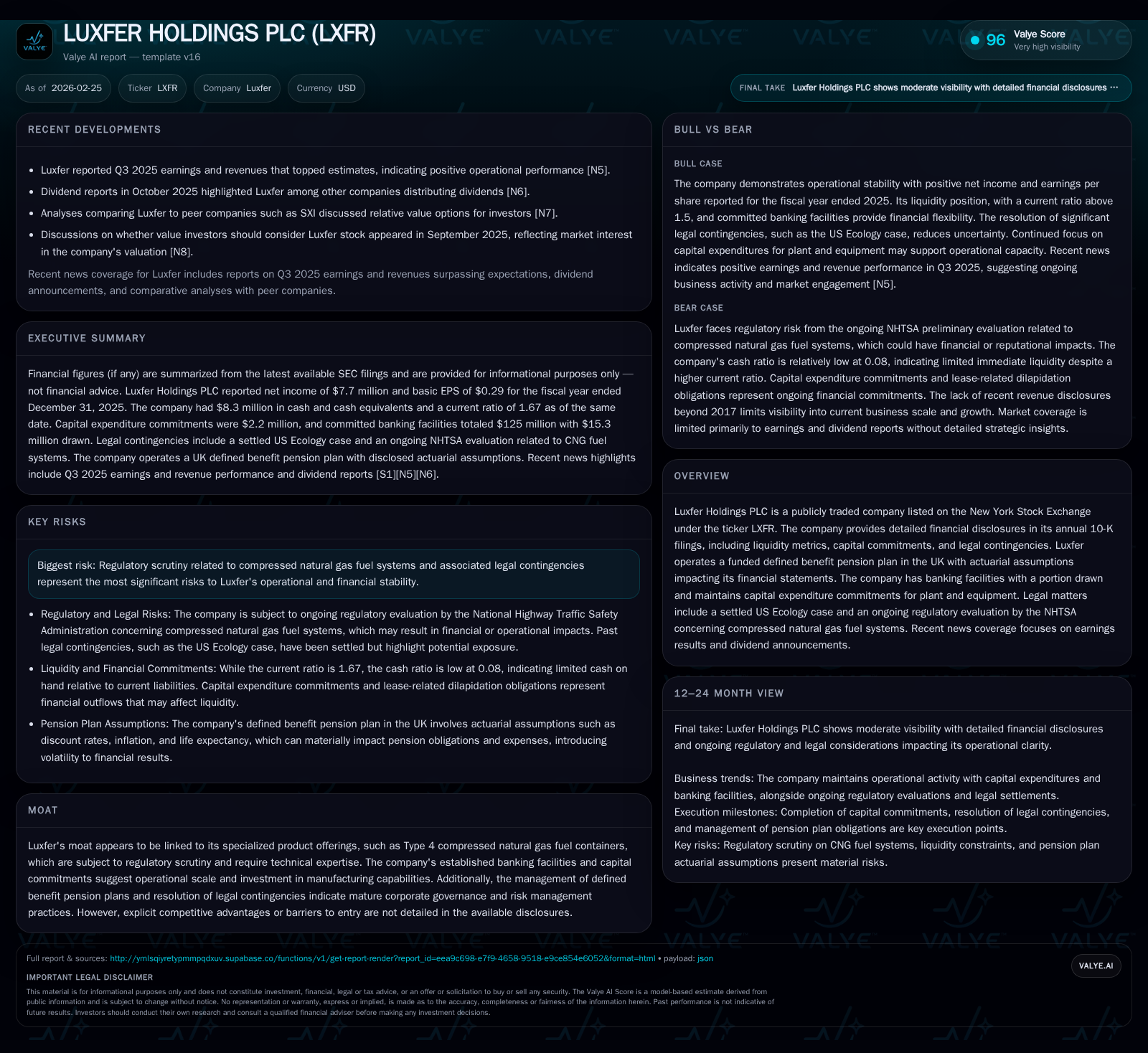

Luxfer’s Mixed Earnings and Pension Commitments Spotlight Operational Challenges

Luxfer Holdings PLC faces earnings pressure despite steady cash flow, influenced by regulatory probes and pension obligations.

Luxfer Holdings PLC reported a decline in operating income and net profit in 2025, reflecting operational headwinds within its specialized manufacturing segments. The company’s cash flows remain robust but are offset by reduced capital expenditure and ongoing regulatory scrutiny, particularly related to its Type 4 compressed natural gas (CNG) fuel containers. Furthermore, Luxfer’s management of UK defined benefit pension plans introduces accounting complexities that affect its financial position. While dividends have remained stable, buyback activity has slowed, underscoring cautious capital allocation amid profit growth challenges.

Historical Financial Trajectory and Profitability Shifts

Luxfer Holdings PLC delivered consistent revenue figures near $441 million over the period spanning 2022 to 2025 [F1], maintaining top-line stability amid sectoral fluctuations typical for specialty industrial manufacturers. However, beneath this revenue steadiness lies pronounced volatility in profitability measures: operating income climbed marginally from $10 million in 2022 to $42 million in 2023 before retreating sharply to $24 million in 2025—a decline of roughly -20.3% year-over-year [F1]. Net income trends were more volatile; from a strong $26.9 million in 2022, Luxfer slipped into a net loss of -$1.9 million in 2023 before partially recovering but contracting again to just $7.7 million in 2025—a precipitous -58.2% annual drop [F1]. This contrast signals margin compression and cost pressures that outpaced revenue growth.

Operating cash flow exhibited growth from $15.9 million in 2022 to a peak of $51.1 million in 2024 before dropping to $34 million in 2025 (-33.5%) [F1]. Despite this downturn, cash flow remains robust relative to capex, which itself fell by -24.3% from $10.3 million in 2024 to $7.8 million in 2025 [F1]. The cyclicality reflects Luxfer’s cautious reinvestment stance following operational headwinds.

These financial dynamics underscore Luxfer's position within a niche manufacturing segment demanding technical precision and regulatory compliance—often yielding episodic earnings swings despite stable revenues.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 8 | 34 | 24 | 8 | -58.2% |

| 2024 | 18 | 51 | 30 | 10 | +1068.4% |

| 2023 | -2 | 26 | 4 | 9 | -107.1% |

| 2022 | 27 | 16 | 10 | 8 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 14 | 3 | 26 |

| 2024 | 14 | 2 | 41 |

| 2023 | 14 | 3 | 17 |

| 2022 | 14 | 11 | 8 |

Source: SEC companyfacts cache [F1].

Note: Revenue values not available for all years from XBRL data tags; dividends payments rounded; Buybacks declined steeply post-2022.

Impact of Regulatory Scrutiny on Specialized Product Lines

A significant external variable impacting Luxfer’s current and future performance relates to regulatory scrutiny over its Type 4 CNG fuel containers investigated under a Preliminary Evaluation launched by the National Highway Traffic Safety Administration (NHTSA) beginning April 2025 [S1][S4][S12]. Specifically, the Office of Defects Investigation is probing allegations of fuel leaks—a critical safety issue for compressed natural gas systems integral to alternative-fuel vehicles.

Although Luxfer maintains that no unreasonable risk to motor vehicle safety exists given their technical safeguards and product design [S12], the open-ended nature of this inquiry injects uncertainty surrounding potential recall costs, liability provisions, or mandated redesigns—all capable of materially affecting earnings or capital deployment [S4].

This regulatory lens highlights inherent complexity for manufacturers operating at the intersection of specialized composites technology and environmentally sensitive market segments: compliance costs may escalate while reputational stakes intensify.

Capital Structure, Liquidity, and Pension Obligations

Luxfer’s balance sheet fundamentals illustrate disciplined liquidity management paired with moderate leverage risks [S7][S10][F1]. At December 31, 2025, committed banking facilities stood at $125 million with an additional uncommitted accordion feature worth $25 million; however, only $15.3 million was drawn—down slightly from prior-year usage—reflecting conservative borrowing amid adequate internal cash flows [S1][F1]. These credit lines mature October 2026 [S7], making facility renewal or refinancing a near-term focus.

Capital expenditure commitments increased moderately to $2.2 million in late-2025 from an unusually low level of $0.5 million during the previous year yet remain well below pre-pandemic peaks [S1]. This signals calibrated investment aligned with production efficiencies rather than aggressive expansion.

Pension obligations add another layer of financial nuance involving complex actuarial valuations tied primarily to the UK funded defined benefit plan [S1][S10]. Annual mark-to-market adjustments entail sensitivity to discount rate fluctuations (weighted average ~5.50% at end-2025), inflation expectations subject to UK index reforms transitioning RPI toward CPIH measures post-2030, and demographic trends (life expectancy increases amplifying liabilities) [S10][S15]. The last triennial valuation reported a surplus (£20.8m), an improvement on prior deficits evidencing improved asset returns or funding policies but was accompanied by volatility risks inherent to these assumptions.

Such pension accounting intricacies influence both reported earnings and balance sheet strength unpredictably year-on-year—an operational challenge amid external market stressors.

Dividend Policy and Shareholder Returns Amid Cost Pressures

Despite profitability contraction between fiscal years ending December 31st of 2024 and 2025, Luxfer preserved dividend payments near historic levels (~$14m annually) evidencing commitment to shareholder income continuity versus withholding distributions amid earnings declines [F1][S13][S17][S19].

Conversely, share repurchase activity tapered considerably—from over $11m spent on buybacks four years ago (FY22) down sharply below $3.1m most recently—highlighting management’s deliberate preservation of liquidity amid uncertain profit trajectories and regulatory pressures.

Given reported equity approximating $226m at FY25-end with net income around $7.7m yields ROE near a modest ~3.4%, capital returns appear constrained relative to equity base size reflecting operational profitability challenges within technical manufacturing domains [F1].

Future Growth Prospects Aligned with Industry Risks

Luxfer’s forward growth narrative largely hinges on resolving ongoing regulatory reviews alongside judicious capital allocations supporting production capabilities indicated by measured capex commitments [$2–3m range] [N3][N4][S1]. The absence of explicit guidance on market expansion or new contract wins focuses investor attention on outcomes relating to compressed natural gas system safety inquiries which could reshape cost structures or product acceptance.

Environmental indemnity provisions recognized for divested assets coupled with lease guarantor duties remind stakeholders of contingent legacy exposure urging operational caution versus aggressive scaling [S1][S12].

In sum, growth drivers seem tightly bound by risk mitigation priorities rather than broad commercial acceleration currently.

Key Upcoming Milestones and What to Monitor Next

Critical near-term catalysts include:

- Resolution timeline for the NHTSA preliminary evaluation on Type 4 CNG container allegations—the outcome will materially impact warranty reserves or recall expenses recorded [S12].

- Banking facility renewal strategy as existing committed lines totalling $125m expire October 2026—with current modest drawdown levels suggesting room for refinancing but also dependence on credit markets condition [S7].

- Actuarial assumptions review ahead affecting pension expense recognition given sensitivities surrounding discount rates, inflation indices reform trajectory starting circa next decade, and longevity forecasts influencing valuation volatility [S10][S15].

- Any changes or clarifications regarding environmental indemnity commitments related to historical site sales including Madison Illinois closure cost projections capped at ~$1m plus contingencies up to $10m over five years [S1].

Absent explicit financial guidance disclosures—common for companies facing regulatory uncertainty—stakeholders must track filings for updates on these fronts alongside interim quarterly performance releases keyed into cash flow trends versus operating profitability metrics.

This analysis synthesizes public disclosures from Luxfer Holdings PLC’s most recent SEC filings and news releases up through February 25, 2026 without offering investment advice or predictions beyond documented facts and observed industry patterns.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments