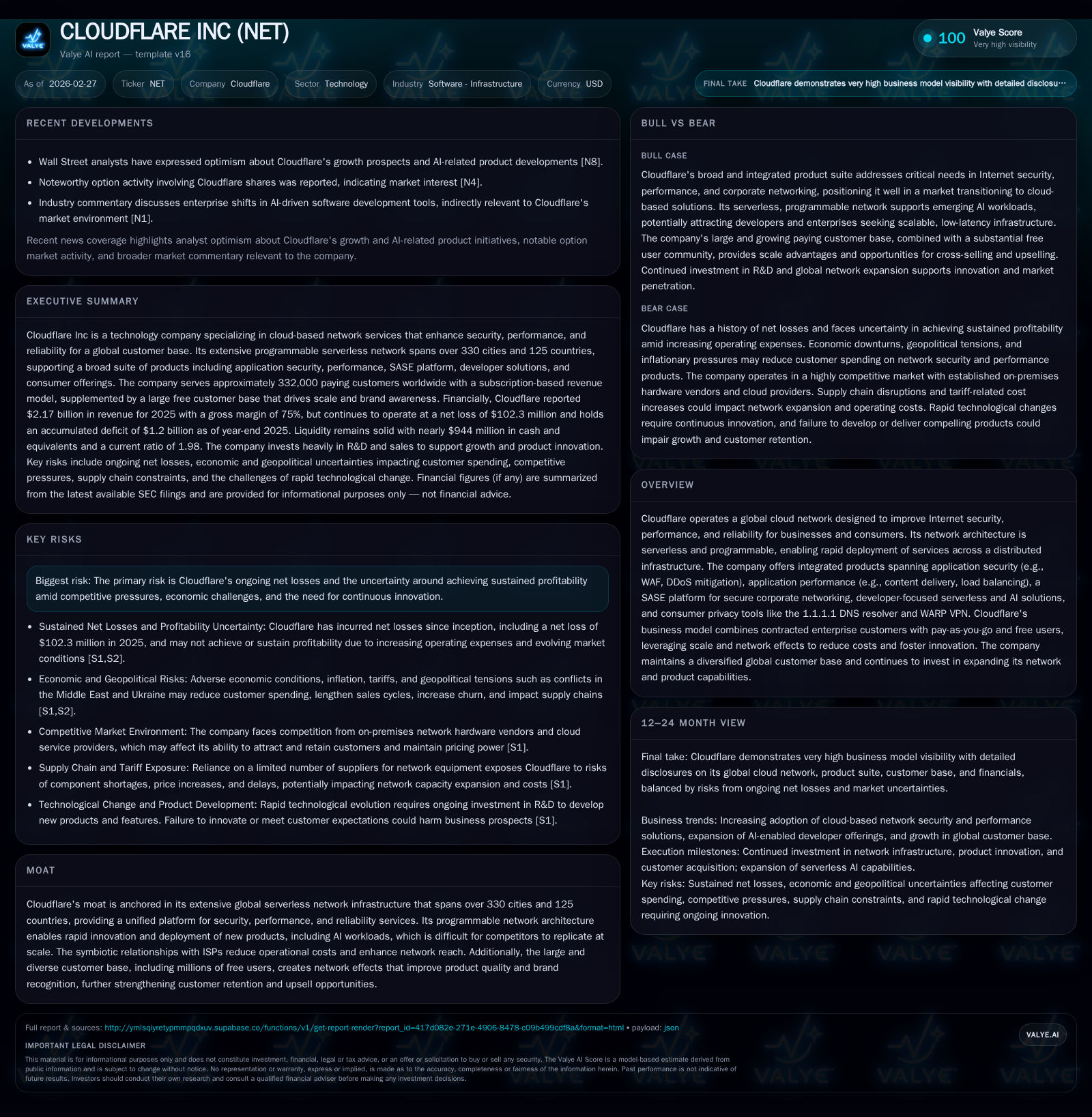

Cloudflare's Growth Balances Rapid Network Expansion With Persistent Profitability Challenges

Cloudflare leverages its extensive global serverless network to drive robust revenue growth while grappling with ongoing net losses amid heavy investment and competitive pressures.

Cloudflare, a leader in cloud-based network security and performance infrastructure, has demonstrated significant revenue acceleration supported by a vast global network spanning over 330 cities and more than 125 countries. Its innovative serverless architecture and diversified business model targeting both enterprise contracted and pay-as-you-go customers underpin this growth. However, despite strong operating cash flows and free cash flow generation, the company remains unprofitable with a sizable accumulated deficit driven by sustained investments in research, development, and network expansion. Key risks include market competition, regulatory complexities especially around AI and data privacy, and macroeconomic headwinds that could impede sustained profitability. Future growth hinges on expanding large enterprise customer penetration and leveraging AI capabilities built into its platform.

Company Overview

Cloudflare operates an expansive global cloud network aimed at improving Internet security, performance, and reliability across enterprises of all sizes. Central to its proposition is a programmable "serverless" architecture that allows it to deliver unified network services globally without the need for traditional on-premises hardware boxes. This network infrastructure spans more than 330 cities across over 125 countries with interconnection spanning over 13,000 networks including ISPs, cloud providers, and enterprises. The architecture's flexibility supports rapid deployment of services such as web application firewall (WAF), DDoS mitigation, Zero Trust SASE security platform offerings, content delivery networks (CDN), load balancing, developer-focused serverless compute products (Cloudflare Workers), and AI workload hosting.

Cloudflare’s customer base mixes contracted Enterprise clients with multi-year agreements alongside a substantially larger pay-as-you-go subscriber base ranging from developers to mid-sized businesses. The inclusion of millions of free users enhances global traffic visibility which aids threat detection and product refinement while enabling scale economies via partnerships with ISPs that reduce bandwidth costs.

Historical Performance

From the financial data through year-end 2025 [F1], Cloudflare has exhibited remarkable top-line growth:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -102 | 603 | -207 | 316 | -29.8% |

| 2024 | -79 | 380 | -155 | 185 | +57.2% |

| 2023 | -184 | 254 | -185 | 114 | +4.9% |

| 2022 | -193 | 124 | -201 | 144 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 0 | 287 | -7.0 |

| 2024 | 0 | 195 | -7.5 |

| 2023 | 34000 | 140 | -24.1 |

| 2022 | 3000 | -20 | -31.0 |

Source: SEC companyfacts cache [F1].

Revenue growth accelerated from about +29% in FY24 to roughly +30% in FY25. Despite increasing revenue scale, operating losses widened to over $200 million in FY25 from ~$155 million in FY24 as investments intensified primarily in R&D related to expanding product capability including AI features as well as geographic infrastructure buildout [F1], [S1]. Net losses show improvement versus prior years but remain substantial.

Operating cash flow improved materially by nearly 60% year-over-year driven by improving collections efficiency and scale benefits internally, delivering strong positive cash generation even while net income remains negative—an important liquidity factor given ongoing capex expenditures upward of $315 million reflecting capacity expansion as well as integration of AI-optimized servers with GPUs [F1], [S17].

Business Model & Product Offering

Cloudflare's serverless model underpins not only its scalability but also its ability to rapidly innovate across a broad spectrum of products that bundle security, performance optimization (CDN, load balancing), and reliability under one umbrella—referred to as their "Connectivity Cloud" platform [S4], [S14]. This approach contrasts with legacy models relying on managing discrete network appliances or stitching together multiple point security/cloud providers.

Contracted enterprise customers account for high-value predictable revenue streams via multi-year agreements often inclusive of both fixed subscriptions plus variable usage components or "pool of funds" commitments allowing flexible consumption without strict minimum feature adoption monthly or quarterly obligations [S4]. Additionally, pay-as-you-go customers buy online access plans ranging from Pro/Business tiers mostly billed per domain or API plus modular add-ons for advanced needs; these plans enable a low friction entry point fueling large paying user growth especially among developers deploying serverless applications using Cloudflare Workers' usage metered model [S4], [S7].

Competitive Position & Moat

The moat centers on ownership of the world's most expansive programmable global edge network deployed into over 330 cities in more than a hundred countries combined with deep integrations with ISPs allowing lower bandwidth costs due to co-location discounts—a significant cost advantage rarely matched by peers who may rely more heavily on leased cloud capacity or localized points-of-presence without the same breadth or programmability capabilities that enable tailored AI workload deployment closer to end users [S4], [S10], [S14].

While competing against entrenched on-premises hardware vendors (e.g., traditional firewalls), specialized point solution providers (e.g., DDoS protection firms), and major cloud hyperscalers offering fragmented networking/security add-ons (AWS Shield/WAF, Azure Front Door), Cloudflare emphasizes integrated service delivery combining security/performance/reliability layers under one control plane accessible via APIs—all deployed globally without requiring costly hardware installs or single-cloud lock-in risks for customers seeking multi-cloud strategies [S10], [S12].

This platform is further differentiated by its commitment not to mine or sell customer data aligning closely with customer trust needs while building new AI-oriented developer solutions that could significantly expand downstream TAM beyond traditional CDN/security markets as applications incorporate generative AI workloads hosted at edge locations [S14].

Geographic & Customer Base Diversification

International revenue comprised approximately half of total revenues by the end of FY25 demonstrating successful geographic expansion especially across Europe (28%), Asia-Pacific (15%), Middle East/Africa regions—all continuing consistent proportions since prior years—which reduces dependency on US market fluctuations or regulatory shifts domestically while capturing fast-growing digital economies abroad [S6].

Paying customers grew briskly from ~190K in FY23 to over 330K by year-end FY25 (+75%), while those contributing more than $100K annually increased similarly from ~2,750 to around 4,300 indicating growing enterprise wallet penetration—critical for long-term ARPU expansion given enterprise customers' propensity for consolidating networking/security stacks onto fewer cloud platforms providing cross-product synergies across the Cloudflare ecosystem [S6], [S19].

Profitability & Cash Flow Profile

Despite robust growth at the top line fueled by product breadth expansion and market penetration initiatives including marketing tied to flagship consumer tools like the free DNS resolver (1.1.1.1) and WARP VPN which serve as both brand ambassadors and traffic sources enhancing ISP partner economics; Cloudflare reported negative operating margins nearing -10% in FY25 after adjusted positive non-GAAP margins reflecting stock comp add-backs however still contending with challenging path toward GAAP profitability amid heavy investments in scaling infrastructure and talent acquisition globally—the company explicitly cautions such expenses are expected to rise further before economies of scale can be fully realized profitably [F1], [S5], [S17].

Operating cash flows considerably outpace net income losses showing proficient operational leverage efficiency benefiting working capital management despite intensified capex spending necessary for building out new server capacities especially GPUs for AI workloads productivity gains; free cash flow reached $260 million roughly representing a healthy ~12% margin on revenues offering runway for continued capex-fueled growth absent external financing near term though capital returns via buybacks remain minimal/nonexistent signaling prioritization towards reinvestment over shareholder distributions currently [F1].

Return on equity is still negative approximating -7%, reflecting net loss persistence relative to equity base bolstered by recent capital raises expanding shareholder funding available for spend on R&D/network expansion rather than dividends or share repurchase programs at present time alongside accumulated deficit exceeding $1.2 billion underscoring Cloudflare’s current stage outlook focused on scale vs immediate profit extraction strategy typical among high-growth SaaS/infrastructure companies balancing innovation cycles versus commercialization timing nuances inherent in broad technology platform plays today [F1], [S18].

Risks & Regulatory Challenges

Key risk factors include the history of net losses without assured path to sustained profitability especially facing intensifying competition from entrenched incumbents with deeper pockets or newer entrants leveraging AI differentiations able to rapidly evolve go-to-market approaches potentially pressuring pricing/margins further alongside economic cyclicality influencing corporate IT spend patterns globally impacting sales velocity particularly at enterprise levels where lengthened sales cycles have been observed recently due partially to macroeconomic uncertainties such as tariff escalation fears between US-China affecting supply chain components pricing for server hardware used extensively by Cloudflare’s network footprint expansion efforts notably commodity servers augmented now increasingly with GPU nodes sensitive to semiconductor sector dynamics [S18], [S15], [S16].

Regulatory compliance costs tied specifically to evolving data privacy regimes worldwide plus emerging legislation targeting artificial intelligence software development/deployment such as EU’s AI Act implemented progressively through early-mid 2026 exacerbate complexity necessitating substantial internal controls evolution increasing legal/operational overhead incurred whilst ensuring Cloudflare products meet new standards on transparency/accountability which if not properly maintained could lead to enforcement actions or reputational damage impairing customer retention/brand goodwill particularly critical given large scale user community spanning free consumers to enterprises requiring trust continuity alongside intellectual property litigation risks arising typical within fast-evolving tech ecosystems engaged intensively in cryptographic software development portions powering core secure edge functionalities central also referenced within Cloudflare’s risk disclosures illustrating multifactor operational environment requiring vigilant legal/risk management focus ([S18], [S20]-[S23]).

Outlook & What To Watch Next

Wall Street anticipates upcoming earnings reports expected shortly will provide clarity around revenue growth sustainability amid competitive pressures as well as any hints toward narrowing losses or operating margin inflections following heavy investment periods noted over last years—a critical milestone as investors gauge whether recent influxes into AI workloads-driven developer platforms yield near-term monetization acceleration or will require extended lead-time before profitability levers materialize substantially given long sales cycles cited within large Enterprise contract renewals postulated predominantly between one-to-three year terms incorporating variable usage fees creating lumpiness percentile effect quarter-to-quarter episodic revenue recognition trends warranting careful scrutiny ([N2]).

Additionally monitoring dollar-based net retention rates will be telling since they reflect ability not only to retain but upsell existing clients consolidating further their networking/security spend onto Cloudflare’s unified platform—these metrics often foreshadow sustainable organic expansion beyond pure new logos acquisition fueling next stages of healthy margin progression underpinned by economies of scale enhancing gross margins previously stable around mid-70%s historically but vulnerable short term due to amortized cost layer increases from onboarding diverse international cohorts faster.

Capital allocation decisions remain critical albeit presently Cloudflare prioritizes reinvestment evidenced by zero share repurchase activity through recent years indicating focus squarely aligned toward supporting accelerated infrastructure rollout plans especially adding storage-enabled nodes plus GPU-capable servers specifically purposed for AI inference acceleration positioning itself competitively against hyperscale public cloud providers attempting similar edge compute offerings ([F1]).

Remaining competitive edge resides not only within technical merits but also strategic ISP partnerships crucial for favorable bandwidth/carrier access economics which could potentially face renegotiation risk depending on geopolitical shifts or changing telecom regulations particularly relating cross-border data flows intertwined deeply into Cloudflare’s operational fabric manifesting real-world sensitivity impacting unit economics should key interconnection agreements become less favorable ([S21]).

Summary

In sum, Cloudflare stands at an intersection of strong secular tailwinds powering demand for integrated secure cloud networking platforms fueled additionally by emerging AI workloads opportunity while concurrently navigating persistent profitability challenges typical for infrastructural SaaS innovators growing quickly yet investing heavily ahead of profits realization horizons. The company benefits from a uniquely extensive global programmable edge network coupled with diversified customer monetization approaches yet must remain vigilant managing regulatory compliance expenses alongside competitive threats primarily posed by established giants plus agile cloud-native startups increasingly leveraging artificial intelligence tools themselves. Financially sound liquidity position provides flexibility yet underscores need for sustained execution excellence translating innovation into scalable commercially profitable engagements gradually improving margin profiles going forward. Stakeholders watching upcoming earnings releases will seek confirmation regarding revenue acceleration stability alongside narrowing loss trajectory—a fundamental step toward validating maturity of current business investment phase amid evolving technology industry transformations.

Disclaimer: This company analysis is based solely on publicly filed financials ([F1],[S#]) and verified news sources ([N#]) without personal opinions or investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments