Norwegian Cruise Line's Financial Rebound Meets Capital Structure Challenges

Strong profitability recovery contrasts with intense liquidity and debt pressures amidst heavy capex spending.

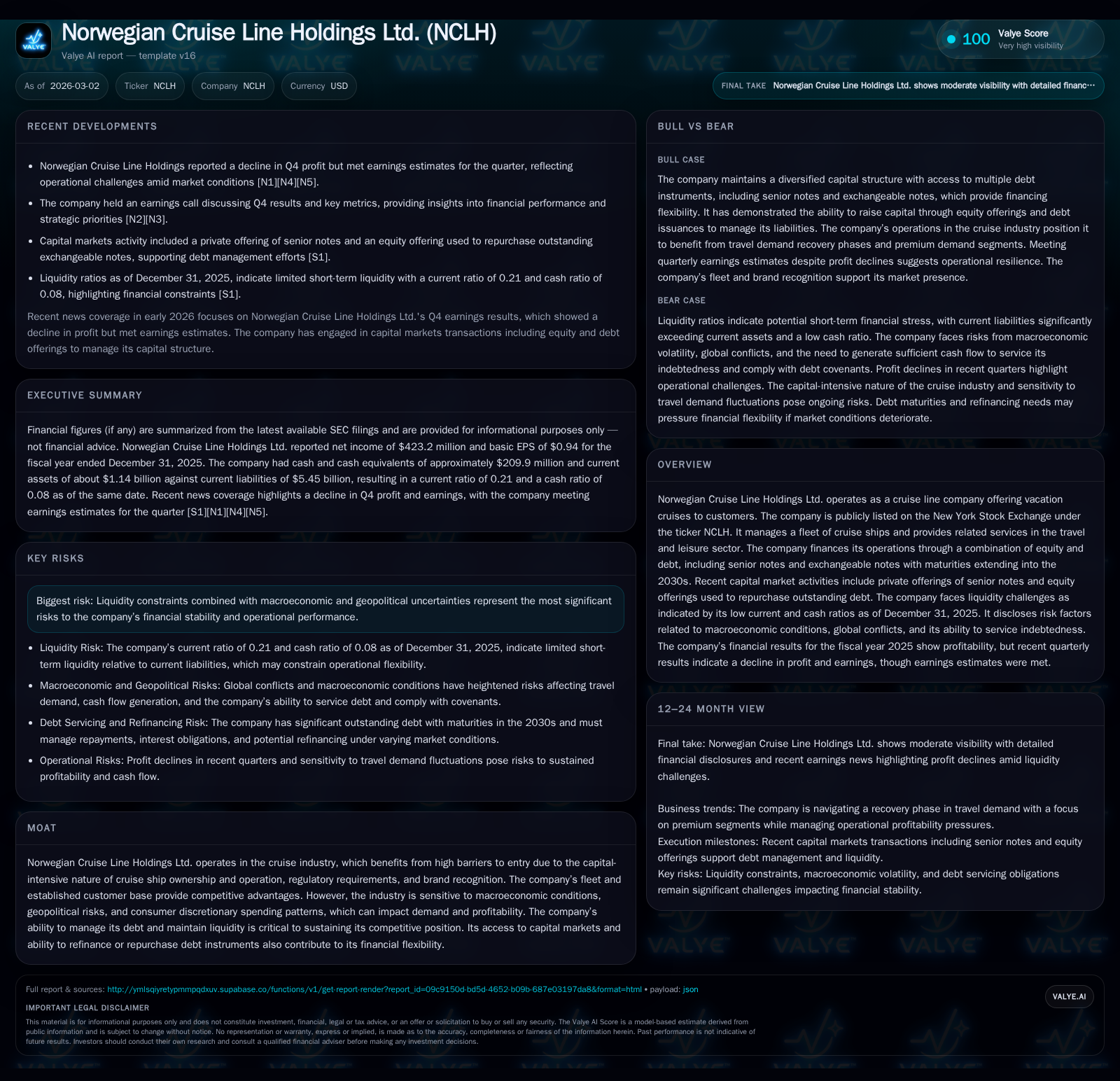

Norwegian Cruise Line Holdings Ltd. has rebounded from deep losses in 2022 to deliver robust operating income and profits by 2025, supported by revenue growth driven by fleet expansion and strong passenger demand. However, its liquidity position remains constrained with a low current ratio of approximately 0.21, reflecting significant short-term liabilities against limited current assets. A surge in capital expenditures, up 169% year-over-year in fiscal 2025, underscores the company's commitment to modernizing its fleet but weighs heavily on free cash flow generation. NCLH’s complex debt profile includes multiple senior notes extending into the early 2030s, with embedded covenants and refinancing risks that require careful monitoring. Despite a solid return on equity of about 19.2% in 2025, the negative free cash flow highlights operational cash demands amid growth investments and debt management challenges.

From Recovery to Profitability: NCLH’s Recent Historical Performance

Norwegian Cruise Line Holdings Ltd. traces a striking financial recovery arc over the recent years. After recording an operating loss north of $1.55 billion in fiscal year (FY) 2022—a period marked by pandemic repercussions—NCLH swung to an operating profit of approximately $930 million in FY2023, then further expanded its operating income to about $1.47 billion in FY2024 before reaching a peak over $1.56 billion by FY2025 [F1]. This trajectory reflects not only a significant restoration of demand but also operational leverage coming into play.

Revenue similarly exhibits long-term growth momentum with an over 11% compounded annual growth rate (CAGR) since FY2014, climbing from roughly $789 million to north of $12 billion as cruise operations normalized and market share was regained. However, net income figures demonstrate more fluctuation; after posting a hefty loss of roughly $2.27 billion in FY2022, net earnings rebounded strongly the following years to highs above $910 million in FY2024 before moderating to around $423 million in FY2025 [F1]. This moderation signals margin pressures or elevated costs despite overall top-line strength.

Crucially, operating cash flows reveal underlying stability across this volatile earnings profile — hovering consistently around the $2 billion mark annually through FY2025 [F1]. This steadiness attests to effective working capital management and core business resilience even when net income swings substantially.

Historical performance (annual)

| FY | Net ($bn) | CFO ($bn) | OpInc ($mm) | Capex ($bn) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 0.4 | 2.1 | 1561 | 3.3 | -53.5% |

| 2024 | 0.9 | 2.0 | 1466 | 1.2 | +447.8% |

| 2023 | 0.2 | 2.0 | 931 | 2.8 | +107.3% |

| 2022 | -2.3 | 0.2 | -1552 | 1.8 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -1170 | 19.2 |

| 2024 | 839 | 63.9 |

| 2023 | -745 | 55.2 |

| 2022 | -1574 | -3309.3 |

Source: SEC companyfacts cache [F1].

Table presents selected historical financial performance for Norwegian Cruise Line Holdings Ltd., highlighting key trends.

Fleet Expansion and Passenger Demand: Key Drivers Behind Revenue Growth

Norwegian Cruise Line operates within a capital-intensive domain where fleet size and quality fundamentally dictate revenue capacity and customer experience differentiation [S5]. The company’s business model centers on high-value vacation cruises serviced through a diversified fleet portfolio incorporating new builds and regular refurbishments.

Passenger demand recovered strongly post-pandemic driven by pent-up travel appetite and effective pricing strategies for various cruise itineraries discussed during earnings calls [N2][N3]. Seat capacity utilization rates have climbed along with ticket yields reflecting successful repositioning efforts.

However, underpinning these gains is a substantial funding burden necessitated by continual capital deployment toward ships’ renewal programs — a dynamic fundamental to maintaining competitive positioning given industry peers’ similar upgrade cycles.

Liquidity Crunch Amidst High Leverage: NCLH's Capital Structure in Focus

Despite operational improvements, Norwegian Cruise Line faces material liquidity constraints illustrated starkly by its current ratio around a precarious 0.21 as of December 31, 2025 (current assets approx. $1.14 billion vs current liabilities exceeding $5.45 billion) [F1]. Such compression spells elevated risk for near-term working capital sufficiency.

The firm’s debt profile is intricate with senior notes spanning maturities into the early-to-mid-2030s issued via private placements [S6][S8][S9][S13].[N1] NCLH has proactively engaged capital markets with private senior note offerings coupled with equity raises to fund tender offers repurchasing nearer-term notes — moves that are beneficial for easing refinancing pressure but result in extended debt duration and incrementally higher leverage metrics.

Indenture covenants attached to these instruments impose typical operational limitations including restrictions on additional liens, sale-leaseback transactions, asset disposals, alongside stringent change-of-control repurchase clauses accompanied by make-whole premiums [S9][S11][S28]. Such constraints require vigilant covenant compliance monitoring particularly under episodic macro shocks which could impair cash flow availability.

The Surge in Capital Expenditures: Modernizing Fleet for Competitive Edge

Capital expenditure requirements surged by approximately +169% YoY in FY2025 totaling over $3.25 billion compared with roughly $1.21 billion spent the prior year [F1][S5]. This spike predominantly aligns with ongoing new ship construction activities and comprehensive refurbishment projects designed to elevate guest experience standards while incorporating sustainability features increasingly demanded by regulators and consumers alike.

While necessary for long-run competitiveness given cruise vessel asset life cycles typically span decades with intermittent upgrades, such heightened capex intensity disproportionately balloons near-term cash outflows pushing free cash flow into significantly negative territory [F1]. Managing this trade-off between growth investment and liquidity preservation remains critical.

Debt Profile Nuances: Senior Notes, Covenants, and Refinancing Options

The issuance of multiple tranches of senior unsecured notes—including $1.2B of exchangeable notes due 2030 at low coupons (~0.75%), along with sizable offerings featuring higher coupons around ~5.875%-6.25% due through the early-2030s—forms the backbone of NCLH’s capital structure remediation strategy executed mid-2025 [S9][S13][S17][N2].

These notes contain sector-standard indenture provisions such as make-whole call options permitting redemption before stated maturities upon payment of premiums calibrated to lost yield compensation for investors; change-of-control triggering repurchase rights at par plus interest; as well as limits on collateral pledging preserving unsecured status critical for ongoing issuance flexibility.

Furthermore, the company utilized proceeds from these offerings alongside equity raises (per registered direct offerings priced near ~$24.53/share) to prepay/refinance portions of older senior secured obligations approaching near-term maturity dates reducing rollover risk but increasing overall gross leverage lengths [S17][N2]. Equity-linked securities also provide conversion optionality which may moderate principal amounts outstanding if exercised.

Analyzing Cash Flows and Returns: ROE Strength vs. Free Cash Flow Deficit

Though Norwegian Cruise achieved an estimated return on equity close to approximately 19.2% for FY2025—reflecting profitable operations against shareholder equity around $2.21 billion—the firm's free cash flow was negative by nearly -$1.17 billion primarily due to capex outlays exceeding operating cash flow generation for the year [F1].

This dichotomy suggests that while profitability metrics are sound indicating efficient use of equity capital relative to reported net income levels, cash flow dynamics expose strain linked with heavy reinvestment needs amid liquidity tightness.

High leverage likely inflates ROE measures inside accounting frameworks without fully capturing underlying cash demands—a common complexity faced by asset-heavy leisure travel operators balancing investment cycles against protracted recovery pathways post-COVID disruption.

Outlook and Forward Indicators: What to Watch in 2026 for NCLH Investors

Absent explicit forward guidance beyond standard risk disclosures regarding macroeconomic turbulence—including inflationary pressures accelerating costs—and geopolitical uncertainties weighing on consumer discretionary spending patterns—key focus areas throughout calendar year 2026 will be covenant compliance amid tight liquidity ratios and monitoring actual cruise booking trends against assumptions baked into recent earnings releases [N1][N7][S7][S10].

Given multiple large debt maturities now pushed into the early next decade after recent refinancing steps, maintaining access to capital markets or alternative funding sources remains essential while sustaining fleet modernization momentum without exacerbating free cash flow deficits.

Moreover, industry cyclicality tied closely to global travel sentiment will remain a pivotal variable affecting pricing power and voyage occupancy metrics—both central determinants shaping revenue trajectories for operators like Norwegian Cruise Line.

Capital Allocation Strategy: Dividends, Buybacks, and Debt Reduction Plans

Recent filings confirm that Norwegian Cruise has eschewed dividend payments or share repurchases amidst ongoing deleveraging efforts focused on preserving hard liquidity buffers necessary for operational resilience amid heavy capex demands and debt servicing obligations [F1][S17][N3].

The company’s September-2025 transactions involving combined equity raises alongside exchangeable notes allowed partial repurchases targeting older higher-coupon exchangeable senior notes due mid-decade—a tactical approach aimed at smoothing upcoming redemption cliffs while managing interest expense loadings [S17].

Going forward balancing shareholder returns versus liquidity retention will be critical especially if macroeconomic headwinds intensify or if fleet renewal requires further incremental investment beyond currently planned levels.

This analysis synthesizes publicly available SEC filings and recent news reports without providing investment recommendations or price forecasts. It does not substitute professional financial advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments