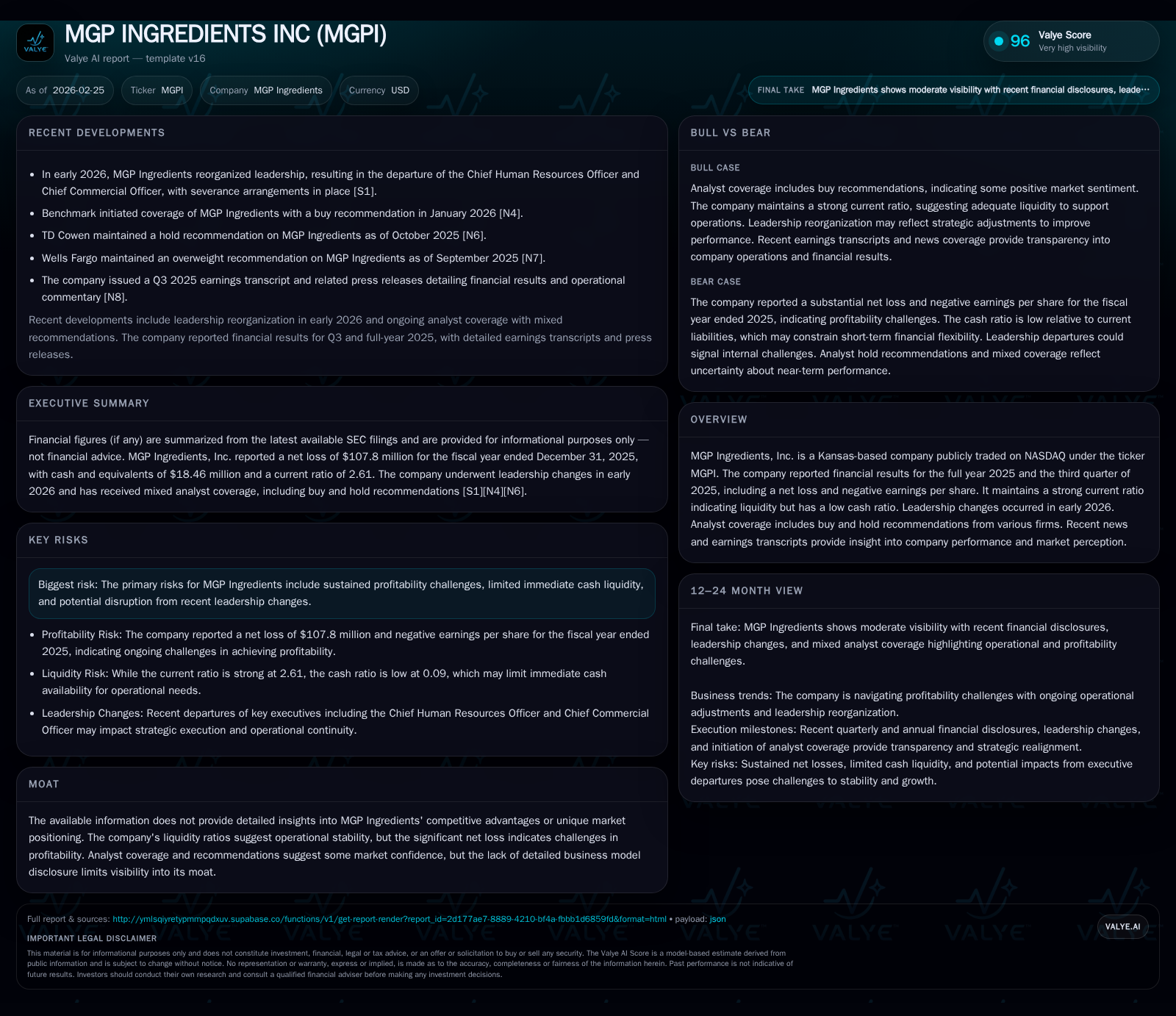

MGP Ingredients Faces Profitability Decline Despite Strong Liquidity

Despite a sharp net loss in 2025, MGP Ingredients demonstrates robust operating cash flow and liquidity, highlighting strategic challenges amid leadership changes.

MGP Ingredients’ fiscal year 2025 was marked by a pronounced reversal from profitability to significant losses, with net income plunging over 400% year-over-year. This steep decline contrasts sharply with its solid operating cash flows and a strong current ratio of 2.61, signaling underlying financial resilience despite earnings pressures. Recent leadership turnover and cautious capital deployment signal a company in transition, balancing operational challenges with liquidity stability. Analysts remain cautiously optimistic, citing the company’s cash generation capacity as a buffer while closely monitoring cost control and strategic execution.

Financial Performance Trajectory: From Operational Gains to Steep Losses

Fiscal year 2025 marked an inflection point for MGP Ingredients (MGPI), with the company recording its first significant operating loss in recent history. Previously, MGPI exhibited strong operational performance—operating income rose sharply from approximately $29.7 million in FY2022 to $148.6 million in FY2023 before tapering to $74.4 million in FY2024. Correspondingly, net income remained positive and robust through 2024, peaking at about $109 million in FY2022 and maintaining healthy levels through FY2023 ($107 million) before declining to $34.7 million in FY2024.

However, FY2025 reversed this trend dramatically: operating income plunged to a negative $(94.6) million—a year-on-year decrease exceeding 227%. Net income followed suit with a staggering loss of $(107.8) million representing a decline of over 410% compared to the prior year [F1]. This deterioration occurred alongside an approximate 13.5% contraction in revenue when considering comparable periods within recent years' data streams.

The deterioration signals material operational strain that eclipsed prior profitable runs and marks MGPI’s sharpest financial setback over this multi-year horizon.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -108 | 122 | -95 | 45 | -411.0% |

| 2024 | 35 | 102 | 74 | 71 | -67.7% |

| 2023 | 107 | 84 | 149 | 55 | -1.8% |

| 2022 | 109 | 89 | 30 | 45 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 10 | 1 | 76 |

| 2024 | 11 | 49 | 31 |

| 2023 | 11 | 1 | 29 |

| 2022 | 11 | 1 | 44 |

Source: SEC companyfacts cache [F1].

Note: Revenue figures for recent years are limited due to inconsistent yield streams; operating income and net income illustrate profitability swings.

Unpacking the FY2025 Decline: Key Drivers Behind MGPI’s Negative Earnings

The precipitous drop into negative territory for earnings stems from a confluence of factors disclosed within regulatory filings and news updates [S1], [S3], [S4], complemented by observed market conditions reported contemporaneously.

Risk factor disclosures highlight heightened commodity input costs disrupting ingredient supply chain economics coupled with inefficiencies from production throughput variability amid challenging end-market demand patterns [S4],[S5],[S6],[S7]. Litigation matters appear contained without direct immediate financial impact but add governance complexity that can divert management focus.

Leadership turbulence coincides chronologically with the performance downturn: key executives including the Chief Human Resources Officer and Chief Commercial Officer exited early February 2026 after severance arrangements were executed [N4], [S18]. These changes emphasize potential strategic realignments aiming to address operational deficiencies.

The erosion is partly attributed to contraction across higher-margin private label contracts juxtaposed against increased fixed overhead absorption costs—a dynamic not uncommon in ingredient manufacturing where scale utilization critically impacts margin profiles (analysis).

Liquidity Health and Balance Sheet Overview: Stability Amid Turbulence

Despite profitability headwinds, MGPI maintains substantial liquidity buffers anchored by current assets exceeding current liabilities by over $322 million culminates into a healthy current ratio of approximately 2.61 as of December 31, 2025 [F1], [S10], signifying readily available short-term asset coverage against obligations.

Cash and equivalents stood at roughly $18.5 million—relatively modest compared to total current assets—resulting in a low cash ratio reflective of working capital deployed within inventory and receivables typical for ingredient suppliers engaged in volume-based contract fulfillment cycles (analysis).

Such liquidity positioning affords MGPI operational flexibility under strained earnings conditions, allowing continuation of supply chain commitments while retooling cost/fixed expense structures.

Capital Deployment Review: Dividends, Buybacks, and Investment Patterns

Capital allocation choices align conservatively given earnings pressure yet reflect management’s intent to maintain shareholder returns where feasible.[S11],[S18],[S19] Dividend payments persisted near $10 million annually through FY2025 representing consistency relative to prior years despite lower profits [F1].

Conversely, share repurchase activity contracted significantly—from roughly $48 million deployed in buybacks during FY2024 down to approximately $1 million in FY2025—likely driven by cautious capital preservation amid uncertain profitability trends.

Capital expenditure outlays declined by over one-third year-over-year to approximately $45 million after peaking above $71 million the previous year signaling either deferred growth investments or recalibrated spending aligned with operational restructuring efforts or broader macroeconomic uncertainties impacting ingredient sector growth prospects.

Leadership Shifts and Market Positioning: Implications for Future Growth

The executive reshuffling noted at the outset of calendar year 2026 marks potentially pivotal inflection points for MGPI’s strategy implementation.[N4],[S11] The departure of senior commercial and human resources officers suggests renewed focus on optimizing organizational execution amid emerging challenges.

Analyst scrutiny through Benchmark’s coverage initiation—with an accompanying Buy rating—provides external validation anchored chiefly on MGPI’s resilient operating cash flows rather than detailed moats or differentiated technology/IP positions.[N4]

Absent explicit moat disclosures constrains confidence related to sustainable competitive advantages; ingredient supply chains entail substantial customer concentration risk and margin cyclicality making leadership execution critical (analysis).

Forecast Signals and What to Monitor: Analyst Insights and Company Expectations

While explicit forward guidance remains undisclosed as per filings,[N4],[S3] market observers should track forthcoming quarterly earnings releases focusing on:

- Efficacy of cost containment measures,

- Resumption or stabilization of gross margin trajectories,

- Cash flow consistency supporting operations without incremental leverage,

- Progression under new leadership frameworks,

- Contract wins or retention signaling revenue baseline recovery. Benchmark’s buy recommendation foregrounds these metrics as principal signals supporting valuation normalization assumptions pending operational turnaround confirmation.

Risks Influencing Path Forward: Profitability Challenges and Governance Changes

Risk exposures remain elevated reflecting both financial performance volatility and governance dynamics documented across multiple SEC filings.[S4],[S5],[S6],[S7] Key risk vectors include:

- Continued negative earnings momentum threatening equity returns (FY25 ROE approximates negative 15%, computed as net loss relative to shareholder equity)[F1],

- Liquidity stress scenarios compounded by low immediate cash reserves,

- Legal/regulatory complexities increasing compliance overhead,

- Potential disruption from leadership churn impeding swift decision-making,

- Market-driven ingredient pricing variability amplifying margin pressures (sector analysis). Investor confidence hinges on demonstrated stabilization trajectories and effective capital stewardship under evolving corporate governance structures implemented via recently amended bylaws.[S19]

Disclaimer: This analysis is provided solely for informational purposes based on public filings and reported data; it does not constitute investment advice or solicitation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments