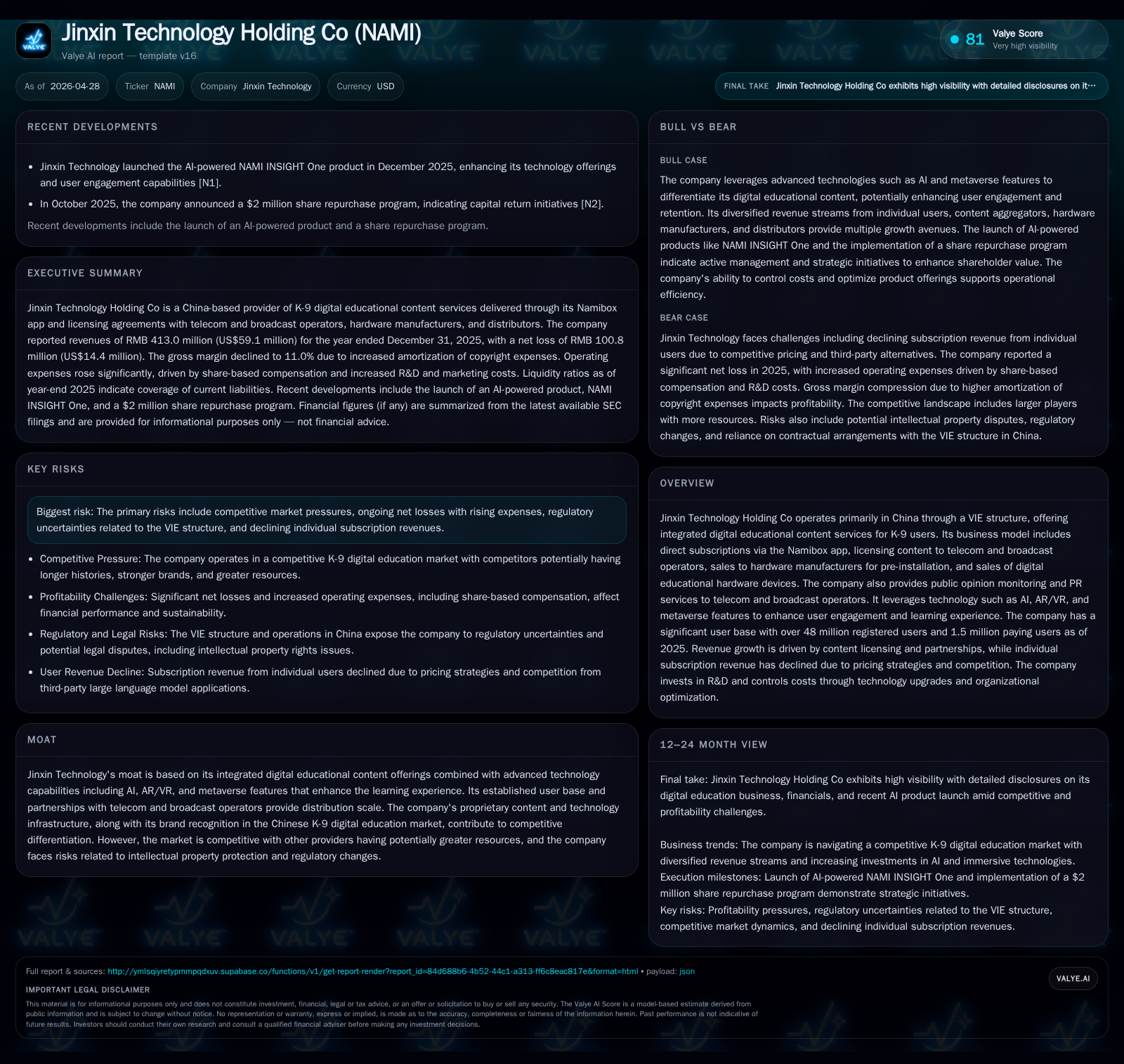

Jinxin Technology Strengthens CFO Role as Operating Loss Deepens Amid Content Investment

April 2026 financial leadership confirmation coincides with mounting operating losses driven by intensified investments in digital content and technology.

Jinxin Technology, a key player in China’s K-9 digital education sector, recently appointed Jun Jiang as its official CFO, signaling renewed focus on financial stewardship during a period of escalating losses. The company’s latest quarterly filing reveals growing expenses mainly from employee compensation and increased copyright amortization amidst declining individual subscription revenues. While content licensing and telecom partnerships fuel modest revenue growth, rising costs and pricing pressures weigh on margins. Jinxin leverages AI, AR/VR, and metaverse integrations to enhance its learning platform moat, but faces competitive and regulatory headwinds that complicate near-term profitability.

Recent Quarterly Operating Update: Leadership Change and Performance Snapshot

In its latest 6-K filing dated April 28, 2026, Jinxin Technology announced the formal appointment of Jun Jiang as its chief financial officer following his interim tenure alongside his director and COO roles [S2]. This management clarification is significant given the company’s operating performance deterioration highlighted in recent disclosures.

For the fiscal year ended December 31, 2025, Jinxin reported an operating loss of RMB104.3 million (approximately $14.9 million), contrasted with an operating income of RMB27.1 million just one year earlier [S4,F1]. The swing primarily reflects accelerated employee compensation costs—a strategic investment to bolster internal capabilities—and sharply higher amortization expenses rooted in expanded content copyright acquisitions. Additionally, research and development expenses rose nearly 12% year-over-year as the company focused efforts on new product innovation [S4,S5].

The revenue side showed modest growth (+1.6%) reaching $59.1 million driven largely by expanded content licensing partnerships with telecom and broadcast operators [S9,F1]. However, this was offset by a steep 20.6% decline in subscription revenue from individual users during aggressive promotional pricing strategies designed to retain customers while countering free offerings from large language model providers [S9]. Declining hardware sales due to intensified price competition further pressured revenues in other segments [S9].

This snapshot reflects Jinxin’s current operational tension: bolstered investment into digital educational content and proprietary technologies against the backdrop of near-term margin stress.

Business Model Ecosystem: Integrated Digital Content and Diverse Revenue Streams

Jinxin operates primarily through a Variable Interest Entity (VIE) structure within China’s K-9 digital education market [S1]. Its business model is multifaceted:

- Direct user subscriptions via the Namibox app provide personalized access to digital educational materials.

- Content licensing to telecom/broadcast operators constitutes a major revenue stream; these partners distribute Jinxin's proprietary materials broadly across platforms.

- Sales to hardware manufacturers for pre-installation of Jinxin’s learning software expand usage reach but currently face margin pressure due to raw material cost inflation.

- Direct sales of digital educational hardware products contribute additional revenue.

- Complementary public opinion monitoring and PR services address telecom partner needs related to content engagement management [S1].

As of end-2025, Jinxin reported over 48 million registered users with roughly 1.5 million paying subscribers—a modest paying-user base relative to total registrations indicative of challenging conversion dynamics under current pricing tactics [F1,S1,S9]. The company’s flexible monetization approach balances direct subscriptions with more scalable institutional licensing but must carefully manage the trade-offs between volume growth and yield.

Competitive Positioning in China’s K-9 Digital Education Market

Jinxin competes in a deeply fragmented yet highly competitive market marked by several sizable players with longer operating histories and greater brand recognition [S12]. Key competitive factors include:

- Product quality and diversity: Jinxin emphasizes rich interactive content differentiated through technology-driven enhancements.

- User base scale: A large registered user pool leverages network effects but attracts competition for paying customer acquisition.

- Technology infrastructure: Proprietary AI-powered analytics combined with AR/VR capabilities support personalized learning journeys.

- Brand reputation: Although meaningful within certain regional clusters, it faces pressures against better-financed incumbents.

- Regulatory agility: Adaptation to shifting educational policies and restrictions distinguishes sustainable competitors.

These technology layers constitute differentiated user engagement mechanisms underpinning Jinxin's value proposition beyond standard digital textbooks or video lectures [S1,S4,F1]. Nevertheless, these benefits come at notable cost—research & development spending increased nearly 12% in 2025—heightening the operating expense burden at a time when gross margins have compressed dramatically due to copyright amortization rises [S4,S14]. Balancing ongoing innovation investment with cost containment presents a delicate operational challenge.

Growth Catalysts and Constraints: User Engagement, Licensing, and Pricing Pressures

Jinxin aims to stimulate growth through several levers:

- Enhanced technology-driven product upgrades targeting improved retention among existing users seeking more engaging learning tools.

- Expanding content licensing agreements, particularly with telecom operators who tap into broad subscriber bases allowing revenue scaling without directly onboarding individual consumers.

However, constraints emerge from:

- Competitive pricing pressures forcing promotional discounts that dilute average revenue per paying user (ARPPU).

- Declining demand in hardware-related revenues aggravated by raw material inflation undermining previously solid price advantages.

- Rising amortization charges linked directly to amplified copyright acquisitions increasing fixed costs thus adding operational leverage risk [S9,S5,F1].

Overall demand appears structurally supported by China's significant urban K-9 student demographic but cyclical factors tied to school term seasonality impose variability on subscription revenues emphasizing the need for consistent product appeal [S23].

Regulatory and Structural Risks from VIE and Market Environment

Operating via a VIE structure places inherent legal uncertainty on Jinxin’s control over underlying assets amid China's tightening overseas listing regulations [S12,S16,S21]. Government scrutiny on foreign investment entities further complicates governance stamina.

China’s Ministry of Education mandates strict filings for educational apps targeting minors along with substantial usage restrictions including time limits for underage users—all impacting user engagement dynamics especially on mobile platforms [S12,S23]. Intellectual property disputes remain an ongoing concern given extensive industry litigation around digital education copyrights—litigations which are costly both financially and reputationally if not effectively managed [S12,S26]. Tightened anti-monopoly statutes also require vigilant compliance around platform behavior preventing exclusionary practices or abuse of dominant positions further complicating competitive strategy execution.

Financial Profile: Funding the Expansion Amid Rising Costs

As of December 31, 2025, Jinxin held cash & cash equivalents of approximately $9.2 million juxtaposed against total debt near $2.15 million yielding net cash surplus around $7 million [F1]. Current assets exceed liabilities with a current ratio near 1.53 supporting operational liquidity cushions [F1].

Despite this healthy balance sheet positioning, profitability challenges magnify as net loss widened sharply to $13.49 million reflecting greater amortization expenses allied with climbing payrolls largely stemming from share-based compensation plans granted during the year [S4,S5,F1,S13]. Net cash used in operating activities turned negative indicating growing funding requirements aligned with heavy investment phases although prior years had positive operating cash flow contributions [S7].

Collectively this points toward a corporate trajectory reliant on continued capital infusion or improved operational leverage through enhanced monetization before sustainable profit normalization is achievable.

Key Milestones and What Investors Should Monitor Next

To assess progression amid strategic uncertainties during the next quarters investors should track:

- Conversion rates from registered users into paying subscribers signaling effectiveness of pricing/promotional initiatives.

- Trends in content licensing revenue expansion relative to rising fixed copyright amortizations informing margin outlooks.

- Product launch success particularly incorporating AI/AR/metaverse features that can materially uplift user engagement metrics.

- Regulatory developments impacting educational app operating licenses or cross-border VIE model viability shaping long-term structural risk profile.

- Cost control effectiveness focusing on personnel expenses and amortization management critical for reversing margin erosion trends.

- Further senior leadership appointments especially within finance or product divisions which may indicate shifts in strategic execution priority levels.

- Quarterly earnings releases for signs of reduced loss acceleration or early profit pockets illustrating operational stabilization progress.

Monitoring these operational KPIs will elucidate whether recent investments forge durable competitive advantages or exacerbate financial strain amidst intensifying market headwinds.

This analysis is based solely on publicly available regulatory filings as of April 28, 2026, without any recommendation or investment advice. It aims to provide an informed assessment grounded in disclosed company data.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments