near-Term Catalysts and Market Watchpoints

Investors should monitor upcoming milestones including announcements of new commercial partnerships expanding the reach of AI-based diagnostics within hospital networks [N2]. Clinical validation data releases from pipeline assays targeting oncology or rare diseases could provide fresh demand impetus reflecting broader adoption curves.

Management updates on guidance during upcoming earnings calls will also serve as important signals regarding margin trajectory amid reimbursement landscape shifts. Observing volume trends in specialty test categories will be critical given their outsized impact on overall profitability.

Current Financial Profile Summary

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $532mm | |

| 2025-12-31 | ||

| Current assets | $4.0bn | |

| 2025-12-31 | ||

| Current liabilities | $2.8bn | |

| 2025-12-31 | ||

| Current ratio | 1.42x | |

| 2025-12-31 |

Source: SEC companyfacts cache [F1].

Labcorp's latest balance sheet reflects healthy liquidity with cash & equivalents standing at approximately $532 million as of year-end 2025 [F1]. Current assets exceed current liabilities by a ratio of about 1.42x, indicating comfortable short-term financial flexibility [F1].

| Metric | Value | Period End |

|---|---|---|

| Revenue | $13.95B | |

| 2025-12-31 | ||

| Operating Income | $1.38B | |

| 2025-12-31 | ||

| Net Income | $876.5M | |

| 2025-12-31 | ||

| Cash & Equivalents | $532.3M | |

| 2025-12-31 | ||

| Current Ratio | 1.42 | |

| 2025-12-31 |

This analysis is based solely on publicly available SEC filings up to May 4th, 2026, complemented by selected news sources; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments