Medical Properties Trust Navigates Tenant Challenges and Capital Pressures Amid Revenue Declines

Healthcare-focused REIT contends with concentrated tenant risks and impairment charges in a complex regulatory and economic environment.

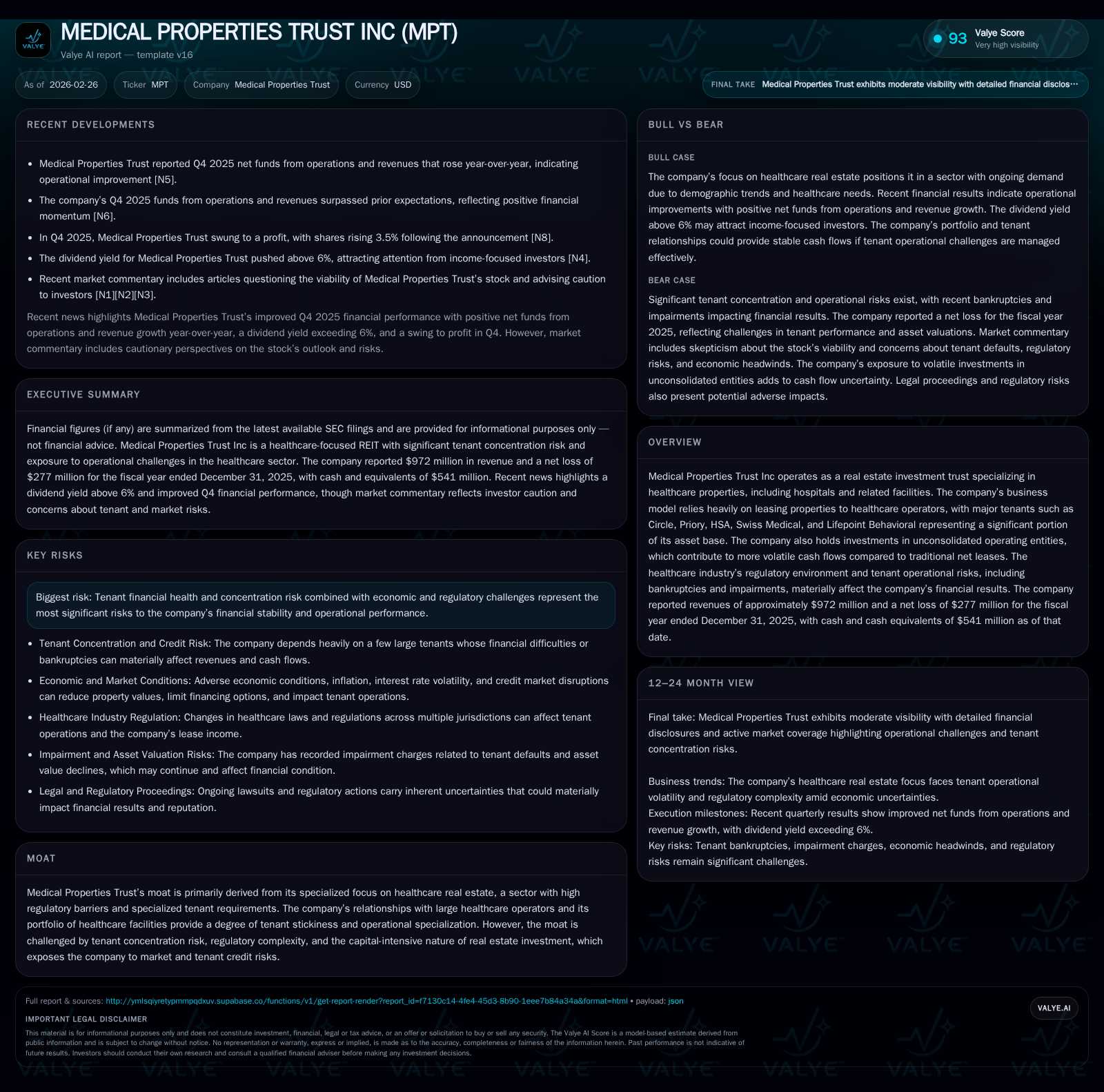

Medical Properties Trust Inc (MPT) saw revenues decline to $972 million in 2025, continuing pressures from tenant bankruptcies and impairments. Despite narrowing net losses to $277 million, tenant credit risk and regulatory challenges weigh on cash flows. The company retains over $540 million in liquidity and pursues disciplined capital allocation with dividends yielding above 6% alongside modest share repurchases. Key near-term focus includes tenant performance, lease renewals, and asset valuations amid volatile healthcare real estate markets.

Historical Financial Performance

Medical Properties Trust's revenue trajectory illustrates ongoing headwinds within its specialized healthcare real estate portfolio. Revenues peaked at approximately $1.54 billion in FY2022 before contracting sharply to about $872 million in FY2023, with a modest recovery to $972 million in FY2025 [F1]. This decline is linked primarily to operational disruptions among key tenants, including bankruptcies.

The net income pattern reflects significant volatility: a profitable $903 million in FY2022 gave way to deep losses surpassing $2.4 billion in FY2024 before narrowing to a loss of $277 million in FY2025. These results incorporate large impairment charges associated with bankruptcies of major tenants such as Steward Health Care and Prospect Medical Holdings [S7][S11].

Operating cash flow has remained positive but declined from $739 million in FY2022 to $231 million in FY2025, highlighting pressures on cash generation due to tenant credit issues and lease restructurings [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($bn) | CFO ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|

| 2025 | 972 | -0.3 | 231 | -2.4% | +88.5% |

| 2024 | 996 | -2.4 | 245 | +14.2% | -333.1% |

| 2023 | 872 | -0.6 | 506 | -43.5% | -161.7% |

| 2022 | 1543 | 0.9 | 739 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | ROE% |

|---|---|---|

| 2025 | 23 | -6.0 |

| 2024 | 18 | -49.9 |

| 2023 | 18 | -7.3 |

| 2022 | 18 | 10.5 |

Source: SEC companyfacts cache [F1].

Source: Company filings [F1]

Business Model & Market Position

MPT operates as a healthcare-focused REIT investing predominantly in properties leased under triple-net or loan arrangements to healthcare operators globally. The company’s niche expertise lies in managing specialized hospital and behavioral health facilities subject to complex regulations including patient privacy laws and reimbursement frameworks [S6][S9].

The competitive moat arises from this specialization combined with the difficulty of repurposing these assets for alternative uses. However, the portfolio’s high tenant concentration—where the five largest tenants constitute over 40% of total assets—exposes MPT to material credit risk tied directly to operator performance [S7][S10].

Additionally, investments in unconsolidated operating entities (~$300 million or ~2% of total assets) introduce greater earnings variability since returns depend on operators’ business outcomes rather than fixed rents [S6].

Tenant Credit Risk & Regulatory Environment

Tenant financial health remains MPT's principal risk factor. Recent bankruptcies such as Steward Health Care (in 2024) and Prospect Medical Holdings (in 2025) have resulted in impairment charges affecting earnings and asset values [S7][S11]. Bankruptcy proceedings can delay collections or require replacement of operators—a complex process given stringent licensing requirements across jurisdictions.

Tenants also face evolving regulatory challenges including cybersecurity risks impacting protected health information systems, which may lead to enforcement actions or reputational harm affecting their financial viability. Labor shortages within healthcare further elevate operational costs potentially impacting rent payments [S6][S9].

Liquidity & Capital Structure

As of December 31, 2025, MPT held approximately $541 million in cash and equivalents, providing liquidity support amid uncertain market conditions [F1][S13]. The company actively manages its debt profile through refinancing amid elevated interest rates and tightening credit availability affecting the REIT sector broadly [S7][S8].

Equity capital has contracted from roughly $8.59 billion in FY2022 to about $4.6 billion by FY2025 due primarily to impairment charges reflecting the challenging operating environment for key tenants [F1].

Capital Allocation: Dividends & Repurchases

MPT maintains dividend yields exceeding 6%, reflecting its commitment to shareholder returns despite balance sheet pressures. In fiscal year 2025, share repurchases were modest at approximately $23 million under cautious capital return policies aligned with preserving liquidity amid operational risks [N4][F1][S15].

Growth Outlook & Strategic Considerations

Near-term growth depends critically on improving tenant financial stability and mitigating concentration risks through diversification or restructuring master leases involving major tenants such as Circle Health and Priory Group [N5][S10]. Acquisition activity appears limited given current interest rate conditions constraining accretive financing.

Redevelopment opportunities within existing properties could provide incremental value if market conditions permit upgrades aligned with shifting care delivery models like outpatient behavioral health services.

Monitoring lease expiration schedules—especially those subject to cross-default provisions—and regulatory developments will be essential for assessing re-leasing prospects or impairment risks. Macroeconomic factors including inflationary wage pressures on healthcare workers also influence tenant profitability and thus MPT’s lease cash flow stability.

Conclusion

Medical Properties Trust faces a challenging operating environment marked by significant tenant credit risk, regulatory complexity, and capital market pressures that have eroded equity capital while compressing revenues and earnings. The company's liquidity position affords some flexibility as it navigates these headwinds.

Investors should focus on updates regarding tenant financial health, lease renewal outcomes especially for concentrated master leases, impairment recognition trends under GAAP accounting standards, and broader credit market dynamics shaping cost of capital for healthcare real estate investments.

This analysis is based solely on publicly available information as of February 26, 2026 and is not investment advice.

Comments