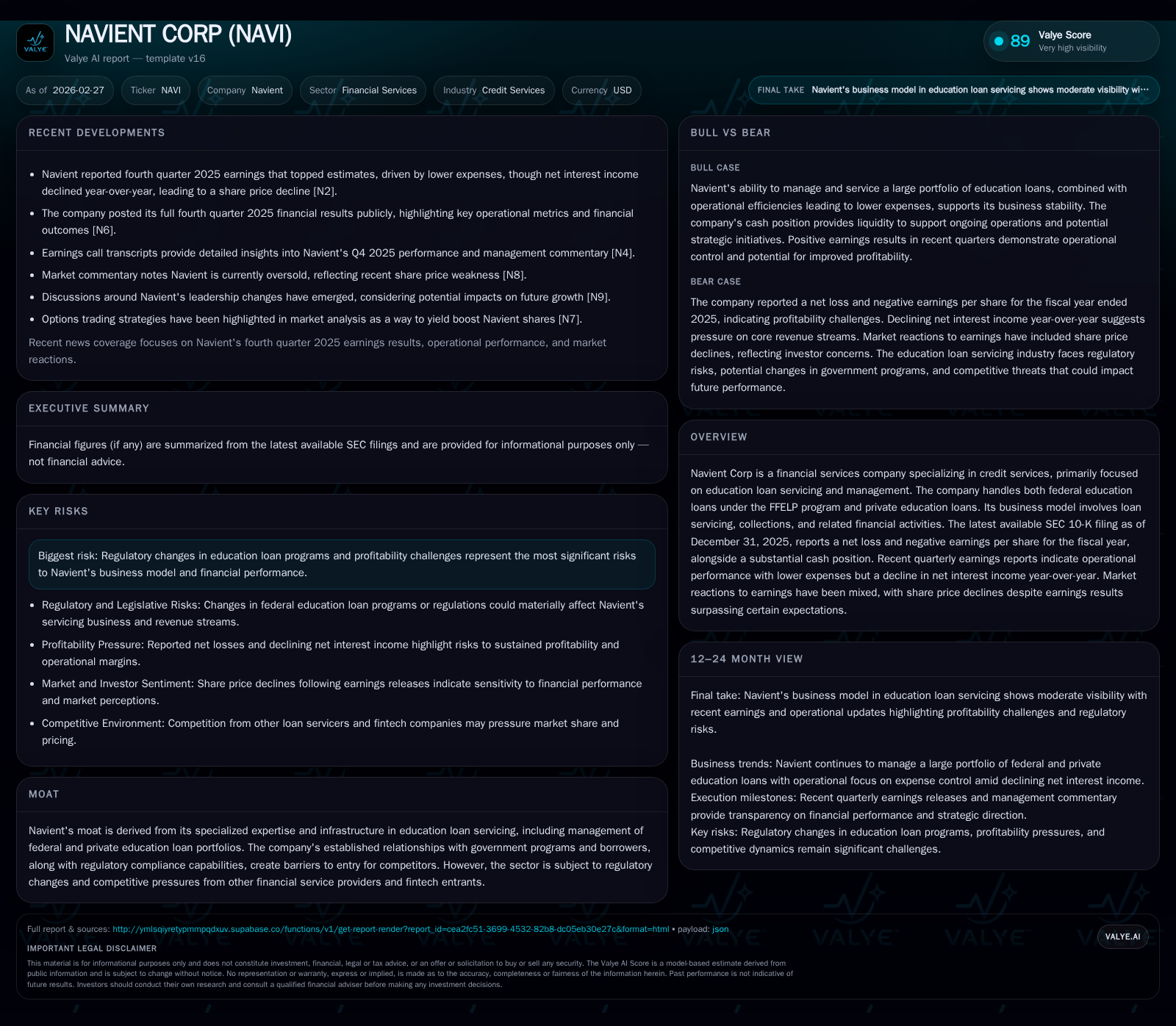

Navient Corp's Earnings Paradox: Lower Expenses but Declining Net Interest Income

Navient’s recent financial results show a tension between operational cost reductions and compressing net interest margins in a complex education loan servicing market.

Navient Corp reported a net loss for fiscal year 2025 despite surpassing quarterly earnings expectations driven by significant expense cuts. The company grapples with declining net interest income amid structural shifts in the education lending market, notably the ongoing wind-down of FFELP loans and regulatory challenges. Capital allocation remains disciplined with dividends paid and share repurchases reduced, reflecting a cautious strategy given earnings volatility. Monitoring net interest margin trends and regulatory developments will be critical to assessing Navient’s recovery trajectory.

Historical Financial Trajectory and Operating Drivers

Navient Corp’s financial landscape has experienced marked shifts over the past four fiscal years. After robust profitability with net incomes of $645 million in FY2022 and $228 million in FY2023, earnings declined but remained positive at $131 million in FY2024 before turning negative by -$80 million in FY2025 [F1]. This drastic earnings inversion (-161.1% YoY change) accompanies only a moderate drop in operating cash flow (-3.9% YoY to $441 million), illustrating resilience in the firm’s cash-generative loan portfolios despite compressed net interest margins.

This divergence between earnings and cash flow mainly stems from factors such as increased default remediation costs and tighter net interest spreads within Navient's credit services, particularly servicing federally guaranteed FFELP loans alongside private education loans. The FFELP program segment naturally declines over time following its discontinuation after July 2010, imposing inherent top-line pressures [S1]. Meanwhile, steady cash flow supports sustaining operations and capital returns.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Net YoY |

|---|---|---|---|

| 2025 | -80 | 441 | -161.1% |

| 2024 | 131 | 459 | -42.5% |

| 2023 | 228 | 676 | -64.7% |

| 2022 | 645 | 305 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | ROE% |

|---|---|---|---|

| 2025 | 63 | 111 | -3.3 |

| 2024 | 70 | 179 | |

| 2023 | 78 | 310 | |

| 2022 | 91 | 400 | 21.7 |

Source: SEC companyfacts cache [F1].

Table: Navient’s financial performance depicts shrinking earnings with relatively stable operating cash flows, while ROE turns negative FY2025.

Decoding the Recent Earnings Upset: Expense Cuts versus Income Decline

In the fourth quarter of FY2025, Navient delivered earnings that surpassed analyst estimates primarily due to effective expense management [N3][N6]. The company implemented a variable, outsourced servicing model — notably contracting MOHELA — that lowered fixed operational expenses associated with loan servicing functions [S4]. This modular expense structure enabled the firm to reduce servicing costs while maintaining regulatory compliance.

However, this improvement was counterbalanced by a decline in net interest income (NII) year-over-year as loan prepayment rates fell below prior assumptions and prevailing rates compressed margins across both the federal loan portfolio winding down and private refinancings [S1][N4]. With FFELP loans securitized extensively under non-recourse structures (~87%), yield compression on these assets directly impacts net interest margin structures critical for revenue [S13]. Moreover, servicing fee income shifts due to evolving customer delinquency behavior and non-accrual loans further pressure revenue streams.

Stock price declines following Q4 results reflect investor concerns about near-term NII sustainability despite operational gains [N3]. This paradox highlights structural challenges tied to macro-financial conditions intersecting with Navient's specialized credit servicing model.

Evolving Business Model: From Loan Servicing to Portfolio Optimization

Navient has streamlined its business focus substantially since early-2024 by divesting non-core healthcare and government processing units finalized by February 2025 [S4]. This strategic pruning aligns with a clear emphasis on educational loan servicing — Federal Family Education Loan Program (FFELP) loans legacy portfolio management alongside augmented private education lending origination through its Earnest platform [S9][S13].

The firm leverages deep expertise in federal student loan program regulations and infrastructure — encapsulated within its adherence to the 'Three Lines Model' governance framework — reinforcing regulatory compliance as a core competitive moat [S6]. This specialization poses high barriers for new entrants attempting FFELP loan servicing due to stringent oversight requirements.

Private education loans feature enhanced underwriting criteria aiming for higher credit quality amidst increasing origination volumes (+77% growth in private loans originated in FY2025 vs prior year), suggesting Navient is positioning for organic franchise expansion beyond federal contraction [S9]. The complexity of managing securitized asset-backed pools necessitates skilled capital and risk management capabilities now central to Navient’s operational model.

Capital Allocation Dynamics and Shareholder Returns

Despite profitability headwinds, Navient has maintained a disciplined capital return approach balancing shareholder distributions against liquidity preservation [S4]. In FY2025, the company paid $63 million in dividends, slightly down from $70 million in FY2024, evidencing ongoing commitment albeit at a moderated scale relative to prior years [F1]. Share repurchases similarly contracted materially to $111 million from $179 million year-over-year, consistent with Board authorization for $100 million remaining buyback capacity at year-end.

Navient's equity-to-asset ratio remains stable at approximately 4.9%, with an Adjusted Tangible Equity Ratio of 9.1%, underpinning its capital adequacy [S4]. This prudent leverage posture supports access to capital markets while navigating profitability volatility.

ROE for FY2025 stands at an approximate negative -3.3% given losses amid strong equity levels — underscoring near-term return challenges but also reflecting investments into portfolio quality enhancement and operational flexibility.

Regulatory Landscape and Its Impacts on Profitability

Operating within federally guaranteed educational loan programs exposes Navient to substantial regulatory risk fluctuations that can materially impact revenue streams tied to servicing contracts [S2]. The discontinuation of the FFELP program constrains long-term growth potential as the portfolio amortizes down over several years.

Moreover, the firm employs rigorous compliance governance including the industry-standard 'Three Lines Model,' ensuring strong internal controls but also imposing operational complexity that elevates costs [S6]. Emerging fintech entrants apply digital innovations disrupting traditional loan servicing economics potentially pressuring fees.

Any significant policy shifts regarding borrower relief initiatives or changes to guaranty agency contracts could alter loss remediation dynamics or reduce recoverable amounts on defaulted loans—directly hitting Navient's credit services revenue base.

Forward-Looking Signals: What to Watch in Navient’s Next Phases

Investors should monitor several key metrics as signals of Navient’s ability to regain profitability momentum. Chiefly among these are:

- Trends in net interest income amid rate environment changes and stabilizing or accelerating private loan origination volumes,

- Sustainability of lower operational expenses under the variable outsourced model,

- Evolution of credit quality indicators within both federal legacy portfolios and newer private loans,

- Regulatory developments impacting FFELP contractual terms or passage of new borrower assistance legislations,

- Capital return policy adjustments reflecting changes in free cash flow generation.

Recent partial market oversold conditions per technical analysis imply some investor skepticism embedded already; however, execution on portfolio optimization alongside regulatory navigation will ultimately dictate longer-term outcomes [N12][N10].

This report is prepared solely for informational purposes based on publicly available data as of February 27, 2026. It contains no investment advice or recommendations. Readers should conduct their own due diligence before making any financial decisions related to Navient Corp or its sector context.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments