Vaxart Advances Oral Vaccine Platform with Dynavax Partnership Extending Runway to 2027

Recent licensing deal with Dynavax for oral COVID-19 vaccine candidate and BARDA contract progress reshape Vaxart’s near-term prospects.

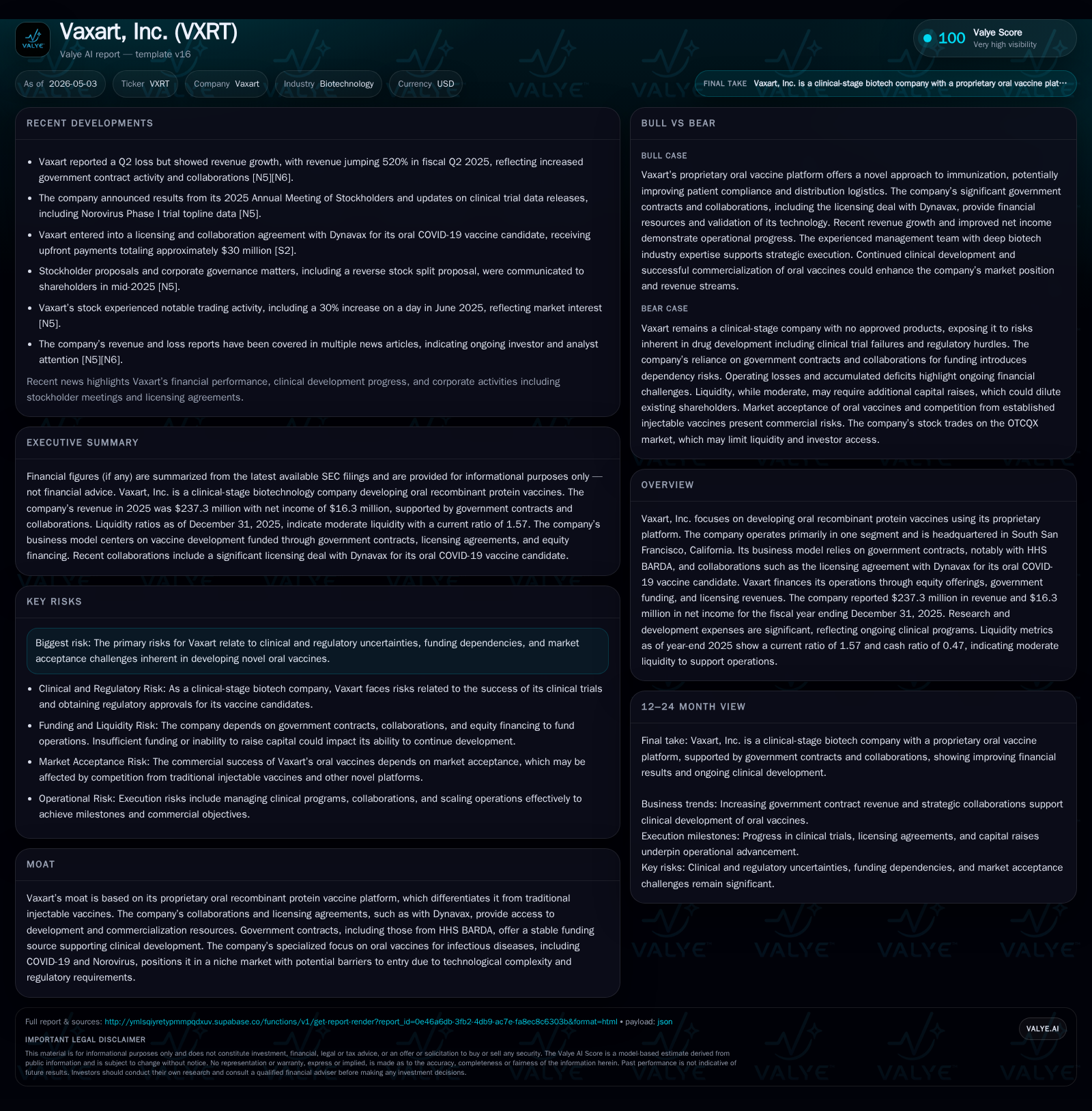

Vaxart, Inc. is anchored in developing oral recombinant protein vaccines, uniquely positioning itself within the vaccine technology niche. The latest 10-Q reveals a significant revenue increase driven by government contracts, facilitating ongoing R&D investment amid operating losses. A November 2025 licensing and equity transaction with Dynavax injects $30 million of capital, extending the cash runway into mid-2027 and alleviating prior going-concern doubts. The company’s business model relies on partnerships, government funding, and licensing fees, targeting infectious diseases via oral vaccines that may offer convenience and compliance advantages. While clinical and regulatory uncertainties persist, Vaxart’s proprietary platform and collaboration network underpin a differentiated competitive stance. Monitoring clinical trial milestones and regulatory interactions will be critical for assessing future inflection points.

Recent Operating Update

Vaxart's latest quarterly report filed on November 13, 2025 [S2] reveals substantial operational developments shaping the company's near-term outlook. Revenue rose dramatically to $72.4 million through the first nine months of 2025, predominantly driven by government contracts—an explosive increase from $4.9 million in the same period a year earlier [S6]. This surge is attributable to enhanced funding from HHS BARDA under its Advanced Technology International Respiratory Recombinant Protein Vaccine (ATI-RRPV) contract.

Critically, in early November 2025, Vaxart entered a strategic License and Collaboration Agreement with Dynavax Technologies Corporation alongside an equity Purchase Agreement [S5][S20]. Dynavax acquired an exclusive global license to develop and commercialize Vaxart's oral COVID-19 vaccine candidate. The financial terms included a $25 million upfront license fee paid directly to Vaxart plus $5 million via common stock purchase at $0.45 per share—a combined influx of approximately $30 million [S5]. This capital injection significantly extends Vaxart’s cash runway into Q2 2027 [S5], alleviating prior material uncertainties about its short-term liquidity that had raised doubts about its status as a going concern.

While the company reported an operating loss narrowing to around $37 million for the nine months ended September 30, 2025 [S6], its strategic focus on advancing oral vaccine candidates remains intact bolstered by this fresh capital and ongoing government support.

Business Model

Vaxart operates primarily as a pre-commercial clinical-stage biotechnology firm focused exclusively on oral recombinant protein vaccines leveraging proprietary delivery technology [S1]. Unlike conventional injectable vaccines requiring cold-chain logistics and needles, Vaxart’s platform uses oral tablet formulations intended to stimulate mucosal immunity along with systemic immune responses. This mode aims to enhance patient compliance, reduce administration costs, and broaden accessibility—potentially disrupting traditional vaccine paradigms.

Revenue generation is mainly through three channels:

- Government Contracts: Substantial non-dilutive funding from agencies like HHS BARDA supports clinical trial activities. Contract revenue recognition follows milestone or cost-reimbursable models depending on specific agreements [S6][S14][S25].

- Licensing Agreements: Strategic partnerships such as the recent Dynavax pact provide upfront fees and potential downstream royalties contingent on successful product development and commercial launch [S20].

- Equity Financings: To cover extensive R&D expenses absent product sales, the company raises funds via public equity offerings as needed [S17].

Margins are currently negative given ongoing heavy R&D outlays including external program costs (notably large spend on COVID-19 clinical trials exceeding $66 million year-to-date through Q3) balanced against limited revenue outside government shipments [S6][S25]. General administrative expenses remain moderate relative to R&D efforts.

The business model is thus investment-heavy with an extended clinical development timeline before potential commercialization revenue streams materialize.

Industry Structure and Competitive Position

The global vaccine development sector is dominated by established pharma players focusing on injectable modalities. Within this landscape, Vaxart occupies a specialized niche centered on oral vaccines—an area which remains underdeveloped commercially due to technical complexities but offers meaningful advantages if proven effective.

Vaxart's moat derives principally from its proprietary oral recombinant protein vaccine platform combined with accumulated intellectual property rights—creating barriers against new entrants lacking similar technology capabilities. Collaborations such as the license deal with Dynavax not only bring in capital but also align commercial expertise beneficial for navigating regulatory pathways and eventual market access.

Government partnerships are essential in this sector due to high capital requirements and public health imperatives; BARDA support provides both validation and financial stability to the company’s programs.

However, competition exists at multiple levels: other biotech firms exploring oral or needle-free vaccines (though fewer have advanced clinical pipelines), legacy injectable vaccine manufacturers with ingrained relationships across markets, and emerging mRNA platforms which continue to reshape vaccine R&D priorities.

The distinctiveness of Vaxart’s approach lies in targeting mucosal immunity through oral dosing potentially facilitating immunization strategies in pandemics or endemic infections difficult to control otherwise.

Growth Drivers

Pipeline Advancement

The foremost growth driver is successful advancement of Vaxart's lead candidates, particularly the oral COVID-19 vaccine. Positive phase 2b trial results combined with FDA advisory actions like End of Phase 2 meetings would reinforce regulatory confidence opening paths towards pivotal trials or accelerated pathways [S10][S20].

Government Funding Continuity

Continued funding under BARDA contracts remains critical enabling pipeline progression without immediate need for dilutive financings. Expansions or renewals augment stability amidst volatile biotech financing climates.

Strategic Partnerships & Licensing Deals

Building additional collaborations following the Dynavax deal could bring expertise for commercial scale manufacturing or international distribution while monetizing assets early via licensing structures.

Expansion Beyond COVID-19

Broader application of the oral platform to target other infectious diseases such as norovirus may diversify risk while leveraging existing technological know-how enhancing long-term growth potential [F1].

Market Demand for Oral Vaccines

Increasing interest globally in non-injectable vaccines driven by patient preference trends and logistical considerations supports structural demand growth for products like those developed by Vaxart.

Risks / Watchpoints / Growth Constraints

Clinical Development Risks

As with all biotech ventures, clinical trial outcomes are inherently uncertain. Failures or delays at any stage – including immunogenicity endpoints or safety issues – could materially impair asset value.

Regulatory Approval Complexity

The novel nature of oral recombinant protein vaccines may invite rigorous scrutiny from regulators requiring additional data or novel biomarker validation extending timelines beyond current expectations.

Market Acceptance & Competition

Despite theoretical advantages, market adoption depends heavily on payer reimbursement decisions and competitive dynamics against entrenched injectable products or emergent mRNA-based substitutes.

Capital Intensity & Financing Risk

Although recent deals have improved liquidity visibility through mid-2027 [S5], sustained high R&D expenditures could require further capital raises under potentially unfavorable conditions impacting shareholder dilution.

Litigation Exposure

Historical securities class action litigation resolved via settlement introduces reputational considerations though does not presently forecast material operational disruption [S7][S9].

What to Watch Next

- Progress reports from Phase 2b COVID-19 vaccine trial including safety/immunogenicity readouts scheduled over upcoming quarters.

- Outcomes of FDA End of Phase 2 discussions shaping pivotal trial design requirements.

- Updates on pipeline expansion beyond COVID-19 indications such as norovirus vaccine development milestones.

- New partnership announcements or additional licensing agreements replicating Dynavax’s model enhancing financial flexibility.

- Quarterly financial disclosures revealing burn rate trends relative to remaining cash runway extending into Q2 2027.

- Regulatory filings associated with candidate products including potential Investigational New Drug (IND) advancement or Marketing Authorization Applications (MAA).

Financial Profile Overview

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Current assets | $136mm | |

| 2025-12-31 | ||

| Current liabilities | $87mm | |

| 2025-12-31 | ||

| Current ratio | 1.57x | |

| 2025-12-31 |

Source: SEC companyfacts cache [F1].

Vaxart reported full-year ending December 31, 2025 revenue of approximately $237.3 million driven almost entirely by government contracts supported by BARDA funding [F1]. Operating income unexpectedly turned positive at $18.1 million reflecting license fees combined with cost management efforts while net income settled at $16.3 million [F1], marking a rare profitability milestone for a clinical-stage biotech absent commercial products.

Balance sheet strength improved markedly with current assets totaling $136.1 million versus current liabilities at $86.8 million yielding a healthy current ratio of 1.57 by year-end [F1]. Cash equivalents stood near $22 million as of September 30, 2024 [F1], supplemented by licensing revenues received subsequent to that date per filings [S5]. Total debt appears modest relative to cash levels (~$17.7 million last reported in 2018) resulting in an approximate net cash position [F1].

Despite net losses reported during interim periods in FY2025 [S21], the infusion from Dynavax solidifies liquidity enabling uninterrupted clinical progress through mid-2027 without immediate refinancing pressures [S5]. The company continues managing expenses prudently while investing heavily in R&D programs essential for value creation.

Disclaimer

This analysis is for informational purposes only based on publicly available filings as referenced. It does not constitute investment advice or recommendations regarding Vaxart securities or any other instrument.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments