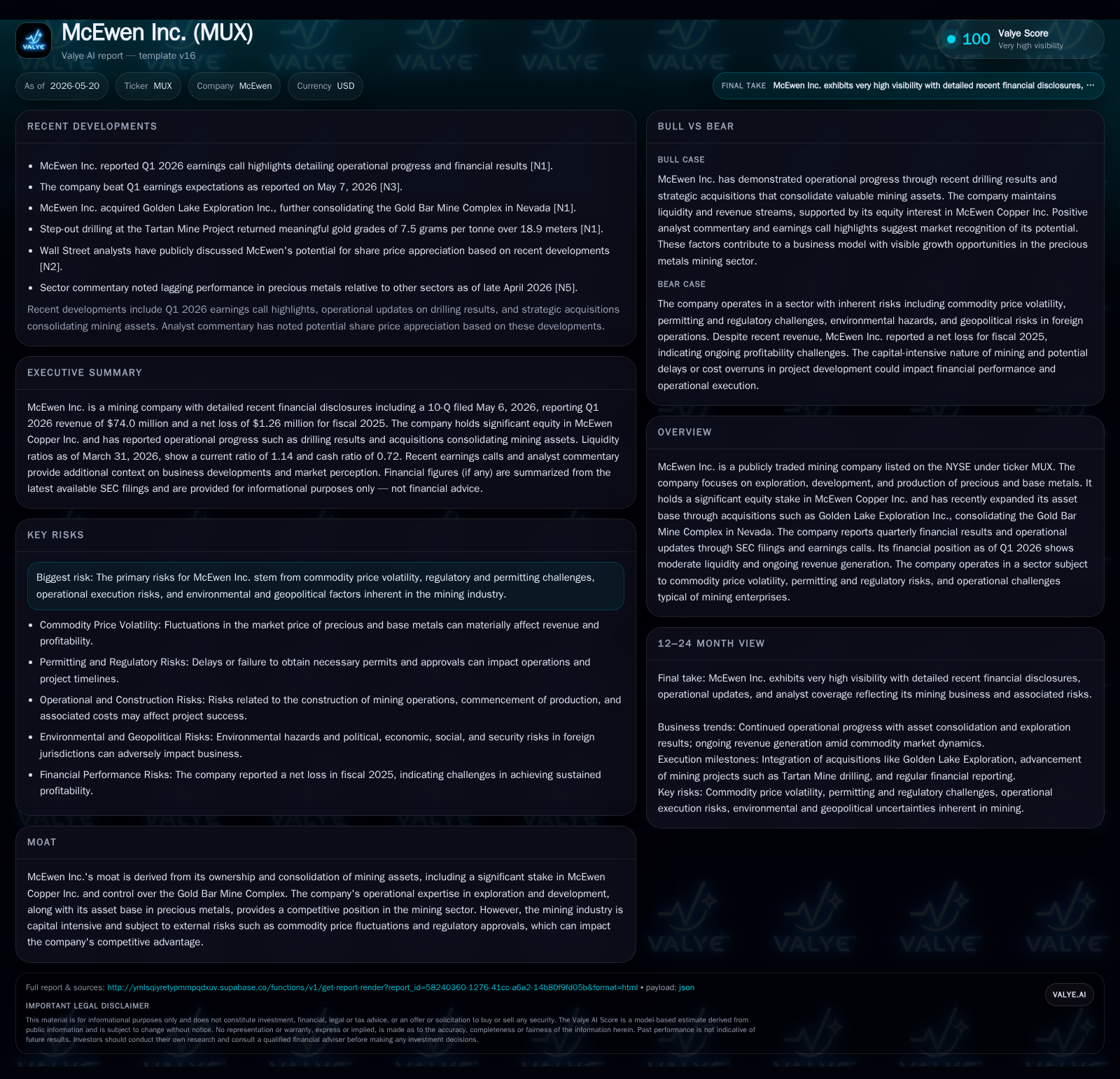

McEwen Inc. Boosts Asset Base and Navigates Commodity Volatility

Recent quarterly disclosures underline McEwen’s strategic asset consolidation and operational performance amid metal price fluctuations.

McEwen Inc.’s Q1 2026 filings reveal meaningful progress in expanding its mining asset portfolio, notably through the Golden Lake Exploration acquisition consolidating the Gold Bar Mine Complex in Nevada. The company is actively managing the cyclical pressures from volatile commodity prices while advancing exploration and development efforts. Its business model leverages both direct production and significant equity stakes, supported by operational expertise to unlock value. Key risks remain rooted in price swings, permitting timelines, and execution challenges intrinsic to mining operations.

Latest Quarterly Update: Operational Highlights from Q1 2026

McEwen Inc.’s latest Form 10-Q filed May 6, 2026 ([S2]) alongside the subsequent 8-K release ([S3]) provide a detailed snapshot of the company’s first quarter performance and strategic advances. The company reported sustained production levels consistent with prior guidance while indicating cost management initiatives that align with the volatile metals market environment. Notably, this quarter documents the recent completion of the Golden Lake Exploration Inc. acquisition executed via statutory plan of arrangement ([S27]), effectively consolidating ownership and operational control of the Gold Bar Mine Complex located in Nevada — a region recognized for its favorable ore grades and mining-friendly permitting framework.

This addition not only improves McEwen’s resource scale but also integrates synergistic exploration opportunities within a contiguous asset base. Operational updates accompanying this consolidation reflect anticipated ramp-up activities coupled with targeted investment in infrastructure enhancements aimed at extracting higher-margin reserves within the complex. The filings underscore ongoing development work at other projects such as Tartan Mine and Grey Fox Project with updated mineral resource estimates recently disclosed ([S21], [S29]). These indicate measured progress in upgrading resource confidence, supporting longer-term production outlooks.

Management commentary captured during the Q1 earnings call ([N1], [N2]) confirms resilience against headwinds tied to fluctuating gold and copper prices. The company benefits from its geographically diversified portfolio combined with agile operating practices designed to offset cyclical metal price volatility.

McEwen Inc.’s Business Model and Asset Portfolio

McEwen Inc. operates within the upstream mining segment focusing primarily on precious metals—chiefly gold—alongside growing exposure to base metals via its equity interest in McEwen Copper Inc., where it holds approximately 46.3% ownership ([S1]). The business model centers on creating shareholder value through a combination of direct mine production, exploration-driven asset expansion, strategic acquisitions, and equity investments in complementary ventures.

The core revenue mechanic involves converting mined ore into refined precious metal output sold into global commodity markets where pricing is dictated by spot and futures contracts sensitive to macroeconomic trends. Clients are wholesale commodity buyers rather than end consumers; thus, product differentiation relies heavily on ore grade quality, geographic location advantages (such as proximity to existing infrastructure), and efficient cost structures rather than branded product features.

Recent acquisitions like Golden Lake bolster McEwen’s reserves at Gold Bar Mine Complex—an asset already recognized for higher-grade gold deposits—which markedly improves scale economies by consolidating contiguous land holdings allowing for streamlined open-pit or underground operation expansions ([S27]). This also enhances optionality for future permitting phases by reducing external stakeholder complexity.

Operational quality factors influencing margins include ore grade variability, metallurgical recovery rates, energy costs given intensive processing requirements typical across base metal concentrate flows, and labor market stability influencing site-level throughput capacity. McEwen leverages technical expertise internally to optimize mine plans balancing near-term cash flow generation against capital-intensive development projects – an approach critical in an industry where permitting cycles can range from several months to multiple years depending on jurisdictional regulations.

Industry Dynamics and Competitive Positioning

The broader mining sector confronts structural challenges such as capital intensity requiring access to substantial funding sources for exploration drilling campaigns and mill expansions. Commodity pricing remains intrinsically cyclical; recent years’ volatility underscores significant margin pressure periods balancing intervals of strong cash flow generation opportunities.

Within this context, McEwen's competitive position is buoyed primarily by asset quality (high-grade Nevada properties) combined with strategic equity holdings amplifying exposure to copper—a metal benefiting from ongoing electrification trends globally ([S1]). However, competitive pressures emerge from peer producers who command broader scale or more diversified geographic footprints that may mitigate localized permitting risk or cost inflation.

The permitting environment—particularly in jurisdictions like Nevada—is generally viewed as pro-mining but still entails multi-year review processes incorporating environmental impact assessments which can delay project advancement or limit near-term production upside. Supply chain dynamics around specialized equipment sourcing and workforce availability further constrain rapid capacity increases.

McEwen’s operational moat centers on leveraging its consolidated asset base including the Gold Bar complex along with tight integration between exploration drills targeting reserve replacements and mine planning teams to ensure continuous feedstock quality. Its holdings in McEwen Copper offer strategic leverage should copper prices sustain upward trajectories driven by decarbonization policies requiring copper-intensive supply chains.

Growth Catalysts: Asset Consolidation and Exploration Prospects

The primary growth driver identified in recent disclosures revolves around unlocking value from Golden Lake Exploration acquisition integrated into the Gold Bar Mine Complex ([S27]). This consolidation expands measurable mineral resources enabling potential scale efficiencies in blasting operations, waste rock handling logistics, and milling throughput improvements.

Exploration success at adjacent zones within Nevada remains pivotal; positive drill results may extend mine life or provide feedstock grade uplifts—two factors directly increasing unit profitability under prevailing ore grade economics ([S21], [S29]). Furthermore, planned feasibility studies linked to these assets will refine capital allocation strategies aligning mine design with prevailing metal price expectations.

Secondary drivers reside in McEwen Copper equity exposure; copper pricing stability or increases could materially enhance overall earnings given shared margins though this remains less controllable from McEwen Inc.’s direct operating standpoint ([S1]).

Operational discipline maintaining cost per ounce mined during low-price environments paired with selective capital deployment fosters a flexible financial model sustaining exploration without jeopardizing balance-sheet integrity.

Risks and Constraints: Commodity Cycles, Permitting, and Operational Challenges

Intrinsic risks pervade the mining sector spanning macroeconomic influences on metal prices—where cyclical downturns can compress margins significantly—and regulatory uncertainties around permitting approvals which may delay project execution timelines impacting cash flow predictability ([S2], [S1]).

Environmental compliance obligations pose continued monitoring needs; evolving standards require potentially costly retrofits or mitigations that can extend development caps on new mine phases—especially significant given Gold Bar’s ongoing expansion initiatives.

Operational execution risks include geological surprises altering grade assumptions mid-mine life or equipment downtime which constrain output volume targets essential for fixed-cost absorption efficiency.

The company also faces typical geopolitical sensitivities inherent when operating partially through equity interests outside North America that could expose it to currency exchange swings or policy shifts affecting mining incentives.

Collectively these constraints require vigilant management focus balancing risk mitigation versus opportunistic growth capex deployments aligned with market signals.

Key Metrics to Watch for Upcoming Quarters

Key performance indicators defining near-term progress include:

- Mineral reserve updates at Gold Bar mines anticipated from forthcoming technical reports underpinning mine plan revisions ([S21]).

- Production volumes relative to prior quarters reflecting integration efficacy post-Golden Lake deal implementation ([S2], [N1]).

- Sustained cost control metrics such as all-in sustaining costs per ounce mined amid inflationary pressures.

- Developments regarding permitting approvals influencing future expansion initiatives’ timelines.

- Movements in copper/gold spot prices impacting operational leverage indirectly through McEwen Copper stake valuation adjustments ([S1]).

- Capital expenditure pacing reflecting drilling intensity supporting resource extensions before major build-outs.

- Any refinancings or liquidity transactions affecting balance sheet flexibility particularly if metal price environments deteriorate unexpectedly.

Investor attention should focus on these quantitatively evidenced milestones as clear directional guides for operational momentum assessment leading into later-stage developments.

Brief Financial Profile: Liquidity, Leverage, and Capital Structure

As of March 31, 2026 quarter-end data show McEwen holding approximately $56.5 million in cash & equivalents paired against total debt near $126 million yielding net debt around $69.8 million resulting in a current ratio of about 1.14 ([F1], [S2]). This moderately leveraged stance supports ongoing exploration expenditures while maintaining sufficient liquidity buffers necessary given industry operating capital demands.

The capital structure reflects common pressures typical of mid-tier miners seeking balance between growth investments—including integration costs following recent acquisitions—and prudent leverage management to avoid overextension amid cyclic commodity environments. Cash conversion dynamics will continually depend on realized metal prices alongside disciplined capital allocations to preserve financial health while pursuing value accretive project developments.

This analysis objectively synthesizes available SEC filings alongside verified news sources without advocating investment actions or forecasting specific outcomes. Mining sector inherent risks require careful consideration alongside company-specific progress indicators detailed herein.

Financial position in context

As of 2026-03-31, companyfacts shows $57mm in cash and equivalents and $126mm of total debt [F1]. The same snapshot implies net debt of roughly $70mm, keeping balance-sheet context relevant but secondary to the operating story [F1]. Current assets of $110mm and current liabilities of $97mm imply a current ratio near 1.14x for 2026-03-31 [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments