MOBIX LABS Drives Demand Growth in Defense Components While Battling Listing Risks

The company’s latest quarter underscores rising defense sector demand amid ongoing financial and Nasdaq compliance pressures.

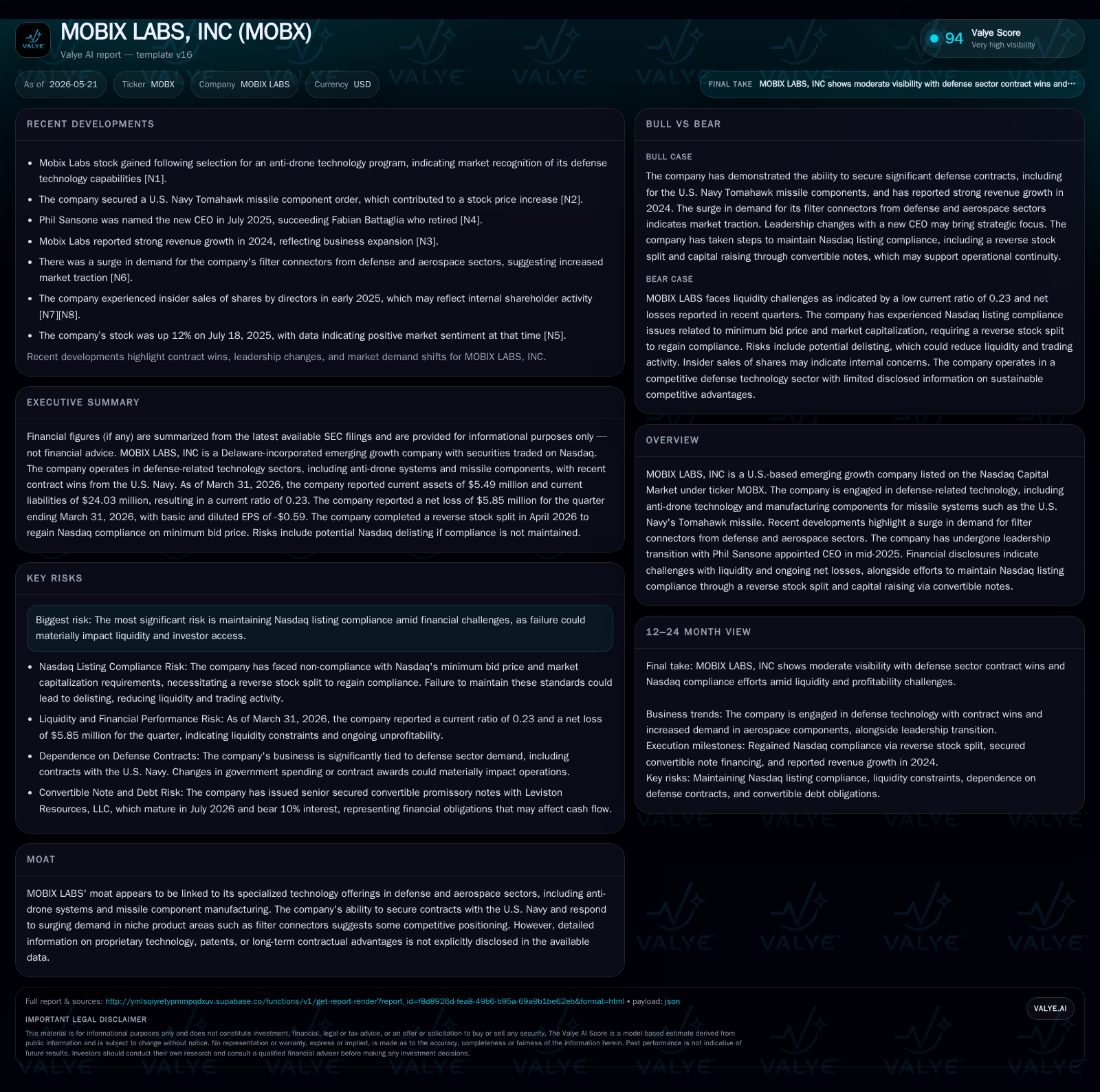

MOBIX LABS’ newest quarterly filing reveals increased orders for specialized defense components, notably filter connectors linked to missile and aerospace systems, supporting near-term growth prospects. However, the company continues to struggle with low liquidity, a weak current ratio of 0.23, and persistent net losses, reflecting ongoing financial stress. Regulatory pressures intensified following a reverse stock split meant to maintain Nasdaq listing compliance, but risks of delisting remain if minimum bid price thresholds are not sustained. Leadership changes and an amended convertible note provide some stability, yet capital management remains critical as MOBIX attempts to convert defense demand momentum into durable operational scale.

Latest Operational Developments: Quarterly Filing Highlights

MOBIX LABS’ latest 10-Q filed May 20, 2026 [S2], supplemented by an 8-K on May 19 [S3], provides crucial updates on the company’s financing and compliance status pivotal to understanding its current operating trajectory. Notably, the company amended its senior secured convertible promissory note with Leviston Resources to increase principal from $3 million to $4 million in March. Shortly thereafter, in mid-May, all $4 million was satisfied through conversion into shares of Class A Common Stock, extinguishing this obligation [S3]. This maneuver injects flexibility in capital structure but highlights reliance on equity dilution.

Simultaneously, MOBIX executed a one-for-ten reverse stock split effective April 6, 2026 which brought its common stock above Nasdaq’s minimum bid price threshold by April 21 [S2][S6]. This step resolved immediate delisting threats due to prior prolonged noncompliance with the $1 minimum bid rule. Despite this short-term regulatory relief, the filing cautions that any future breach will trigger immediate delisting risks without grace periods owing to reverse split rules under Nasdaq policy [S2].

Operationally, the filings underscore a pickup in demand for filter connectors—a high-precision component integral to missile system functionality—and other aerospace-defense product lines tying into U.S. Navy programs like the Tomahawk missile system. These developments suggest incremental order gains that may improve top-line traction amid historically negative net income trends.

Company Business Model and Core Product Portfolio

MOBIX LABS operates predominantly within niche U.S. defense supply chains focused on advanced anti-drone technologies alongside manufacturing highly specialized components—such as filter connectors—for missile systems including the Tomahawk missile deployed by the Navy [S1]. The business model relies on winning government contracts which require adherence to stringent performance, reliability, and regulatory standards that create technical entry barriers.

Revenue generation stems primarily from sales of these precision-engineered electronic components used in high-stakes military applications where failure is unacceptable. Contracts tend to be multi-year with fixed or negotiated pricing reflective of defense budget cycles. Customers likely consist mainly of prime contractors or direct government agencies in aerospace-defense verticals—entities emphasizing reliability certifications and supply continuity.

Product differentiation is rooted in technological quality and durability under extreme environmental conditions; such characteristics underpin some level of switching cost since alternative suppliers must meet exacting military standards. However, the firm’s proprietary technology moat is not explicitly clarified beyond contract exclusivity and specialized engineering capabilities.

Industry Context and Competitive Positioning

Within the broader U.S. defense industrial base ecosystem, MOBIX sits as a specialized supplier addressing specific demand pockets tied closely to evolving military technology trends such as counter-drone capabilities and missile system modernization [S1]. The segment exhibits significant regulatory oversight including export controls (ITAR), procurement protocols (DFARS), and cybersecurity mandates impacting supplier qualifications.

Competition is substantial given many legacy manufacturers operate established government relationships with entrenched scale advantages. Pricing power tends to be constrained by contractual negotiations typical in government procurement—while quality thresholds serve as a gating factor limiting new entrants. Customer concentration risk is elevated due to dependence on limited defense agencies or prime contractors.

Switching costs arise primarily from strict qualification processes and the operational criticality of components making supply chain continuity essential for end-users. Peer firms often blend precision component manufacturing with broader systems integration expertise; compared to that complex landscape MOBIX is more narrowly focused on discrete hardware components that serve as critical “buy” items for prime assembly stages.

Emerging Growth Catalysts from Defense Demand

An acute growth driver highlighted in recent filings is a surge in orders for filter connectors used across defense platforms—capturing an uptick linked to increased geopolitical tensions driving accelerated funding towards drone countermeasures and missile system refresh cycles [S2]. This demand may translate into stepping-up production volumes over near quarters if manufacturing scale can keep pace.

Additional catalysts include potential expansion into adjacent aerospace components leveraged through existing technical capabilities plus fresh contract wins arising from growing U.S. government spending targeting modernized defense infrastructure. Increased military emphasis on unmanned systems further contextualizes strategic relevance of MOBIX’s anti-drone technologies.

However, while order volume momentum looks promising structurally, total revenue impact remains moderated by MOBIX’s constrained manufacturing capacity and capital base which limits rapid scaling absent further investment or partnerships.

Risk Factors: Liquidity Stress and Nasdaq Compliance Challenges

The company faces pronounced liquidity stress reflected by its latest balance sheet metrics showing current assets around $5.5 million versus current liabilities exceeding $24 million for a severely depressed current ratio of approximately 0.23 [F1]. Such imbalance signals tight working capital conditions undermining financial flexibility.

Persistent net losses—the latest annual operating loss tally approaches -$37.7 million—compound financing risk constraints while underscoring ongoing challenges achieving sustainable profitability [F1]. The executed reverse stock split was necessary mainly due to prolonged sub-$1 share prices triggering Nasdaq compliance warnings with imminent delisting threats absent corrective actions [S2][S22].

Nasdaq mandates not only impose minimum bid price floors but also require maintenance of market capitalization (generally $35 million) and public holder counts that have previously been at risk [S2]. Failure to sustain these parameters could result in immediate delisting since previous reverse splits exclude grace periods per Nasdaq policies.

This precarious financial environment creates heightened execution risk where inability to refinance or raise equity on reasonable terms could disrupt operational continuity or limit scale growth efforts despite favorable product market fit.

Near-Term Milestones and Pivotal Indicators to Watch

Key indicators for assessing MOBIX’s trajectory include monitoring subsequent quarter filings for liquidity changes post note amendment conversion; tracking order backlog trends especially related to filter connectors; observing share price stability above Nasdaq thresholds through at least April 2027; and evaluating management performance under CEO Phil Sansone who assumed leadership mid-2025 focusing on financial stabilization [S2]

Capital raising initiatives or partnership announcements will also signal strategic intent to shore up working capital constraints needed for ramping manufacturing output aligned with burgeoning defense sector demand.

Investor attention should particularly focus on operational execution timelines translating contracts into revenue growth paired with careful scrutiny of market regulator communications that could affect listing status.

Summarized Financial Profile

MOBIX currently exhibits a challenging financial profile typified by acute liquidity limitations—current assets approximate $5.5 million against over $24 million in short-term obligations producing a current ratio near 0.23—indicating strained short-term solvency [F1]

Total debt reported stands at roughly $3.93 million from late 2025 figures partially addressed through recent convertible note conversions into equity shares extinguishing significant debt burdens [F1][S3]. Nonetheless, available cash balances measured only about $7,500 as of September 2023 illustrating cash flow fragility under ongoing net losses exceeding -$46 million annually at last fiscal year-end [F1].

This backdrop necessitates prudent capital management while leveraging recent defence technology sector demand spikes as an opportunity pathway toward achieving operational breakeven enabling renewed financial resilience.

This analysis synthesizes publicly filed SEC disclosures and companyfacts data combined with domain-native industry context aimed at elucidating MOBIX LABS’ current operating environment without offering investment advice or price projections.

Financial position in context

Current assets of $5mm and current liabilities of $24mm imply a current ratio near 0.23x for 2026-03-31 [F1]

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments