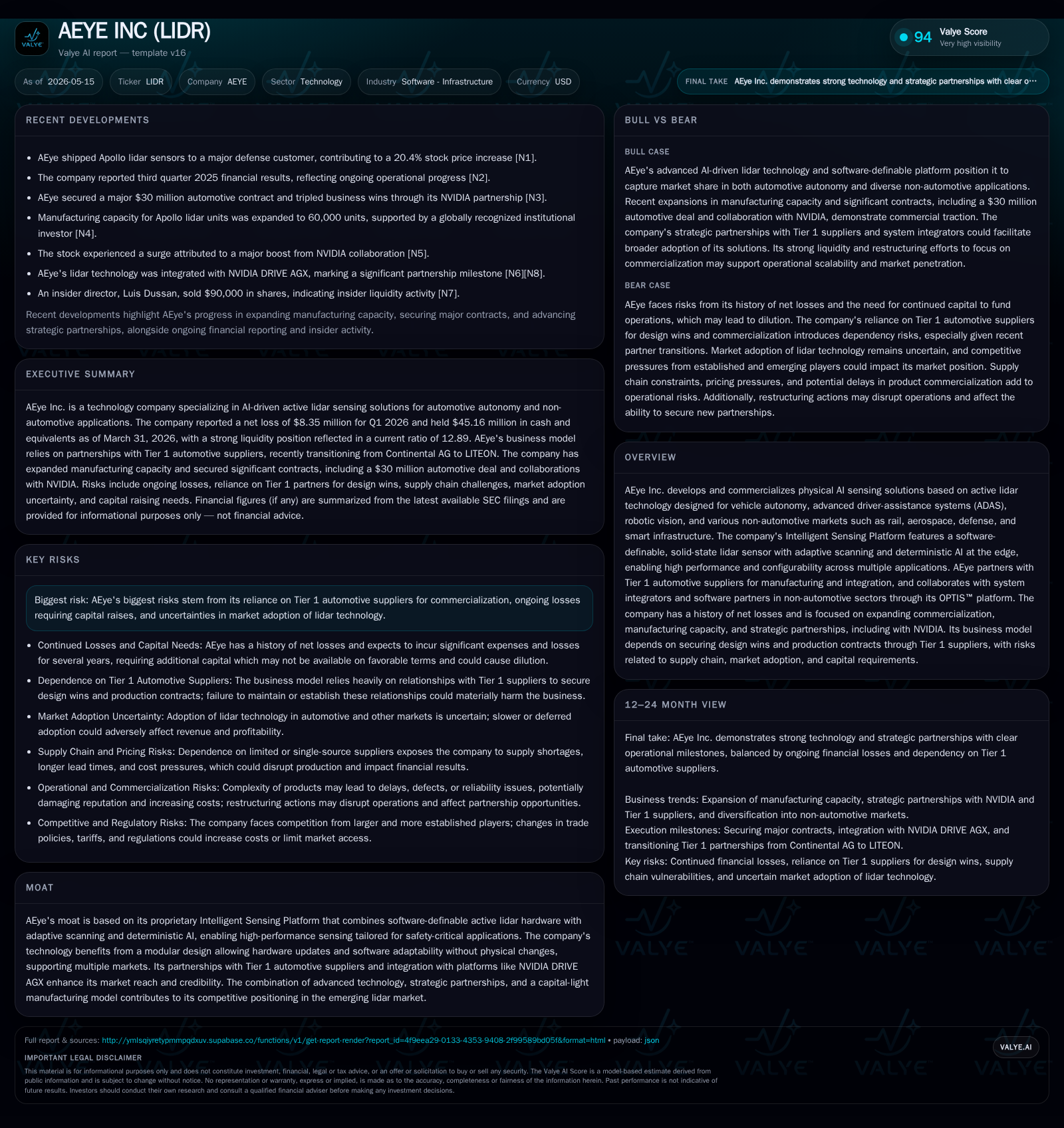

AEye Inc Strengthens Tier 1 Partnerships to Accelerate Lidar Commercialization

AEye’s latest quarterly filing underscores progress in manufacturing scale-up and supplier collaborations amid ongoing losses and market adoption challenges.

In its May 2026 quarterly report, AEye highlights advancing commercialization of its software-definable lidar platform through strengthened Tier 1 automotive partnerships and expanded manufacturing capacity. While these developments enhance prospects for broader market penetration in automotive and industrial segments, the firm continues to contend with persistent net losses and supply chain complexities. The company’s capital-light business model leveraging Tier 1s remains critical for scaling series production, but revenue expansion hinges on timely design wins and OEM engagements. Upcoming execution milestones and technological innovations will be key indicators of AEye's growth trajectory.

Latest Quarterly Operating Update: Commercialization Progress and Supply Chain Dynamics

AEye’s Q1 2026 Form 10-Q filing dated May 14 presents an operational narrative focused on advancing commercialization efforts in partnership with leading Tier 1 automotive suppliers [S2]. The company continues transitioning from legacy partnerships — most notably following Continental AG’s exit from joint lidar development in late 2023 — toward collaboration with LITEON as the new primary Tier 1 partner handling manufacturing scale-up, system integration, sales support, and OEM engagement [S18]. This strategic pivot aligns with AEye’s capital-light model that depends on leveraging Tier 1s’ industrialization capabilities rather than internalizing complex manufacturing or sales functions.

The quarterly report emphasizes ongoing ramp-up of production capacity facilitated through these suppliers. However, it also underscores lingering challenges typical for hardware startups at this stage, including supply chain uncertainties linked to limited single-source raw materials that could disrupt delivery timing and product adoption rates [S2]. Operating expenses remain elevated due to development efforts and commercialization-focused restructuring undertaken since 2023 which included workforce reductions in sales/marketing [S2][S17]. Despite these expenses shaping continued net losses with a trailing annual loss north of $33 million (net income -$33.96M for year ended Dec. '25) [F1], management is intensifying focus on progressing design wins toward binding OEM contracts.

AEye’s Business Model and Product Innovation: The Intelligent Sensing Platform

Central to AEye’s value proposition is its proprietary Intelligent Sensing Platform — a modular solution featuring software-definable active lidar hardware equipped with SmartScan adaptive scanning technology paired with deterministic AI processing performed at the edge [S1][S6]. This architecture enables dynamically configurable scan patterns tailored per application or environmental conditions without physical hardware modifications. Such software adaptability facilitates customizable performance trade-offs between range, resolution, power use, and frame rate that are essential for safety-critical autonomous driving (SAE Levels 2–5) as well as varied industrial sensing use cases.

Revenue generation stems primarily from sales of sensors integrated into vehicles through automotive Tier 1 suppliers who manufacture the components at scale then resell or integrate these into OEM vehicle platforms. Beyond automotive ADAS/autonomy applications supported by the Tier 1 channel, AEye extends its market reach via the OPTIS™ platform that incorporates third-party perception analytics enabling turnkey solutions for rail safety systems, aerospace UAV navigation support, defense sensing applications, smart infrastructure monitoring, and security sectors—all requiring long-range lidar reliability paired with environmental robustness [S6].

This dual-channel go-to-market strategy leverages automotive-grade component reliability standards while deploying modular hardware-software ecosystems that favor scalability and flexibility across sectors. The business model emphasizes partnering over direct manufacturing or distribution, reducing capital intensity but concentrating commercial risk around supplier alliances.

Industry Context: Competitive Landscape and Partnership-Driven Go-to-Market Strategy

The lidar industry has evolved markedly from niche R&D projects toward competitive ecosystems where success hinges heavily on securing Tier 1 automotive supplier partnerships that bridge OEM procurement hurdles. AEyes’ strategy of embedding its Intelligent Sensing Platform within established Tier 1 channels—exemplified by past agreements with Continental AG and current collaboration with LITEON—places it firmly within the traditional three-tier automotive supply chain model [S1][S18].

This interdependent commercial approach grants credibility through suppliers’ manufacturing scale and integration expertise but reconciles significant risks if a Tier 1 partner discontinues support or fails to convert design wins into volume orders [S7]. Additionally, non-automotive markets employ diverse system integrators utilizing AEye’s OPTIS platform for customized solutions integrating external analytics software; nonetheless these segments remain fragmented lacking centralized procurement comparable to automotive OEMs [S7].

Competition stems from other lidar vendors pursuing alternative sensing technologies such as MEMS-based scanning or flash lidar approaches. Regulatory shifts impacting vehicular ADAS sensor mandates further influence adoption timing. Supply chain constraints prevalent across semiconductor-reliant industries also weigh on both lead time predictability and component cost management—factors critical to pricing power durability amid aggressive competition [S28].

Growth Drivers: Scaling Manufacturing Capacity and Expanding Market Penetration

Several levers underpin AEye's growth trajectory:

- Tier 1 Partnership Conversion: Expanding design wins within LITEON-enabled industrialization aims to translate into confirmed OEM series production contracts generating steady volume revenue streams.

- Technology Roadmap Advancements: Enhancements in scan adaptability combined with optimized power efficiency cater specifically to highway autonomous driving applications demanding extended range performance bolstering product differentiation.

- Capital-Light Manufacturing Model: Partnering with Tier 1s reduces fixed asset investment requirements while tapping mature supplier supply chains facilitating improved unit economics as scale increases.

- Adjacent Market Expansion: Utilization of OPTIS platform partners for deploying lidar-enabled visibility solutions in rail crossing protection systems, UAV navigation safety overlays in aerospace defense contexts, cognitive infrastructure monitoring in cities, broadening addressable market beyond traditional ADAS contexts.

- Strategic Ecosystem Alliances: Collaboration with NVIDIA DRIVEX AGX platform aligns AEye’s sensor data output seamlessly within next-generation autonomous vehicle compute architectures enhancing integration convenience for OEMs.

As wafer-level integration capabilities mature reducing sensor size/costs without compromising optical performance, improved margins may emerge enabling economically competitive end-product pricing—a fundamental determinant of broad adoption across cost-sensitive vehicle models. Supply chain stabilization would further enhance delivery reliability supporting customer retention.

Risks and Constraints: Capital Needs, Supplier Reliance, and Market Adoption Uncertainties

AEye faces several notable risks:

- Dependence on Tier 1 Supplier Relationships: Given revenue concentration through a limited number of Tier 1 partners responsible for final bids to OEMs, any partnership disruption could severely impair go-to-market effectiveness or delay contractual commitments [S1][S2][S18].

- Ongoing Operating Losses Necessitate Financing: With cumulative net losses exceeding $400 million historically ([S14]), continued cash burn requires periodic capital raises posing dilution risk under restrictive "baby shelf" SEC rules limiting public float-based issuance caps during low market valuations [S17][F1].

- Supply Chain Vulnerabilities: Limited single source components expose manufacturing timelines to raw material shortages or price escalations complicating consistent product delivery potentially eroding customer confidence [S2][S5].

- Market Adoption Timing: Automotive OEM deployments of lidar remain uncertain amid evolving regulatory standards and competitive sensor technology options; slowdowns or deferrals can postpone revenue realization significantly [S24].

- Legal Contingencies: Ongoing arbitration over a disputed $3.3 million vendor claim relating to alleged defective components plus settled litigation regarding office lease obligations (~$8.5 million claim settled for $1.4 million cash plus warrants) reflect operational stress points though currently contained financially [S5][S13].

- Regulatory Compliance Risks: Evolving regulations around autonomous vehicle safety standards and electronic product radiation controls enforced by FDA require continuous compliance efforts adding complexity/cost risk exposure [S10][S25].

What to Watch Next: Design Wins, OEM Engagements, and Technology Roadmap Milestones

Key upcoming indicators include:

- Public disclosures around confirmed Tier 1 design wins progressing into binding series production contracts with major auto OEMs remain critical to credible revenue visibility.

- Expansion of the OPTIS platform implementations across rail safety projects or aerospace defense sensing integrations would validate cross-market relevance supporting diversified growth base.

- Manufacturing scale milestones evidencing increased throughput coupled with stable lead times signal readiness for higher volume demand fulfillment.

- Collaborations yielding system-level advances such as deeper NVIDIA DRIVEX platform integrations implying broader industry acceptance.

- Capital raising activities tracking earlier than expected given operating liquidity burn rates could impact investor confidence if terms become unfavorable [S2][S3].

Continuous monitoring of these milestones will be essential to assess whether technical innovation translates into commercial traction amid a competitive landscape within an evolving regulatory environment.

Financial Snapshot: Liquidity Position Supports Near-Term Operations

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $45mm | |

| 2026-03-31 | ||

| Current assets | $80mm | |

| 2026-03-31 | ||

| Current liabilities | $6mm | |

| 2026-03-31 | ||

| Current ratio | 12.89x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

AEye holds a solid liquidity position exiting Q1 ’26 with over $45 million cash against very modest current liabilities yielding a current ratio near 13x evidencing healthy short-term coverage despite ongoing operations at a loss level (-$33.96M net income trailing annual basis) requiring additional financing measures eventually if revenue ramps are delayed further [F1][S2]. The absence of debt points to an unlevered balance sheet but underscores dependence on equity issuances or convertible instruments for funding growth initiatives given negative cash flow dynamics typical at this commercialization phase.

This analysis is based solely on publicly disclosed SEC filings up to May 2026 without forward-looking investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments