MasterBrand Inc Approaches Critical Merger Milestone with American Woodmark

Q1 2026 results highlight operational pressures and strategic moves as MasterBrand advances toward merger completion.

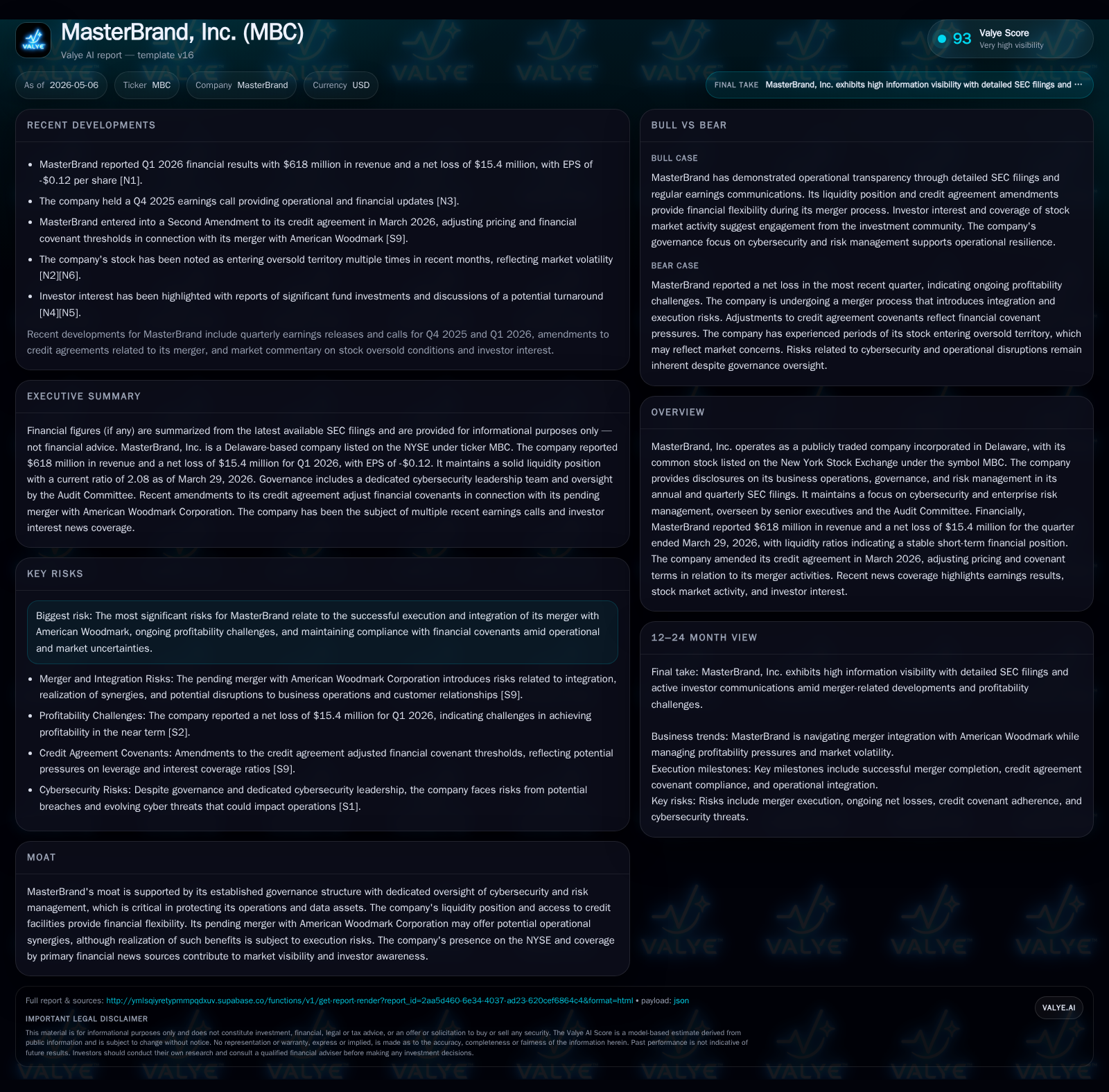

MasterBrand’s latest quarterly report reveals $618 million in revenue alongside a net loss of $15.4 million, reflecting ongoing operational challenges. The company has amended its credit agreement to accommodate merger-related financial covenants with American Woodmark, underscoring the strategic priority of closing this deal in Q2 2026. MasterBrand’s core cabinetry business remains reliant on residential construction trends and supply chain stability, while the anticipated merger promises scale efficiencies and enhanced market reach. Execution risks persist around integration, regulatory approval, and profitability restoration.

Q1 2026 Operating Update and Strategic Implications

MasterBrand reported first quarter 2026 revenue of $618 million accompanied by a net loss of $15.4 million, marking continuing operational challenges amid a stable top line [S2][S3]. This loss underscores the cost pressures and integration investments ahead of the expected merger with American Woodmark Corporation slated for completion in Q2 2026. Notably, in March 2026, the company amended its credit agreement to modify pricing terms and adjust net leverage and interest coverage covenants through January 2027 or until the merger closes—whichever occurs first—demonstrating proactive financial management aligned with the transaction timeline [S2][S12].

While liquidity remains sound with a current ratio near 2.08 supported by $138.4 million in cash equivalents as of March 29, 2026, total debt remains elevated at approximately $1 billion gross, implying a levered balance sheet that will require disciplined integration execution to enhance free cash flow and deleverage post-merger [F1]. Operationally, management has emphasized maintaining steady customer engagement and supplier continuity during this transitional period to mitigate disruption risks frequently associated with large-scale mergers [N1].

MasterBrand’s Business Model and Product Offering: Foundation for Growth

MasterBrand operates primarily as a manufacturer and distributor of cabinetry products serving residential housing markets across the United States [S1]. Revenue generation stems from direct sale of cabinetry solutions—spanning kitchen, bath, and specialized storage units—to new home builders as well as remodelers. Customers predominantly comprise retail chains and specialty distributors who drive downstream sales to contractors and homeowners.

The company’s value proposition hinges on brand reliability, design innovation, customization options, and broad product assortments targeting both value-conscious and premium segments. Switching costs are moderately entrenched given project timelines and supplier relationships; however, competitive pressures necessitate continual investment in manufacturing efficiency and product quality enhancements.

Revenue dynamics are influenced by housing market cycles—new construction starts fuel volume growth whereas renovation demand adds structural resilience across slower economic periods. Pricing power is tempered by commodity price volatility (notably lumber and hardware components), necessitating careful cost pass-through mechanisms combined with procurement savvy to sustain margins.

Industry Structure and Competitor Positioning in Home Cabinetry

MasterBrand competes within a moderately concentrated U.S. cabinetry industry characterized by several key players including American Woodmark—the future merger partner—and other regional manufacturers. The sector faces margin pressure due to escalating raw material costs exacerbated by global supply chain disruptions impacting delivery lead times and input pricing [S1][S16].

While scale confers advantages in negotiating better procurement contracts and accessing broader distribution networks, competition remains vigorous on price points and service levels. Regulatory compliance—covering workplace safety standards in manufacturing plants plus product safety certifications—adds fixed overhead burdens.

Furthermore, channel shifts towards big-box retailers versus specialty outlets require nimble marketing strategies to maintain market share. MasterBrand’s established footprint affords relative resilience; yet efficiency gains post-merger are critical as smaller competitors may aggressively price amidst margin compression.

Growth Drivers: Merger Synergies and Market Opportunities

The pending acquisition of American Woodmark represents a pivotal growth driver expected to unleash significant synergies. Management projects enhanced purchasing power through combined procurement volumes enabling reduced input costs across shared suppliers [S3][S13]. Additionally, rationalization of overlapping manufacturing footprints aims at trimming overhead expenses while preserving capacity flexibility.

On revenue enhancement fronts, the merged entity anticipates expanded geographical penetration leveraging complementary distribution channels—American Woodmark's presence notably strengthens access into select regional markets absent or underrepresented in MasterBrand’s current network.

Macroeconomic tailwinds remain supportive as U.S. housing market fundamentals exhibit stability driven by demographic trends favoring sustained remodeling activity even amidst new build fluctuations [N1]. The cabinetry category benefits from these housing drivers alongside evolving consumer preferences favoring modern designs that necessitate innovative product lines—a strategic focus area for combined R&D teams.

Risks and Watchpoints: Integration, Profitability, and Regulatory Hurdles

Despite optimism around merger benefits, substantial risks cloud near-term prospects. Integration uncertainties include executing operational consolidations smoothly without disrupting longstanding supplier or customer relationships critical for order book stability [S2][S16]. Delays or failures in synergy realization could exacerbate recent profitability challenges.

Regulatory clearance remains a watchpoint as the companies continue cooperation with the U.S. Federal Trade Commission to secure antitrust approval; any postponements could push back expected closure timelines beyond Q2 2026 targets [S13].

These events will collectively shape whether anticipated scale economies begin materializing within planned windows or if additional managerial interventions become necessary.

Financial Snapshot: Current Liquidity, Leverage, and Profitability

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $138mm | |

| 2026-03-29 | ||

| Current assets | $735mm | |

| 2026-03-29 | ||

| Current liabilities | $354mm | |

| 2026-03-29 | ||

| Current ratio | 2.08x | |

| 2026-03-29 |

Source: SEC companyfacts cache [F1].

Note: Approximate net debt calculated from latest available metrics combining total debt less cash balances.

This financial profile reflects sufficient short-term liquidity balanced against significant gross leverage indicative of capital-intensive operations plus expansion via acquisition strategy.

This analysis integrates MasterBrand’s latest quarterly disclosures as well as recent strategic announcements outlining merger progress. While the company benefits from operational scale advantages underpinning cabinet manufacturing leadership in North America, immediate profit recovery hinges on disciplined synergy execution amid regulatory scrutiny. Investors should watch carefully how integration initiatives unfold against evolving economic conditions influencing residential construction demand.

Disclaimer: This report is for informational purposes only; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments