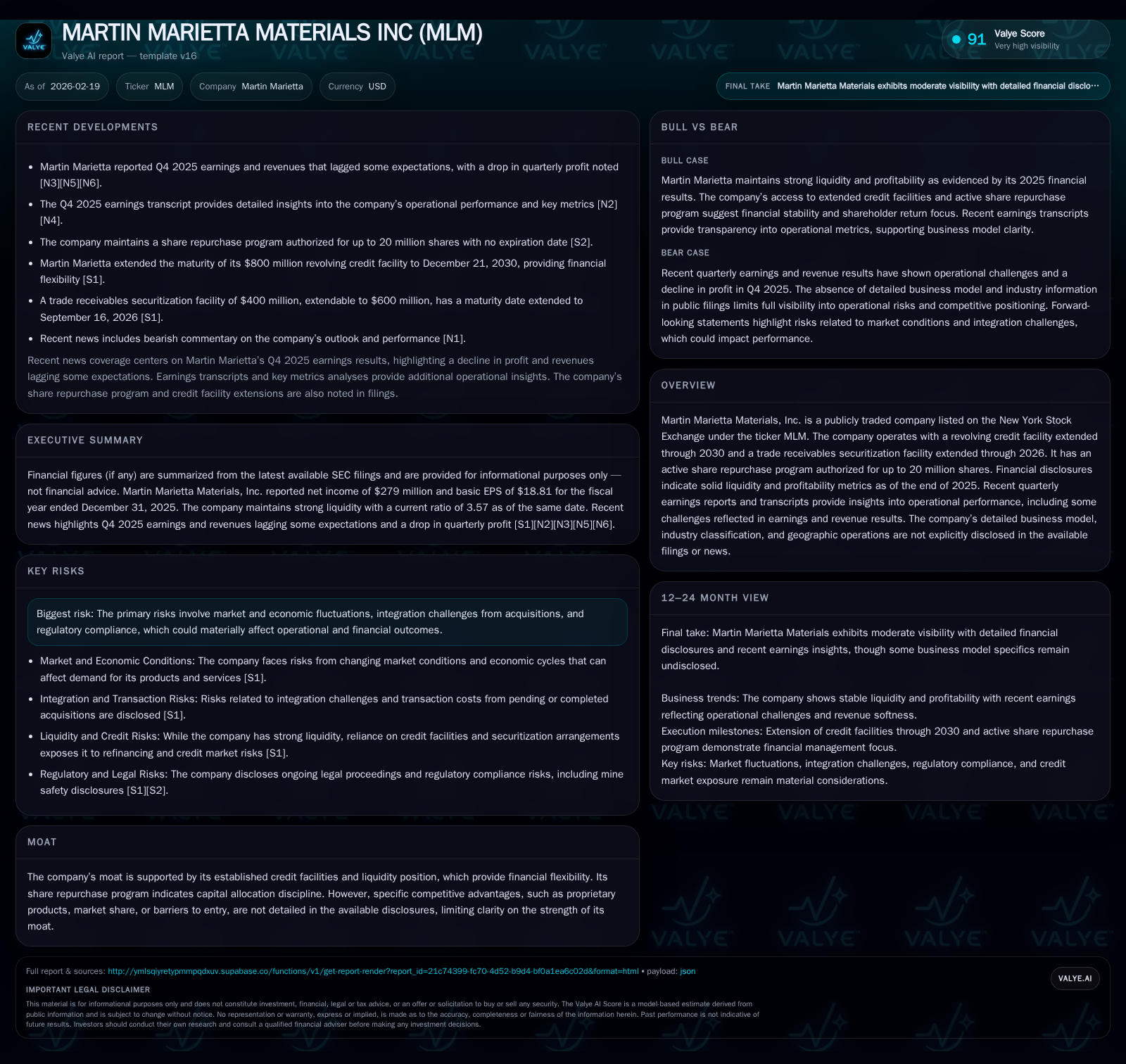

Martin Marietta Materials Confronts Earnings Contraction Post-2024 Surge

After a strong 2024, Martin Marietta faced a sharp decline in earnings in 2025 despite robust operating cash flows, exposing operational and market pressures.

Martin Marietta Materials experienced a dramatic reversal in profitability during 2025, with operating income falling nearly 47% and net income plunging 86% year-over-year following a surge in the prior year. This decoupling from operational cash flow— which grew over 22%—highlights notable earnings pressure amid sustained liquidity and capital allocation discipline, including $450 million in share repurchases and steady dividend growth. Regulatory hurdles, especially mine safety compliance at the Kokomo Quarry, contributed to operational constraints. The extended revolving credit facility and trade receivables securitization underpin liquidity resilience as demand softness tempers near-term growth prospects.

From Momentum to Margin Pressure: MLM’s Recent Earnings Overview

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($bn) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 279 | 1785 | 1.4 | 807 | -86.0% |

| 2024 | 1995 | 1459 | 2.7 | 855 | +70.7% |

| 2023 | 1169 | 1528 | 1.6 | 650 | +34.9% |

| 2022 | 867 | 991 | 1.2 | 482 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 197 | 450 | 978 |

| 2024 | 189 | 450 | 604 |

| 2023 | 174 | 150 | 878 |

| 2022 | 159 | 150 | 509 |

Source: SEC companyfacts cache [F1].

Martin Marietta Materials entered 2025 with considerable momentum following years of steady growth and expanding profitability. However, the fourth quarter of 2025 unveiled stark declines that disrupted this trajectory. Operating income shrank to $1.44 billion for the full year—nearly half its FY2024 peak of $2.71 billion—representing a steep -46.9% year-over-year drop [F1]. Even more dramatically, net income fell from $1.995 billion in 2024 to just $279 million, an -86% collapse signaling acute margin erosion or extraordinary expenses [F1][N1][N12]. Contrasting this earnings contraction was an upsurge in operating cash flow to $1.785 billion (+22.3% YoY), highlighting that while earnings suffered under cost and operational pressures, core cash-generating activities remained resilient and liquid [F1].

This disconnect between accounting profits and cash generation frames the core narrative for Martin Marietta’s recent performance: operational setbacks alongside prudent financial management.

Decoding Historical Growth and What Slowed Momentum in 2025

The company’s four-year performance arc underscores its prior ascent. From FY2022 to FY2024, operating income climbed consistently—from $1.21 billion (FY2022) to $2.71 billion (FY2024)—driven by favorable infrastructure spending environments and pricing power typical for aggregate producers enjoying tight supply-demand balances [F1]. Net income followed suit, rising steadily each year before tumbling sharply in FY2025.

Capex expanded materially across these years, peaking at $855 million in FY2024 before modestly retreating to $807 million in FY2025 as the company dialed back investments slightly amid uncertain demand [F1]. The steep earnings drop despite only mild capex adjustment suggests influences beyond capital intensity—such as cost inflation, pricing pressures, or regulatory compliance—that pressured margins.

Filings hint at operational disruptions including increased safety compliance costs particularly linked to mine incidents which likely contributed materially to margin compression [S3][S4][S11]. The materials sector’s exposure to cyclical infrastructure demand also contextualizes recent softness as federal spending tempos may have moderated after stimulus peaks [N13][N8].

Liquidity Resilience Through Revolving Credit and Securitization Facilities

Financial flexibility remains a notable strength for Martin Marietta despite the profit decline. Key is its extended revolving credit facility with JPMorgan Chase Bank amended to maturity December 2030 [S10], providing a long-dated committed borrowing base of up to $800 million. Additionally, a trade receivables securitization program backed by assets originated by the company was recently extended through 2026 at a base size of $400 million—expandable up to $600 million subject to conditions—and priced off adjusted SOFR +0.70% [S9][S12].

These facilities afford practical liquidity tools critical for working capital management amid uneven revenues or investment timing shifts typical within heavy materials businesses carrying significant inventory and receivable balances.

Capital Allocation Discipline: Share Repurchases and Dividend Strategies

Martin Marietta’s capital return strategy reveals consistent shareholder priority even amidst earnings weakness. Annual share repurchase authorizations have been stable at up to 20 million shares with ongoing execution leading to annual outlays pegged at approximately $450 million in both FY2024 and FY2025 [F1][S8][S17][S18]. Dividend payments also rose steadily from $159 million to nearly $197 million over the same span.

However, the resulting return on equity (ROE) has softened considerably—to an estimated 2.8% for FY2025 (calculated from net income over shareholders’ equity)—reflecting how diminished profits are now spread over an expanded equity base/$10 billion as of end-2025 [F1]. This ROE level may signal revaluation risks or necessitate strategic recalibration if sustained.

Operational Constraints: Regulatory Challenges and Segment Dynamics

A notable event impacting operations was issuance of a Section 107(a) order by MSHA at the Kokomo Quarry following unsafe working condition observations during elevated platform construction [S3][S27][N10]. Although no injuries occurred and remediation was swift enough that the order has been terminated, such regulatory actions impose direct compliance costs—including possible fines or enhanced monitoring—and indirect effects like production downtime or project delays.

Within heavy building materials extraction, such mine safety infractions carry outsized risk for EBITDA given material quarry downtime or workforce distractions; thus this incident likely contributed tangibly to margin pressures observed in late-2025 results.

Forward-Looking Indicators: What the Latest Earnings Signal for MLM

Absent explicit forward guidance from management transcripts or filings for post-2025 quarters [N1][N2], industry analyst commentary highlights ongoing cyclical sensitivity linked primarily to U.S public infrastructure spending trends [N6][N7][N8][N13]. While federal investments remain supportive overall, quarter-to-quarter variations could continue pressuring top-line results alongside raw material input cost volatility.

Market observers focus on near-term volume softness coupled with expected stabilization later if macroeconomic conditions improve. This sets medium-term expectations around how effectively Martin Marietta can control costs while navigating regulatory compliance impacts.

Financial Engines Underpinning Free Cash Flow Amid Operating Income Decline

Martin Marietta’s ability to deliver rising operating cash flows (+22%) despite shrinking reported operating income is noteworthy from a financial efficiency standpoint [F1]. Reduced capex spending (-5.6%) helped lift free cash flow close to $978 million for FY2025 (operating cash flow minus capex), underscoring operational cash resilience even amid earnings headwinds.

Such figures suggest ongoing internal controls over working capital plus disciplined investment timing have prevented liquidity stress—an important consideration when assessing capital structure sustainability alongside active buybacks/dividends.

Mine Safety and Compliance Weigh on Operational Stability

Beyond the Kokomo Quarry episode itself lies a broader regulatory environment increasingly focused on safety risk mitigation for aggregate producers [S11][S27]. MSHA enforcement continues tightening standards with pattern-of-violation scrutiny capable of triggering shutdown orders or fines potentially impairing operational cadence substantially.

These factors inject elevated vigilance costs into Martin Marietta’s mining segments while necessitating capital outlays for equipment upgrades or enhanced training—not typically visible line items but essential expenditures for uninterrupted output.

What to Monitor Next: Debt Maturity, Buyback Execution, and Market Demand

Looking ahead, several factors warrant close observation:

- The revolving credit facility extension through December 2030 provides mid-term borrowing certainty; any adjustments or refinancing terms could impact cost of debt profiles [S9][S10][S12].

- Execution pace of authorized share repurchases remains critical; tracking actual volumes bought versus authorization expansions offers insight into capital return posture [S17][S18].

- Infrastructure funding patterns driven by public policy shifts influence aggregate demand at regional levels; careful monitoring remains essential given cyclicality evidenced historically [N14][N13].

- Updates on regulatory incidents including potential recurrence or expansion beyond Kokomo could recalibrate compliance cost assumptions dramatically.

Taken together, these represent actionable data points for analysts evaluating MLM’s balance between tactical liquidity management and strategic growth amid evolving market headwinds.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments