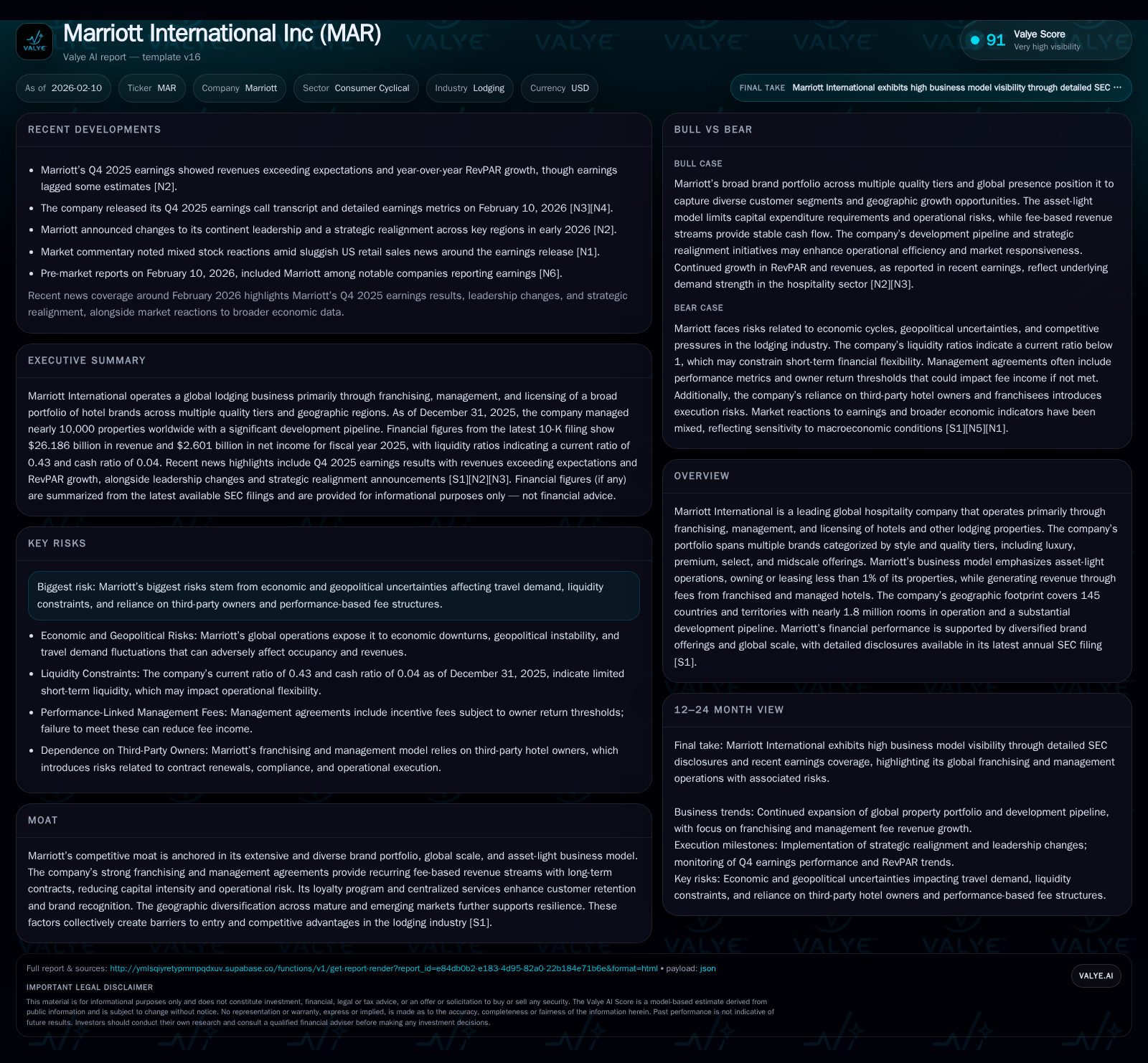

Marriott International's Global Scale and Asset-Light Strategy Amid Q4 Earnings Dynamics

Marriott navigates leadership realignments and macro risks while leveraging its diverse brand portfolio and asset-light model to sustain resilience.

Marriott International continues to assert its dominance in the global lodging industry through an extensive footprint spanning 145 countries and a segmented brand strategy addressing multiple customer tiers. Despite posting stronger-than-expected revenue and RevPAR growth for Q4 2025, earnings fell short of consensus estimates, partly reflecting pressure on margins amid geopolitical and economic headwinds. Recent continental leadership changes signal an intent to sharpen regional strategic execution as the company faces ongoing macroeconomic uncertainties. Marriott’s asset-light business model and loyalty program remain key pillars of competitive advantage, though liquidity metrics warrant continued monitoring given the compressed current ratio.

Global Footprint and Brand Portfolio: Marriott’s Competitive Backbone

Marriott International’s expansive geographic reach is a foundational element of its competitive positioning. Operating in approximately 145 countries and territories with close to 1.8 million rooms under management or franchise contracts, Marriott services a vast array of markets that encompass both mature hubs such as North America and emerging regions including parts of Asia Pacific and Latin America [S1, F1]. This global footprint supports diversified revenue streams that mitigate region-specific economic volatilities.

Integral to this scale is Marriott’s broad brand architecture which strategically segments customers by style preference and price sensitivity. Its league spans luxury (e.g., Ritz-Carlton), premium (Marriott Hotels), select service (Courtyard by Marriott), to midscale offerings tailored to varied traveler demographics [S1]. Such segmentation allows targeted market penetration — serving discerning luxury seekers while capturing volume from business travelers or cost-conscious leisure guests alike. This portfolio breadth also acts as a barrier to entry for competitors unable to replicate such multidimensional coverage.

The scale coupled with brand diversity feeds into what Marriott identifies as its moat: combining global reach with differentiated service tiers enhances brand recognition, customer loyalty, and bargaining power with distributors such as online travel agencies.

The Asset-Light Model in Practice: Strengths and Vulnerabilities

A critical pillar underpinning Marriott’s business model is its heavy reliance on asset-light strategies: owning or leasing less than one percent of hotel properties within its system [S1]. Instead, it focuses predominantly on franchising arrangements where independent hotel owners operate under Marriott brands, paying fees for use of intellectual property and centralized services; alongside management contracts where Marriott runs hotels for owners receiving base fees plus incentive fees tied to operational performance.

This model minimizes capital deployment requirements and enables rapid scaling through third-party development — advantageous in capital-intensive hospitality real estate markets. Fee-based revenue streams derived from franchise fees, base management fees, and performance incentive fees provide relatively stable cash flows insulated from direct operational costs or property depreciation [S1].

However, this structure carries inherent risks that require vigilance. The company acknowledges exposures related to premature terminations of franchise or management contracts due to owner bankruptcy or poor performance—events that could reduce recurring income unexpectedly. Further, dependence on owner financial health means economic downturns causing hotel owner distress can cascade into contractual attrition or delayed developments [S1]. Maintaining strong relationships with owners and ensuring brand standard compliance remain imperative.

Q4 2025 Financial Snapshot: Revenue Upside vs Earnings Lag

Marriott’s Q4 2025 financial results underscore this dynamic tension between topline strength and bottom-line challenges. Revenues topped analyst expectations driven by strong average daily rates (ADR) increases and increased occupancy reflected in rising revenue per available room (RevPAR) year-over-year growth [N1, N3]. These gains confirm continued recovery momentum post-pandemic with sustained demand for both leisure and business travel segments.

Yet despite robust revenue growth culminating in trailing twelve months topping $26 billion (F1), earnings notably lagged consensus forecasts [N4]. The shortfall traces largely to escalating operational expenses exacerbated by inflationary pressures on labor costs, energy prices, and supply chain disruptions impacting service delivery margins globally. Incentive fee revenues also felt strain as variability in hotel owner performance moderated payouts compared with prior quarters [N2].

Such divergence between revenue upside versus margin squeeze reflects industry-wide challenges as lodging companies navigate inflationary environments alongside volatile travel patterns influenced by geopolitical tensions.

Leadership Realignment: Strategic Shifts Across Continents

In early January 2026, Marriott announced significant leadership changes across its continental operations — an acknowledgment of the need to recalibrate management focus amidst evolving market complexities [N12]. These adjustments entail appointing new heads for key regions including EMEA (Europe, Middle East & Africa), Asia Pacific excluding China, Greater China itself, Caribbean & Latin America.

Management cited realignment objectives geared toward sharpening regional agility by empowering local teams better versed in their markets' unique regulatory landscapes, consumer behaviors, and competitive dynamics. This stratagem signals an intention to enhance execution precision particularly in fast-growing emerging regions while defending entrenched positions in mature economies plagued by slower economic expansion or heightened geopolitical friction.

Such recalibration aligns with broader corporate initiatives fostering innovation adoption at regional levels—especially digital transformation efforts supporting reservations platform enhancements tied closely to localized guest preferences.

Loyalty Programs and Digital Channels: Winning Customer Retention Battles

Marriott's Bonvoy loyalty program remains an essential strategic asset driving customer retention amid relentless disruption from alternative lodging options including home-sharing platforms like Airbnb. Boasting tens of millions of members globally, Bonvoy integrates multi-brand rewards accumulation enhancing cross-property visitation incentives—a notable advantage over isolated competitors lacking unified point systems or extensive global presence [S1].

Beyond loyalty points accruals, Marriott has invested heavily in digital infrastructure encompassing mobile apps enabling seamless booking experiences, personalized promotions facilitated by data analytics, co-branded credit card partnerships expanding paid stay financing options—altogether contributing to elevated brand stickiness.[S1]

This digital ecosystem does not merely lock-in frequent travelers but generates valuable behavioral data feeding into dynamic yield management algorithms optimizing pricing strategies relative to market conditions. In an era where convenience increasingly dictates consumer choices, Marriott’s platform sophistication offers sustained differentiation amid intensifying competition.

Risk Factors from Market and Geopolitical Uncertainties

Per SEC disclosures [S1], Marriott explicitly flags myriad external risk vectors that could materially impede its operational stability or financial condition:

- Macroeconomic volatility reducing discretionary travel budgets impacting occupancy rates thus curtailing fee income.

- Geopolitical crises triggering travel bans or advisories diminishing international traveller flows.

- Inflationary cost escalations squeezing operating margins.

- Potential inability or unwillingness of hotel owners to refinance debt affecting hotel system integrity.

- Operational disruption risks including pandemic resurgence or natural disasters affecting property openings or renovations.

- Liquidity stresses arising from tighter credit conditions complicating capital access.

- Cybersecurity threats imperiling reservation systems—a focus area given recent industry trends (not detailed here).

Internally, risk concentrates around maintaining franchisee/owner relationship quality; premature termination clauses introduce unpredictability into revenue streams if poorly managed.

2026 Guidance: Navigating Growth Amid Macro Challenges

Early February guidance release frames a cautiously optimistic outlook balancing aspirational growth paths against existing macroeconomic headwinds [N5]. Management signals intent to push forward on the substantial development pipeline aiming to add rooms chiefly via franchising agreements targeting key growth corridors in Asia Pacific and Latin America while innovating guest experiences digitally.

However, the tone remains measured acknowledging prevailing uncertainties around inflation trajectories, interest rate policies globally influencing travel behaviors broadly. The forecast embraces a scenario expecting sustained modest RevPAR expansions counterweighted by potential incremental expense inflation necessitating tight cost discipline initiatives.

This calibrated guidance attempts transparency towards investors regarding external risks while reinforcing confidence in the robustness of the underlying business model driving long-term value creation potential.

Comparative Lens: Marriott Against Industry Peers

Relative to peers such as Wynn Resorts—which focuses more narrowly on gaming resorts—the scale advantages intrinsic to Marriott's broad portfolio provide differentiation against cyclical shocks impacting discrete lodging segments [N7]. While Wynn may experience sharper volatility tied tightly to leisure gambling tourism concentrations primarily around Las Vegas Macau clusters, Marriott benefits from wide geographic dispersion tempering shocks localized to specific destinations.

Moreover, Marriott’s multi-brand approach uniquely insulates it somewhat; luxury brands can offset premium demand shortfalls via higher-end clientele whereas select/midscale properties capture more resilient segments amid economic softness.

That said industry-wide trends such as rising labor costs, inflationary pressures on energy/utilities inputs are common challenges creating margin compression risks universally requiring operational ingenuity.

Financial Health Check: Liquidity and Balance Sheet Insights

Scrutinizing Marriott's latest SEC filings reveals strengths alongside caution flags on liquidity metrics fundamental for sustaining asset-light strategy execution [F1,S1]. Year-end cash & equivalents stood at approximately $358 million—a modest absolute figure given enterprise scale—aligned with total current assets near $3.58 billion against current liabilities tallying about $8.4 billion yielding a current ratio around 0.43 signaling potential short-term liquidity tightness.

While the asset-light model reduces fixed asset burdens thus lowering capital expenditure requirements compared with traditional ownership-heavy competitors, this liquidity geometry implies reliance on revolving credit lines or short-term borrowing instruments might be necessary for working capital needs especially during periods of unexpected cash flow stress or cyclical downturns.[S1]

Debt maturity ladders were not explicitly disclosed here but past debt restructuring efforts have balanced manageable interest expense profiles facilitating free cash flow generation capacity supporting dividend returns while maintaining investment-grade ratings according to prior company disclosures.

Ensuring ongoing covenant compliance amid volatile demand cycles remains pivotal so close monitoring will be prudent going forward.

This analysis synthesizes publicly available information including SEC filings dated February 10th, 2026 ([S1]), recent news articles detailing earning releases ([N1], [N3], [N4]), leadership updates ([N12]), 2026 guidance ([N5]), peer comparisons ([N7]), along with company facts datasets ([F1]). It aims at providing a comprehensive view of Marriott International's strategic posture without rendering investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments