Mynd.ai's Strategic Patent Acquisitions Contrast With Contracting Revenue and Regulatory Pressure

Mynd.ai confronts NYSE compliance risks amid declining revenue and a shift toward patent-driven growth strategies.

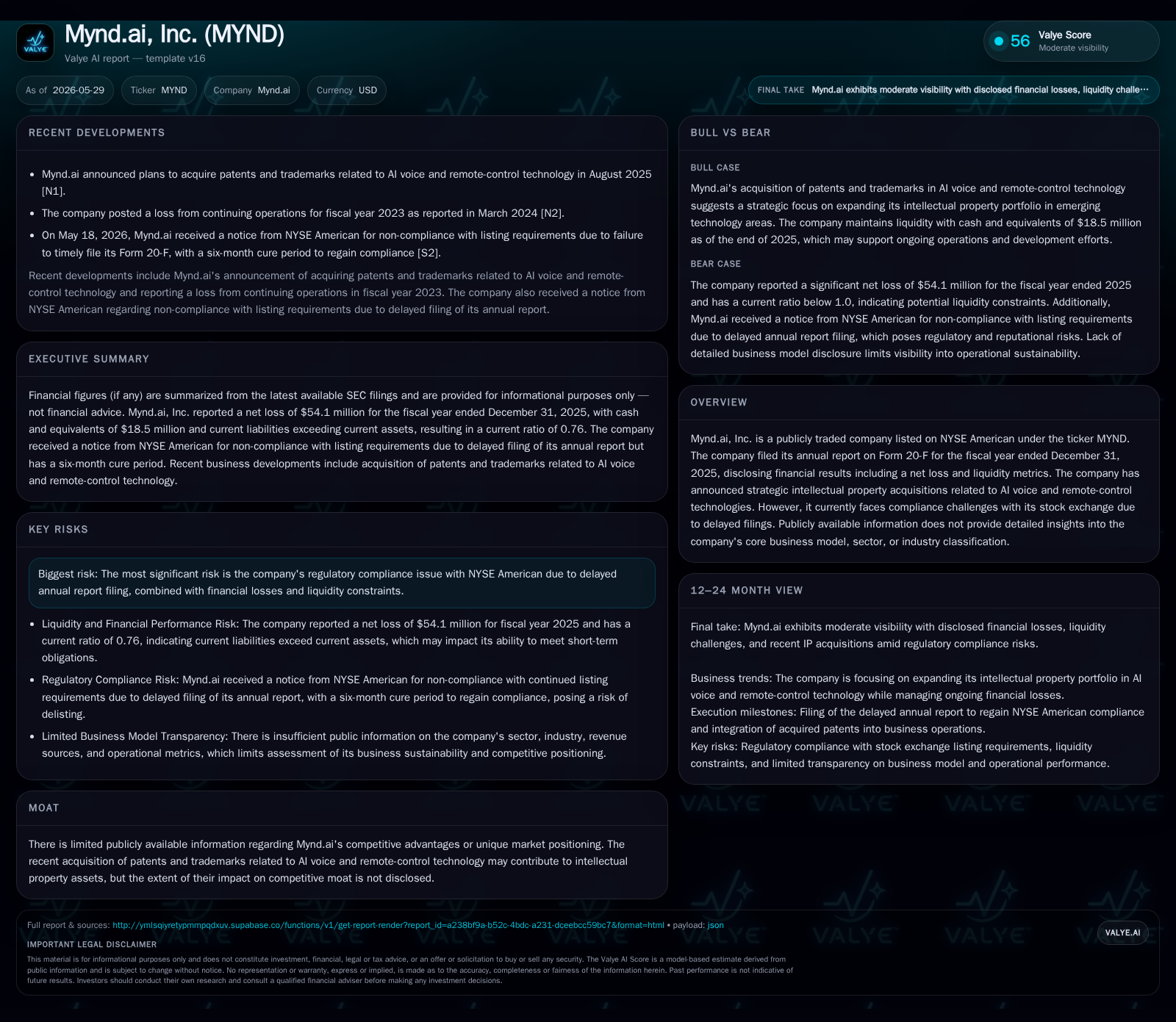

In its latest quarterly 6-K filing dated May 22, 2026, Mynd.ai disclosed receipt of a regulatory notice from NYSE American due to delayed filing of its annual Form 20-F, triggering a six-month cure period that heightens near-term listing risk [S2]. The company’s 2025 annual report reveals a sharp 37% revenue decline and substantial gross profit contraction, reflecting industry-wide budgetary pressure and customer uncertainty [S1]. Against this backdrop, Mynd.ai is pivoting strategically by acquiring intellectual property related to AI voice and remote-control technologies while downsizing internal R&D in favor of partner-led development [S1]. This combination of regulatory pressure, financial stress, and a transformation in product development frames a challenging path ahead.

Recent Operating Update: Compliance Notice and Timely Filing Delays

On May 18, 2026, Mynd.ai received an official notice from NYSE American Regulation citing non-compliance with continued listing standards due to failure to file its Annual Report on Form 20-F for the fiscal year ended December 31, 2025 within the required deadline [S2]. This triggered a six-month cure period running until November 2026 during which Mynd.ai must submit its overdue filing to regain compliance. The company publicly disclosed this delinquency promptly on May 22, highlighting ongoing challenges in maintaining regulatory timelines amid operational pressures. This marks a critical juncture as failure to cure could lead to delisting from the NYSE American exchange, amplifying investor concern and limiting access to capital markets.

Earlier disclosures in March noted Mynd.ai’s intent to file the report by April 30, per SEC allowances, but the actual submission was delayed through late May [S3]. The delay suggests potential internal resource constraints or procedural bottlenecks amidst broader organizational restructuring.

This regulatory overhang frames the company's immediate operational narrative and underscores urgency on compliance as foundational for any strategic moves or capital raising efforts.

Business Model Overview and Strategic Intellectual Property Expansion

Mynd.ai's core business model—as described in the May 29, 2026 annual report—involves offering technology products centered around AI-enhanced voice control and remote-control capabilities embedded within hardware and software solutions, although exact market segmentation remains undisclosed [S1]. Revenue generation fundamentally depends on sales volume within education technology channels across multiple regions; however, total revenue contracted steeply by approximately 37.2% year-over-year to $167.9 million in FY25 from $267.4 million in FY24 [S1].

Gross profit dropped proportionally more—by nearly 47%—to $35.3 million as fixed components within cost of goods sold such as employee-related expenses and depreciation constituted higher proportions of shrinking revenue base. This dynamic implies deteriorating unit economics since fixed costs cannot scale down immediately with volume reductions.

Operating expense management took center stage with general administrative costs falling by roughly $6.9 million due primarily to headcount reduction and leadership restructuring. Research & development expenditure halved from $25.3 million to $12.8 million, signaling a strategic pivot away from heavy internal innovation toward leveraging partner relationships for product development [S1]. Sales & marketing spend was trimmed modestly amid shrinking revenue.

Adding complexity is the acquisition of intellectual property assets related to AI voice recognition technologies and remote-control functions during the reporting period—intended presumably to bolster proprietary technology portfolios enabling differentiation and future monetization opportunities. While Mynd.ai provided limited disclosure on direct impacts, these strategic patent purchases suggest a longer-term orientation toward IP licensing or embedding advanced AI features into offerings that might improve competitive positioning once mature.

Competitive Context and Industry Positioning

Fixed-cost absorption risks are acute given the high base of employee-related COGS which prevent margin flexibility under volume contraction [S1]. Competitors with greater scale or diversified offerings may better withstand such downturns or sustain R&D investment internally rather than shifting externally as Mynd.ai is doing.

Customer retention may face pressure if pricing power erodes against cheaper alternatives or new entrants emphasizing ease-of-integration SaaS solutions over legacy hardware-centric models. The strategic move towards alliances appears aimed at mitigating these risks but also reflects resource constraints limiting stand-alone innovation capacity.

Key Growth Drivers: Strategic Partnerships and Product Development Shifts

In response to financial pressures and changing market dynamics, management restructured product development by significantly reducing internal R&D headcount while collaborating closely with key inventory suppliers and select external partners for software and SaaS platform enhancements [S1]. This partnership-led strategy potentially accelerates time-to-market at lower incremental cost but depends heavily on execution discipline, partner alignment, intellectual property integration quality, and effective IP monetization strategies.

The newly acquired patent portfolio focusing on AI voice recognition technology represents an asset base that could underpin new licensing deals or proprietary product features offering defensible differentiation over competitors lacking similar IP coverage.

Additionally, limited pockets of stability identified in European markets indicate focused geographic penetration efforts might contribute incremental growth beneath headline revenue declines.

Therefore, growth prospects hinge on successfully scaling these partnerships into commercially viable products while navigating competitive pressures and macro headwinds affecting customer buying behavior.

Risks and Constraints: Regulatory Compliance, Financial Challenges, and Market Uncertainty

Mynd.ai contends with multiple interdependent risk factors constraining growth:

- Regulatory Delisting Risk: Failure to file overdue Form 20-F timely places Mynd.ai at risk of NYSE American delisting after November 2026 cure deadline, impairing liquidity options[S2].

- Liquidity and Leverage Pressure: As of December 31, 2025, Mynd.ai held approximately $18.5 million in cash against $76.5 million total debt resulting in net debt around $57.97 million; current liabilities exceeded current assets leading to a challenged current ratio of approximately 0.76 indicating short-term liquidity stress [F1].

- Loss Intensification: Operating loss widened by more than $12 million YoY reaching -$50 million driven by steep revenue erosion coupled with fixed cost structure inefficiencies[S1].

- Demand Uncertainty: Industry-wide slowed IT/education technology budgets driven by macroeconomic caution depress new orders; U.S. market showed particularly sharp declines while only certain European locales fared relatively better[S1].

- Execution Risk on Partnerships: Shifting from internal R&D-heavy model to partnership-based innovation entails dependence risks including IP quality control issues, partner reliance vulnerabilities, plus potential dilution of proprietary know-how.

Collectively these factors elevate operational risk profile requiring close monitoring especially for compliance remediation progress along with consistent operational stabilization signals.

Near-Term Milestones and What to Watch

Critical catalysts in coming months include:

- Form 20-F Filing: Submission before November 2026 deadline remains paramount for preserving NYSE listing status; any further delays would exacerbate regulatory risks [S2][S3].

- Revenue Trend Stabilization: Signs of bottoming or growth resumption via improved bookings or renewals post-partnership transitions will be key demand markers [S1].

- Partnership Expansion Announcements: New collaborations enhancing software/SaaS portfolio breadth could validate management’s strategic shift toward ecosystem engagement.

- Cost Structure Adjustments: Further operational efficiencies improving cash flow metrics amid debt servicing demands should be assessed via subsequent quarterly disclosures.

- Regulator Communications: Any additional exchange correspondence regarding listing standards compliance will inform investor sentiment on regulatory risk management effectiveness.

These milestones frame the pathway for measuring tangible progress through financing relief opportunities combined with gradual recovery on product commercialization fronts.

Financial Profile Brief Contextualization

Fiscal year ended December 31, 2025 financials reveal acute earnings distress driven mainly by contracting revenues (-37%) compounded by largely fixed cost burdens resulting in operating losses enlarging by ~32% YoY ($50M loss) [S1][F1]. Liquidity remains tight with net debt approximating $58M against cash reserves near $18.5M yielding working capital deficiency (current ratio below unity) which constrains financial flexibility especially during delayed filings creating refinancing uncertainties [F1][S2]. Interest expense remained steady around $10M indicating consistent debt servicing requirements further stressing cash flows.

Overall financial indicators underscore the need for effective turnaround actions involving both operational stabilization through partnership innovation focus alongside stringent fiscal discipline coupled with prompt compliance remediation to maintain public listing benefits.

This analysis synthesizes disclosures from Mynd.ai's recent SEC filings up through May 29, 2026 without extrapolation beyond stated facts or speculative projections. Readers seeking further insight should monitor subsequent quarterly reports or exchange announcements for updated performance signals or regulatory milestones.

Financial position in context

As of 2025-12-31, companyfacts shows $18mm in cash and equivalents and $76mm of total debt [F1]. The same snapshot implies net debt of roughly $58mm, keeping balance-sheet context relevant but secondary to the operating story [F1]. Current assets of $84mm and current liabilities of $110mm imply a current ratio near 0.76x for 2025-12-31 [F1].

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments