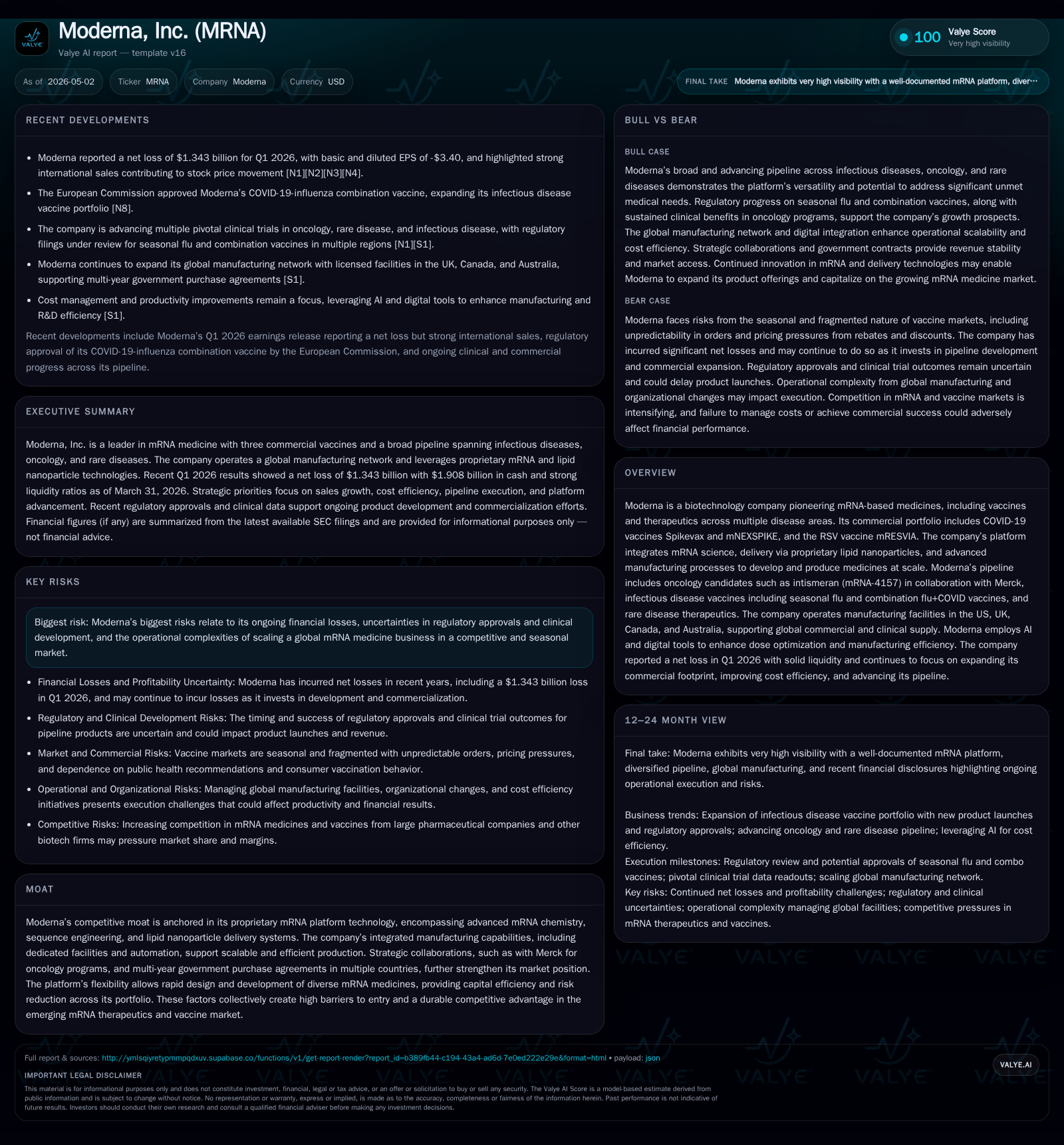

Moderna Advances mRNA Pipeline While Managing Post-Pandemic Commercial and Regulatory Challenges

The latest quarter reflects Moderna's transition from pandemic-driven sales to diversified mRNA vaccines and therapeutics amid competitive and regulatory headwinds.

Moderna’s Q1 2026 results spotlight a strategic pivot from COVID-centered revenues toward broader infectious disease, oncology, and rare disease assets. The company’s proprietary mRNA platform underpins a growing pipeline including combination flu-COVID vaccines, personalized cancer therapies in partnership with Merck, and rare metabolic disorder treatments. However, seasonal vaccine demand variability and evolving regulatory landscapes temper near-term commercial visibility. Operational scale and AI integration support cost efficiency efforts as Moderna seeks sustained growth beyond its initial pandemic blockbuster products.

Recent Operating Update

Moderna's 10-Q filing for Q1 2026 [S2] reveals the company is navigating a pivotal phase transitioning from peak pandemic vaccine sales toward a diversified mRNA portfolio. Revenue continues to derive largely from COVID-19 vaccines Spikevax and the recently launched mNEXSPIKE in the U.S., alongside early commercial activity for the RSV vaccine mRESVIA. Despite a net loss reported in the quarter consistent with rising R&D and SG&A investments required for pipeline expansion [N2], Moderna's robust operational focus remains evident.

Supplementary disclosures [S3] emphasize ongoing progress in clinical trials and commercial launch strategies. Key regulatory submissions are underway globally for next-generation respiratory vaccines, including the seasonal flu+COVID combination candidate (mRNA-1083) and standalone seasonal flu vaccine mRNA-1010. FDA's acceptance of an amended BLA for mRNA-1010 with a PDUFA target date of August 5, 2026, marks a critical near-term catalyst [S1]. This process involves a revised submission strategy targeting partial approval in adults aged 50–64 years and accelerated approval pathways for those over 65, reflecting strategic regulatory engagement.

Business Model

At its core, Moderna operates an integrated biotechnology model built around its proprietary messenger RNA (mRNA) platform. This platform combines advanced mRNA chemical engineering with tailored lipid nanoparticle (LNP) delivery systems to enable rapid design, manufacturing flexibility, and scalable production of vaccines and therapeutics [S1]. Revenue is generated primarily through sales of authorized vaccines whereby governmental bodies, healthcare providers, or retail customers contract for doses delivered either via direct purchase agreements or through channel partners.

Product pricing reflects not only dosage volumes but also varies by indication—COVID vaccines commanded premium pricing during the acute pandemic phase supported by multi-year government agreements; however, pricing power faces downward pressure as markets shift toward endemic management scenarios [S4][S6]. The company’s commercial footprint extends across North America, Europe, Asia-Pacific markets with local teams that leverage expertise in vaccine distribution logistics given the seasonal nature of its key product categories [S22].

Cost efficiency initiatives are increasingly driven by digital transformation: internal AI tools facilitate dose optimization (Dose ID GPT), clinical trial management enhancements, and automated manufacturing controls to reduce per-unit production costs while preserving batch quality [S1][S22].

Industry Structure and Competitive Position

Moderna competes within several intersecting segments: pandemic/seasonal respiratory vaccines (primarily COVID-19 and influenza), emerging therapeutic fields such as oncology neoantigen therapies, and rare genetic diseases treated via therapeutic mRNAs.

In respiratory vaccines, Moderna’s chief competitor remains Pfizer/BioNTech which produces similarly positioned mRNA COVID-19 vaccines. In addition to biological competition from Sanofi, Novavax (non-mRNA approaches), GlaxoSmithKline (RSV market incumbent), and others impose upward pressure on R&D intensity due to cyclical vaccination schedules influenced by evolving immunization policies [S6]. The competitive intensity necessitates technological differentiation; Moderna’s edge includes integrated manufacturing scale with flexible suites capable of parallel production runs supporting distinctive dose formats or indications [S1].

In oncology, collaboration with Merck on intismeran (mRNA-4157), an individualized neoantigen cancer vaccine candidate, situates Moderna strategically in personalized cancer immunotherapy—a field characterized by rapid innovation cycles but fraught with clinical development risk. Early-phase data demonstrate promising recurrence-free survival gains in high-risk melanoma patients post-surgery [S1], underscoring a potential new growth vector although timeline uncertainties remain inherent due to regulatory complexities.

Rare disease ventures such as propionic acidemia therapy (mRNA-3927) leverage targeted patient populations where treatment options have historically been limited. Regulatory designations like rare pediatric disease vouchers offer incentives but require costly registrational studies before commercialization can be realized [S1].

Growth Drivers

Pipeline Progression

The company's development efforts span late-stage pivotal studies bolstering its eventual commercial pipeline breadth. The Phase 3 norovirus vaccine candidate enrolled its second season cohort successfully supporting future registration filings [S1]. For influenza-related vaccines including mono- and combination products addressing respiratory disease pathogens (mRNA-1010 & mRNA-1083), regulatory reviews across multiple jurisdictions represent high-impact inflection points.

Oncology growth hinges on clinical trial progression; eight Phase 2/3 studies are active for intismeran across various tumor indications with synergistic immuno-oncology combos using Merck’s pembrolizumab (KEYTRUDA®). Positive readouts here would validate Moderna’s extension beyond infectious diseases into chronic disease treatment paradigms.

Manufacturing Footprint & Digital Transformation

A key enabler is Moderna's geographically distributed manufacturing network across the US, UK, Canada, and Australia which supports global supply resilience. Its platform affords rapid molecule design-to-production cycles reducing time-to-market compared to traditional biologics workflows [S1]. Enhanced use of generative AI further fuels productivity gains impacting both R&D throughput and operational cost structure providing scalability advantages relative to peers reliant on legacy modalities.

Commercial Expansion & Market Penetration

While COVID demand has moderated since peak pandemic phases—a headwind moderating near-term topline growth—the introduction of novel products such as RSV vaccine offers incremental revenue opportunities albeit currently at smaller volumes due to market entry timing against established competitors (e.g., Pfizer's Abrysvo RSV vaccine) [S6]. Expanding regional approvals along with incremental uptake of updated respiratory combo shots support base case market growth into mid-decade.

Risks / Watchpoints / Constraints

Regulatory uncertainty continues to hem growth momentum; variability exists between FDA guidance versus international counterparts on vaccine composition and indication scopes creating operational complexity in portfolio rollout timing [S4]. Policy shifts around post-marketing safety commitments increase compliance costs for dose monitoring impacting margins.

Market adoption risk is tangible especially where advisory committee recommendations dampen vaccination enthusiasm—as observed with RSV uptake below expectations—and potential pricing pressures arise from competitive entrants or government-mandated drug price frameworks such as Medicare Part D negotiations initiated under the Inflation Reduction Act [S4][S16].

Operational execution challenges include managing ongoing intellectual property litigations against rivals Pfizer/BioNTech and others over foundational mRNA patents that could impair commercialization rights [S8][S14][S19]. Product liability exposure inherent in vaccine distribution adds additional legal risk layers impacting corporate reputation and cost reserves [S23].

Financial losses in recent quarters stem in part from R&D intensification necessary to fund complex oncology trials and rare disease registrational studies; failure to successfully execute these programs or capture anticipated market share would imperil sustainability.[N2][S4]

What to Watch Next

Key near-term catalysts include:

- FDA PDUFA decision anticipated by August 5, 2026 on amended BLA for seasonal flu vaccine candidate mRNA-1010.

- Readouts from Phase 2/3 oncology trials evaluating efficacy signals of intismeran alongside pembrolizumab partnership.

- Enrollment completion milestones for rare disease therapeutics such as propionic acidemia program potentially unlocking global commercialization pacts.

- Market uptake trajectories of newly launched products mNEXSPIKE (COVID) in retail channels plus expansion efforts for RSV vaccine reflecting commercial execution capability.

- Progress in patent litigation outcomes particularly appeals pending at Federal Circuit level affecting platform exclusivity dynamics.

- Pricing environment developments including government policy shifts tied to Medicare drug price negotiations influencing gross-to-net spreads.

Financial Profile Note

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $1908mm | |

| 2026-03-31 | ||

| Total debt | $590mm | |

| 2026-03-31 | ||

| Net debt | $-1318mm | |

| 2026-03-31 | ||

| Current assets | $5.8bn | |

| 2026-03-31 | ||

| Current liabilities | $2.4bn | |

| 2026-03-31 | ||

| Current ratio | 2.41x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

As of March 31, 2026, Moderna holds $1.908 billion in cash and equivalents against $590 million total debt resulting in net cash approximating $1.318 billion. Current assets stand at $5.77 billion vs current liabilities of $2.395 billion yielding a healthy current ratio of approximately 2.41 suggesting strong near-term liquidity [F1]. This capital base underpins ongoing investment capacity into R&D pipeline while supporting operating expenditures amidst reduced COVID revenue contributions post-pandemic.

Disclaimer

This analysis is intended solely to provide an informative business overview based on publicly available filings and does not constitute investment advice or recommendations regarding any security or company.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments