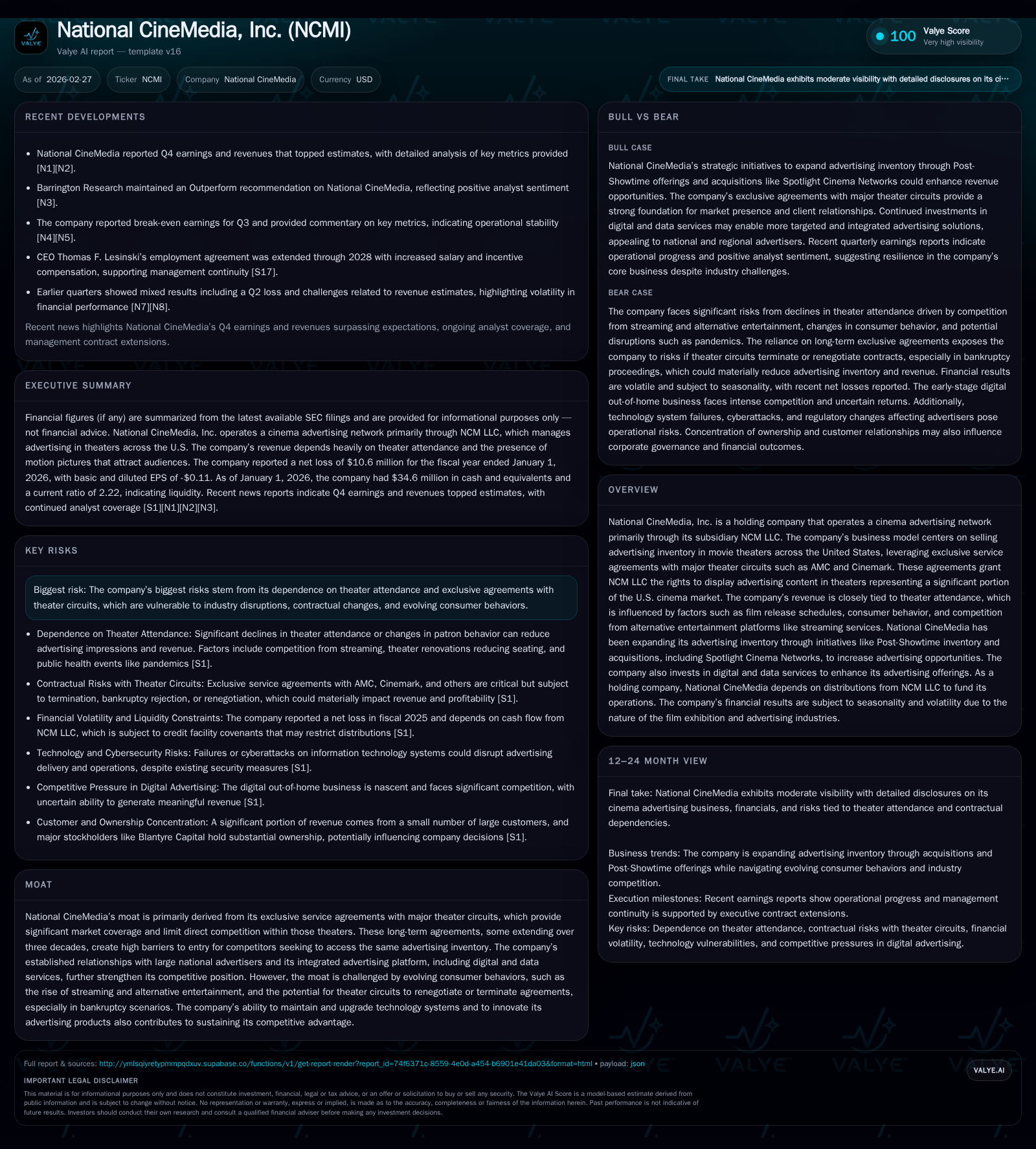

National CineMedia’s Revenue Collapse Reflects Challenges in Cinema Advertising and Consumer Behavior Shifts

Exclusive theater advertising agreements underpin National CineMedia’s position amid protracted declines in attendance and evolving digital competition.

National CineMedia, Inc. (NCMI) operates a dominant cinema advertising network secured by long-term exclusive agreements with key theater circuits AMC and Cinemark. Despite its entrenched position, NCMI has faced severe revenue declines since 2019, driven by falling theater attendance exacerbated by streaming alternatives and changing consumer habits. The company reported a sharp drop from $147 million in 2019 to $15.7 million in 2020, with ongoing losses reflected in operating income through 2025. While recent acquisitions like Spotlight Cinema Networks aim to expand inventory and diversify offerings, growth prospects hinge heavily on cinema foot traffic recovery and technological innovation amid competitive pressures. Capital allocation shows continued dividends and buybacks despite losses, while debt covenants and liquidity management remain areas to monitor closely.

Company Overview

National CineMedia, Inc. (NCMI) functions primarily as a holding company operating through its subsidiary NCM LLC, which holds exclusive rights to offer cinema advertising services across a large portion of the U.S. movie theater market [S1]. The company’s business model depends heavily on strategic service agreements (ESAs) with key exhibitors such as AMC Entertainment Holdings and Cinemark Holdings. These agreements grant NCM LLC exclusivity for displaying pre-show advertisements and other promotional content within participating theaters' auditoriums.

The exclusivity agreements serve as the foundation of NCMI's moat: they erect high barriers to entry by controlling access to premium cinema advertising inventory spread over thousands of screens nationwide [S1]. The company also operates integrated platforms that fuse traditional screen advertisements with digital and data-driven solutions aimed at national advertisers.

Historical Performance and Revenue Decline

NCMI’s historical financials reveal a sharp inflection beginning around FY2020 driven largely by pandemic-related disruptions alongside systemic challenges impacting cinema traffic [F1]. Key revenue figures illustrate this shift:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -11 | 8 | -14 | 6 | +52.5% |

| 2024 | -22 | 60 | -19 | 6 | -103.2% |

| 2023 | 705 | -27 | 3 | +2557.1% | |

| 2022 | -29 | 7 | 3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 11 | 22 | 3 |

| 2024 | 0 | 13 | 55 |

| 2023 | 1 | ||

| 2022 | 10 |

Source: SEC companyfacts cache [F1].

Note: Revenue after FY2020 is not reported due to accounting changes associated with bankruptcy proceedings and consolidation adjustments [S11].

The precipitous fall from roughly $147 million in revenue during FY2019 to just $15.7 million in FY2020 underscores the immediate impact of COVID-19 driven theater closures [F1]. This decline also reflects longer-term secular pressures such as increased consumer preference for streaming services and accelerated contraction of traditional film release windows bypassing theaters entirely [S1; S8]. The industry-wide deterioration suppressed operating margins heavily; operating losses persisted into FY2025 despite some recovery attempts.

Profitability and Cash Flow Dynamics

Operating income has remained negative over the last several fiscal years, bottoming at -$27 million in FY2023 before moderating somewhat to -$13.9 million in FY2025 [F1]. Net income shows fluctuations influenced by non-recurring items related to restructuring post-bankruptcy filings.

Operating cash flow declined sharply from pre-pandemic levels but stabilized around $8–60 million range depending on the year considered [F1]. Capital expenditures have remained controlled at approximately $5–6 million annually—largely focused on technology system upgrades consistent with cloud migration efforts described by management [S17; S18]. Estimated free cash flow remains positive around $2.8 million for FY2025 after capex deductions.

Expansion Initiatives and Future Growth Prospects

In November 2025, NCMI acquired Spotlight Cinema Networks aiming to broaden its advertising inventory through additional preshowtime slots across theaters nationwide [S17]. This deal is positioned strategically as part of an effort to counterbalance declining impressions due to lower attendance by unlocking incremental advertising opportunities.

Growth catalysts include:

- Leveraging existing ESAs with large exhibitors offering access to millions of patrons weekly.

- Expansion into digital out-of-home advertising products integrating data-driven consumer insights collected via proprietary apps and theater visits.

- Developing AI-driven targeted ad placements while navigating regulatory scrutiny concerning consumer privacy [S21; S15].

Conversely, growth limitations are significant:

- Persistently low or uneven moviegoer turnout threatens inventory monetization.

- Shifts toward streaming content reduce theatrical relevance as studios experiment with shortened or eliminated exclusivity release windows [S1; S29].

- Potential renegotiation or terminations of ESAs especially if affiliated theater chains pursue internalizing media sales or restructuring financially [S24].

- Competitive pressures from established digital advertising platforms siphoning marketing dollars away from conventional cinema formats [S8].

Industry trends reflect heightened competition among media placements along with an accelerating push towards programmatic ad buying—a field where NCMI aims but struggles technologically given legacy infrastructure constraints [S18].

Capital Structure, Liquidity & Capital Allocation

NCM LLC refinanced its revolving credit agreement effective January 24, 2025 establishing a senior secured revolving credit facility of $45 million maturing January 24, 2028, with approximately $12 million outstanding as of January 1, 2026 [S4; S6; S13]. The company exhibits reasonable liquidity evidenced by a current ratio above 2x at fiscal year-end January 2026 [F1], suggesting capacity to meet near-term obligations without stress.

Despite ongoing operational losses, the parent company continued returning capital through dividends totaling approximately $11.4 million in fiscal year ending January 2026 accompanied by share repurchases worth around $22 million over the same period [F1; S23]. This capital allocation approach indicates confidence from management or significant stockholders regarding intrinsic value despite industry headwinds.

Equity levels stood near $375 million at fiscal year-end January 2026 following reconsolidation accounting after emergence from Chapter 11 proceedings mid-2023 [F1; S11]. Return on equity remains negative given net losses sustained (-2.8% approx ROE based on latest net loss vs equity).

Risks Impacting Business Sustainability

Key risks emphasize dependence on third-party exhibitors maintaining robust attendance levels directly influencing available ad impressions [S29]:

- Prolonged declines due to shifting consumer preferences away from cinemas.

- Regulatory changes impacting data collection practices critical for targeted advertising capabilities.

- Cybersecurity threats potentially disrupting ad delivery systems affecting advertiser satisfaction and revenues [S19; S22].

- Contractual risks arising from bankruptcy or restructuring events involving network affiliates threatening ESA enforceability or exclusivity rights as witnessed with Regal’s departure post-bankruptcy settlement [S24].

- Competitive encroachments internally via concessions cross-promotions and externally via online video platforms intensifying pricing pressure leading to margin erosion [S25; S8].

Strategic Outlook: What to Watch Going Forward

Absent explicit consensus guidance disclosed recently, critical milestones will revolve around:

- Stabilization or improvement of aggregate attendance reflecting audience normalization post-COVID disruptions.

- Successful integration and monetization of Spotlight Cinema Networks inventory contributing meaningful incremental revenues beyond legacy screens.

- Progression towards scalable digital out-of-home product offerings capturing increasing shares of advertiser budgets transitioning online.

- Maintenance of ESAs amidst possible renegotiations prompted by theater chain economic conditions or changing strategic priorities.

- Enhancement of technological capabilities enabling real-time programmatic ad insertions aligned with media buying trends.

- Regulatory compliance advances ensuring continued access to essential consumer data underpinning targeted ad effectiveness.

Monitoring quarterly earnings releases for comparable ad impressions sold metrics alongside utilization rates across newly acquired inventory may provide early indicators of network health recovery dynamics [N1; N2]. Financial discipline around operating expenses balanced against capex on technology upgrades will further clarify sustainability horizons for profitability restoration.

Conclusion

National CineMedia operates within a uniquely constrained yet potentially lucrative niche dominated by exclusive contracts granting high entry barriers but exposed squarely to volatile external forces reshaping entertainment consumption behaviors globally. The dramatic revenue contraction post-pandemic reveals inherent vulnerabilities tied closely to physical attendance trends challenging historic growth trajectories.

While asset-light holdings approach supported by contractual protections allows some cushion against direct operational burdens, sustaining innovation technologically and operationally remains essential alongside vigilant risk mitigation—particularly regarding contract integrity amidst theater circuit financial strains and intensifying competitive landscapes.

Investors monitoring NCMI should pay close attention to macro trends influencing moviegoing patterns alongside internally generated operational data showcasing progress against strategic expansion initiatives such as Spotlight acquisition deployment and digital product maturation.

This analysis does not constitute investment advice or recommendations but provides an independent assessment based strictly on publicly available information.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments