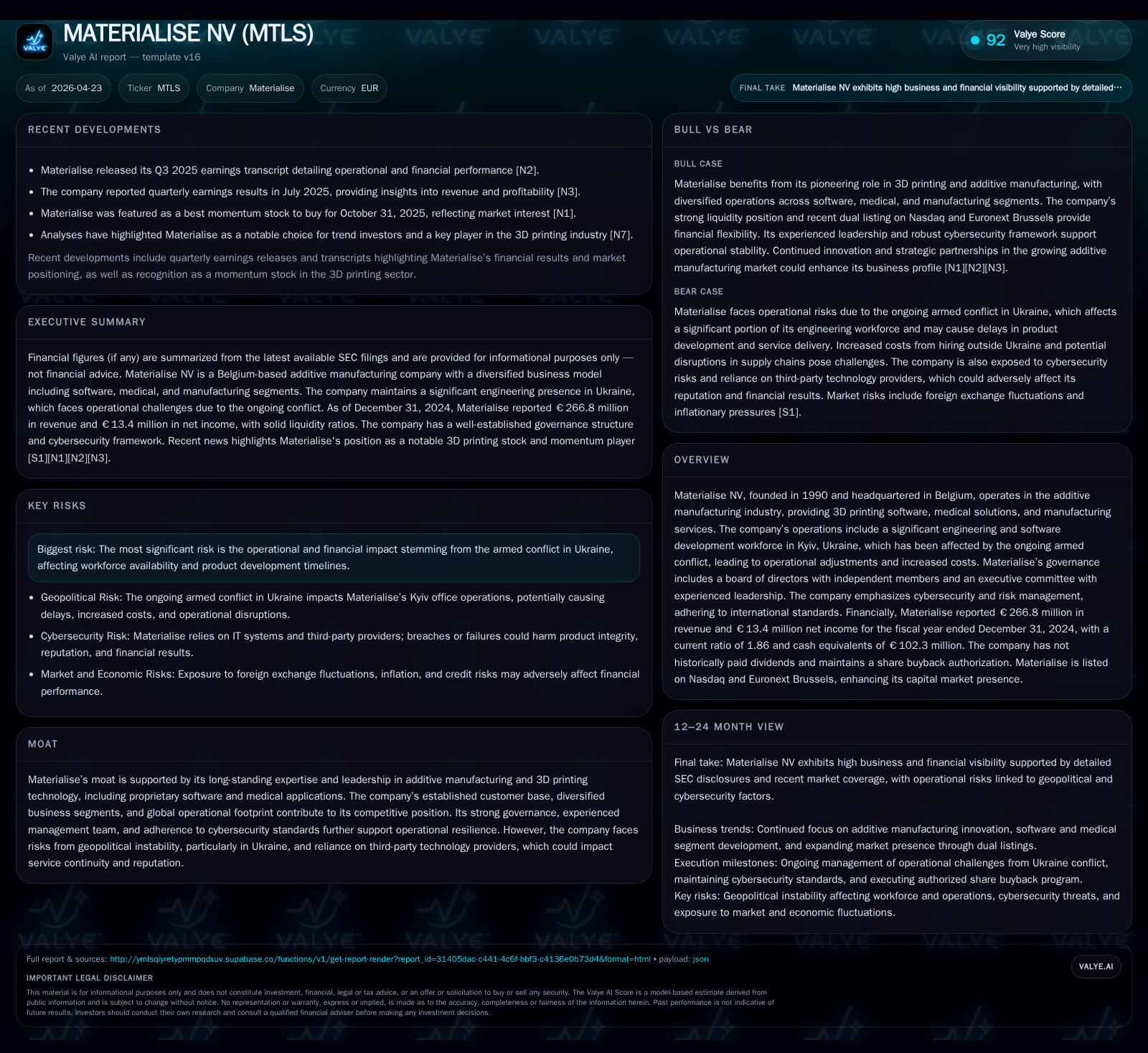

Materialise NV Advances Through Operational Adjustments Amid Geopolitical Strain

Materialise NV’s latest quarterly disclosures reveal operational resilience strategies in response to Ukraine-related disruptions while leveraging its software-led additive manufacturing portfolio.

Materialise NV’s April 2026 filings spotlight ongoing impacts from the armed conflict in Ukraine on its Kyiv-based engineering workforce, prompting strategic operational adjustments and increased costs. The company continues to capitalize on its core proprietary 3D printing software and medical solutions, sustaining customer service with mitigations through relocated personnel. While geopolitical risks create near-term growth constraints and delay certain product developments, Materialise’s diversified business model and strong liquidity provide a foundation for resilience. Key upcoming catalysts include the execution of its ADS buyback program and pending software releases critical to sustaining competitive advantage.

Latest Quarterly Update: Navigating Operational Risks during Conflict

Materialise NV’s most recent filings in April 2026 ([S2], [S3]) provide an essential update on how ongoing geopolitical tensions in Ukraine continue to mold its operational landscape. The company maintains a significant engineering and software development presence in Kyiv—over 400 collaborators primarily engaged in advanced software development and IT functions ([S1], [S17]). Despite the armed conflict’s disruptions causing personnel displacement, Materialise has managed to sustain customer service continuity by reallocating responsibilities to similarly skilled teams across other geographies such as Wroclaw or remote arrangements.

However, the environment has necessitated increased expenditures related to hiring more costly external resources outside Ukraine, pressuring operational expenses ([S1]). These workforce challenges have also contributed to delays in some scheduled product releases within Materialise Software and Medical units. The firm emphasizes the unpredictability of the conflict's trajectory making it difficult to forecast precise impacts on service or financial outcomes.

This candid operational disclosure underscores Materialise’s balancing act: preserving delivery standards while absorbing inflation-driven cost increases attributable both to labor market shifts and global economic pressures ([S4], [S5]).

Core Business Model: Software, Medical Solutions, and Manufacturing Services

Materialise's business model strategically spans three integrated segments: proprietary additive manufacturing software platforms (largely SaaS and cloud-based), specialized medical technology solutions tailored for 3D printing applications in healthcare, and contract manufacturing services that leverage vertically integrated additive production capabilities ([S1]).

The company's growth levers are anchored primarily in the software segment. Its proprietary SaaS offerings enable customers across industrial design and healthcare sectors to streamline complex 3D printing workflows while simultaneously embedding recurring revenue stability through licensing fees. This model benefits from substantial switching costs driven by Materialise's deep engineering expertise supporting custom implementations.

Simultaneously, Materialise Medical focuses on device validation, regulatory compliance (FDA/CE marking), and tailored clinical applications enhancing its moat against commoditization risks common in digital fabrication ([S1]). The Manufacturing segment serves as both a revenue contributor and an internal capacity extension that synergizes with customer-facing software solutions.

The company's worldwide footprint—including established sales channels across Europe, North America, Asia-Pacific—and a mature R&D engine further diversify its exposure to multiple end markets ensuring resilience against isolated economic shocks.

Competitive Position and Industry Dynamics in Additive Manufacturing

Within additive manufacturing's highly technical ecosystem, Materialise distinguishes itself primarily through software innovation combined with domain-specific medical applications ([S1], [F1]). This segmentation fosters notable pricing power not easily replicated by hardware-centric competitors who often compete on volume or machine sales.

Regulatory complexities governing medical device additive manufacturing represent both barriers to entry for newcomers and protect incumbents like Materialise whose solutions comply with stringent certification standards (e.g., ISO 13485) ().

Capacity constraints at an industry level persist due to supply chain burdens affecting raw materials for powder-bed fusion processes and printer availability. While this restricts some scaling potential for physical printing services within Manufacturing segment customers demand elasticities remain differentiated by verticals served; industrial clients exhibit more gradual adoption compared to healthcare providers requiring validated patient-specific solutions.

Growth Drivers: Innovation and Market Penetration

Research & Development is pivotal as Materialise prioritizes enhancement of its SaaS platform capabilities—particularly cloud scalability and AI-driven workflow automation—which promise disruptive efficiencies. Despite partial delays attributable to the Ukrainian situation affecting developer availability ([S1]), innovation remains a cornerstone for medium-term growth.

Geographically, expansion into underserved markets via digital health initiatives coupled with partnerships accelerates adoption curves especially underpinned by telemedicine trends post-COVID-19 (). Further penetration into medical device OEM partnerships provides avenues for co-development licensing revenues offering predictability beyond project-based manufacturing orders.

Financially stable with robust cash reserves like €102.3 million as of December 31, 2024 ([F1]), Materialise possesses the investment capacity needed to support aggressive R&D pipelines without immediate external financing dependence.

Growth Constraints: Geopolitical Instability and Cost Pressures

The primary headwind remains the continuation of armed conflict affecting Ukrainian-based operations—a critical risk factor acknowledged explicitly by management ([S1], [S17]). Rising inflation globally exacerbates input cost structures not fully recoverable via pricing mechanisms given competitive pressures prevalent within manufacturing contracts.

Further risks relate to reliance on third-party technology infrastructure underpinning its cloud SaaS offerings—failures here could critically hurt reputation or incur liability ([S16]). Exchange rate fluctuations introduce additional earnings volatility given significant revenues denominated outside Eurozone currencies ([S7]).

Consequently, these dynamics inject asymmetric risk where unexpected geopolitical shifts might force deeper operational relocations or prolonged product release deferrals extending possible revenue impact horizons.

Leadership, Governance, and Risk Management Framework

Under CEO Brigitte de Vet-Veithen's stewardship since January 2024 ([S17]), governance emphasizes rigorous cybersecurity protocols aligned with international ISO standards (ISO 27001/27701) essential for preserving trust in cloud-based services managing sensitive healthcare data ([S1], [S19]).

Executive Vice President Carla Van Steenbergen oversees legal affairs alongside procurement and M&A activities—reflecting comprehensive governance integration pivotal during turbulent external circumstances. Independent board members contribute oversight particularly around risk management frameworks ensuring shareholders’ interests remain protected amidst volatile externalities.

This blend of experienced leadership augmented by robust internal controls forms the backbone supporting continuity despite elevated external risk profiles.

Key Financial Metrics Reflecting Stability and Investment Priorities

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|

| 2024 | 267 | 13 | +4.2% | +100.2% |

| 2023 | 256 | 7 | +10.4% | +411.0% |

| 2022 | 232 | -2 | +12.9% | -116.4% |

| 2021 | 205 | 13 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2024 | 5.4 |

| 2023 | 2.8 |

| 2022 | -0.9 |

| 2021 | 5.7 |

Source: SEC companyfacts cache [F1].

Materialise’s FY2024 results demonstrate resilient financial health underpinning operational resilience: revenue rose modestly by approximately 4.2% year-over-year reaching €266.8 million while net income doubled from prior year to €13.4 million evidencing margin improvement ([F1]). Cash balance remained robust at €102.3 million supporting liquidity needs complemented by a current ratio of 1.86 signifying sound short-term financial stability ([F1]).

No dividends have been paid historically reflecting capital retention focused on reinvestment into growth initiatives ([S9]). However, recent authorization of an ADS Buyback Program totaling up to €30 million endorses management confidence in intrinsic value accretion opportunities ([S3], [S6], [S24]). This buyback initiative is executed via registered U.S. intermediaries enabling flexible capital return aligned with market conditions.

Catalysts Ahead: Milestones, Buyback Program, and Market Signals

Investor focus should center on the prospective resumption dates for deferred software releases critical for sustaining licensing revenue momentum disrupted by Ukrainian workforce availability challenges ([S2], [S3]). Monitoring Materialise’s adaptation of IT talent sourcing strategies beyond Ukraine will also inform execution feasibility through volatile periods.

The rollout pace of the buyback program serves as an important signal regarding board’s valuation outlook against share price dynamics amid broader macroconditions ([S3],[S24]). Additionally, periodic updates on order pipeline strength across medical OEM partnerships alongside evolving inflation pass-through effectiveness will provide nuanced insights into margin trajectory possibilities.

Together these factors constitute critical checkpoints shaping investment community expectations about Materialise’s ability to advance growth targets while managing prominent geopolitical headwinds.

Disclaimer: This analysis is for informational purposes based solely on publicly disclosed SEC filings dated April 2026 and related sources provided. It does not constitute investment advice or recommendations regarding securities of Materialise NV.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments