Mondelez International Maneuvers Cocoa Cost Pressures to Sustain Snack Market Leadership in 2025

Despite elevated commodity costs and supply chain challenges, Mondelez posted robust Q4 earnings underscoring its resilient brand and operational scale.

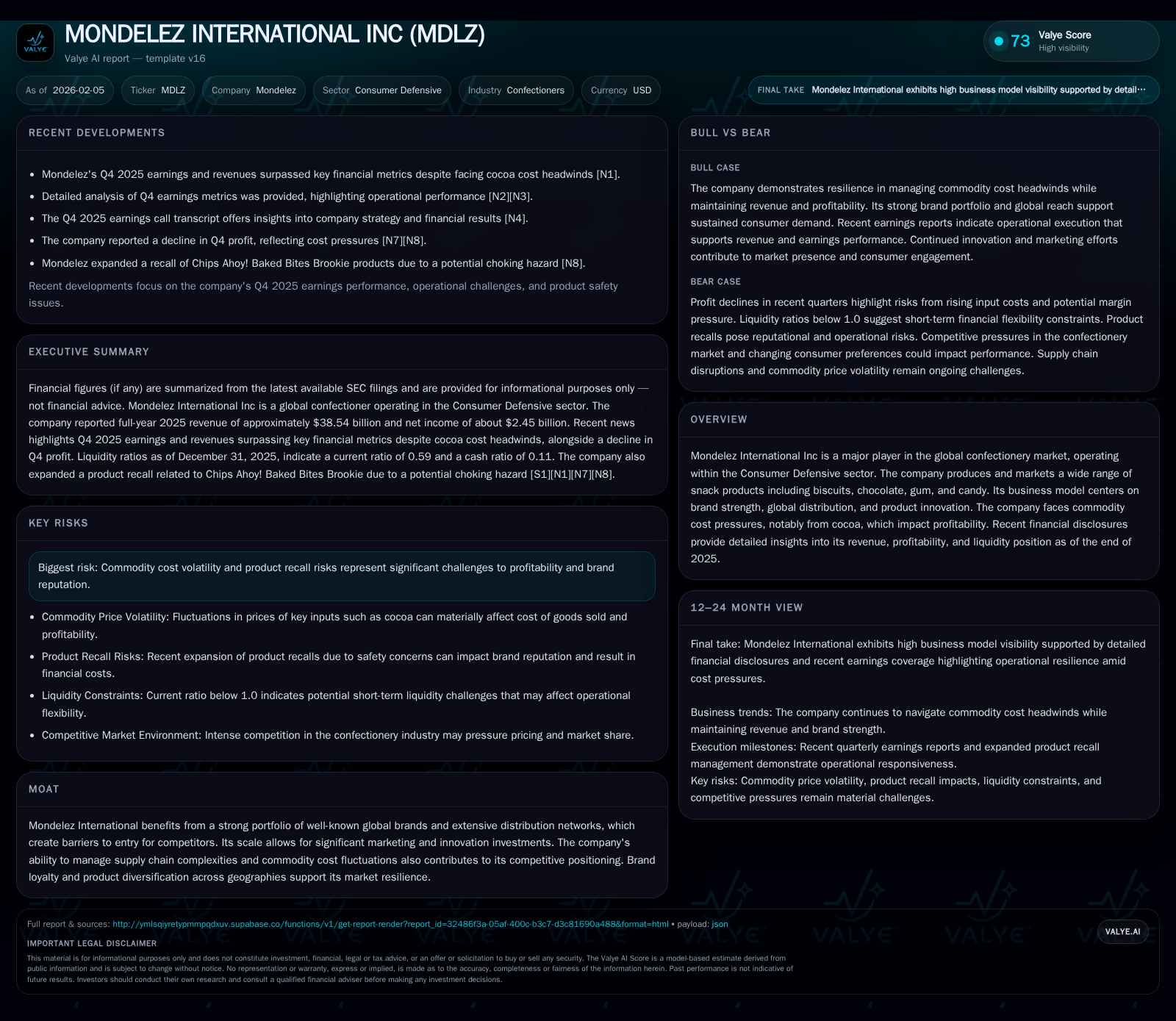

Mondelez International demonstrated financial resilience in Q4 2025 by beating earnings expectations amidst significant cocoa price inflation. Its entrenched portfolio of global snack brands, supported by extensive distribution and continuous innovation, underpins a durable competitive moat. Nevertheless, persistent commodity volatility, supply chain complexities, and recent product recalls present ongoing risks to profitability and reputation. The company’s liquidity position reveals operational tightness but manageable balance sheet strength as it navigates these headwinds.

Earnings Triumph Amid Cocoa Cost Challenges

The closing quarter of 2025 reinforced Mondelez International’s capacity to navigate turbulent commodity markets while delivering financial results that outpaced analyst expectations. The company recorded annual revenues exceeding $38 billion, with net income near $2.45 billion—markers of its considerable scale within the consumer defensive space focused on confectionery products [F1]. This performance stood out notably against the backdrop of escalating raw material prices, most significantly cocoa. Industry reports highlighted cocoa cost increases as substantial headwinds threatening margin contraction across confectioners in late 2025 [N1]. Yet, Mondelez’s Q4 earnings beat was bolstered by effective pricing strategies and robust demand for core brands, alongside measurable operational efficiencies detailed in their earnings call transcript [N4][N5][N6]. This outcome underscores a resilience shaped by decades of brand establishment paired with nimble cost management.

Unpacking Mondelez’s Moat: Brands, Scale, and Innovation

At the crux of Mondelez’s market defense lies a fortified moat constructed around an internationally recognizable brand portfolio. The company commands dominant positions in biscuits (e.g., Oreo), chocolate, gum, and candy categories that benefit from entrenched consumer loyalty worldwide. This brand strength is coupled with an expansive geographic footprint reaching diverse markets—allowing the firm to leverage scale not only for production but also for marketing and distribution efficiencies [valye_report_excerpt][S1]. Such breadth enables Mondelez to maintain pricing power despite inflationary pressures. Furthermore, continuous product innovation pipelines introduce refreshed offerings that address evolving consumer tastes and allow premiumization opportunities. These strategic pillars provide buffers against aggressive competition and shifting demand patterns. Their interplay reinforces competitive advantages that few peers match in scope or depth.

Supply Chain Complexities Across Global Markets

Managing an extensive supply chain sprawling multiple continents introduces intricate operational challenges for Mondelez. Raw material sourcing volatility—accentuated particularly in agricultural commodities like cocoa—intersects with logistical constraints such as port congestion and fluctuating transportation costs [valye_report_excerpt][S1]. These factors collectively heighten risk exposure across Mondelez's manufacturing and delivery processes. Sophisticated risk management capabilities therefore become essential both in planning procurement cycles and responding dynamically to disruptions. An emphasis on supplier diversification and inventory management measures helps moderate these vulnerabilities while protecting product availability in regional markets. Nonetheless, tightness in any link of this chain can cascade into margin erosion or revenue loss if not carefully controlled.

Commodity Pressures: Cocoa and Beyond

Cocoa remains one of the most critical input cost factors for Mondelez given its prominence in chocolate-based offerings. Late-2025 saw pronounced cocoa price surges stemming from geopolitical tensions affecting West African supply zones coupled with weather-related crop uncertainties [N1][S1][valye_report_excerpt]. While the company employs hedging mechanisms that provide partial insulation against short-term price shocks, the inherent volatility significantly pressures cost structures overall. Additionally, other commodity inputs such as sugar and certain packaging materials have exhibited inflationary trends contributing further to cost headwinds. Thus, despite careful procurement strategies and efficiency drives, margin compression risks persist—a reality Mondelez must continuously monitor against evolving market conditions.

Risk Factors Impacting Profitability and Reputation

Beyond commodity cost fluctuations lie additional risks impacting Mondelez’s profitability trajectory. Notably, product safety incidents represent salient threats; an expanded recall announced at the end of 2025 involving Chips Ahoy! Baked Bites over choking hazard concerns highlights sensitivity regarding quality control lapses [N13][S2]. Such events risk damaging brand reputation with downstream effects on sales momentum if consumers lose confidence. Moreover, broader reputational risks intertwine with regulatory scrutiny following recalls or supply chain controversies—demanding rigorous compliance frameworks embedded within operational norms [S1]. The company’s disclosures emphasize these risk dimensions explicitly rather than as generic statements; this recognition suggests active management attention directed at mitigating event recurrence while safeguarding long-term brand equity.

Liquidity and Balance Sheet Resilience in 2025

Examining liquidity status as of December 31, 2025 surfaces some tension between current assets ($12.95 billion) and liabilities ($21.86 billion), rendering a notably low current ratio around 0.59 [F1]. This gap signals potential challenges in covering short-term obligations solely through readily available assets without additional financing measures. However, the balance sheet is cushioned by steady net income levels approximating $2.45 billion annually which improve internal cash generation capabilities for working capital support [F1][S1]. Additionally, presence of long-term financing instruments likely aids flexibility beyond strict current asset coverage metrics. While this degree of liquidity tightness warrants attention for operational preparedness—especially amidst macro uncertainty—it does not currently indicate severe distress given Mondelez’s standing credit profile and cash flow sufficiency.

Strategic Outlook: Leveraging Strength in a Competitive Landscape

Looking ahead into 2026 and beyond necessitates viewing Mondelez through the prism of adaptability grounded in entrenched strengths. Market commentary preceding the Q4 release noted investor focus on sustained growth potential tied to resilient demand for staple snacks during uncertain economic environments [N9][N10]. The company’s commitment to innovation coupled with geographic diversification provides avenues to offset region-specific shocks or ingredient cost escalations while capturing incremental market share where competitors falter. Continued investment into supply chain robustness could further moderate risk exposure inherent in ingredient sourcing complexity. Ultimately, Mondelez’s enterprise value proposition rests on combining heritage brand prestige with execution discipline amid evolving consumer preferences and external pressures.

Disclaimer: This analysis is based solely on publicly available information up to early February 2026 with no predictive assertions or investment recommendations implied.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments