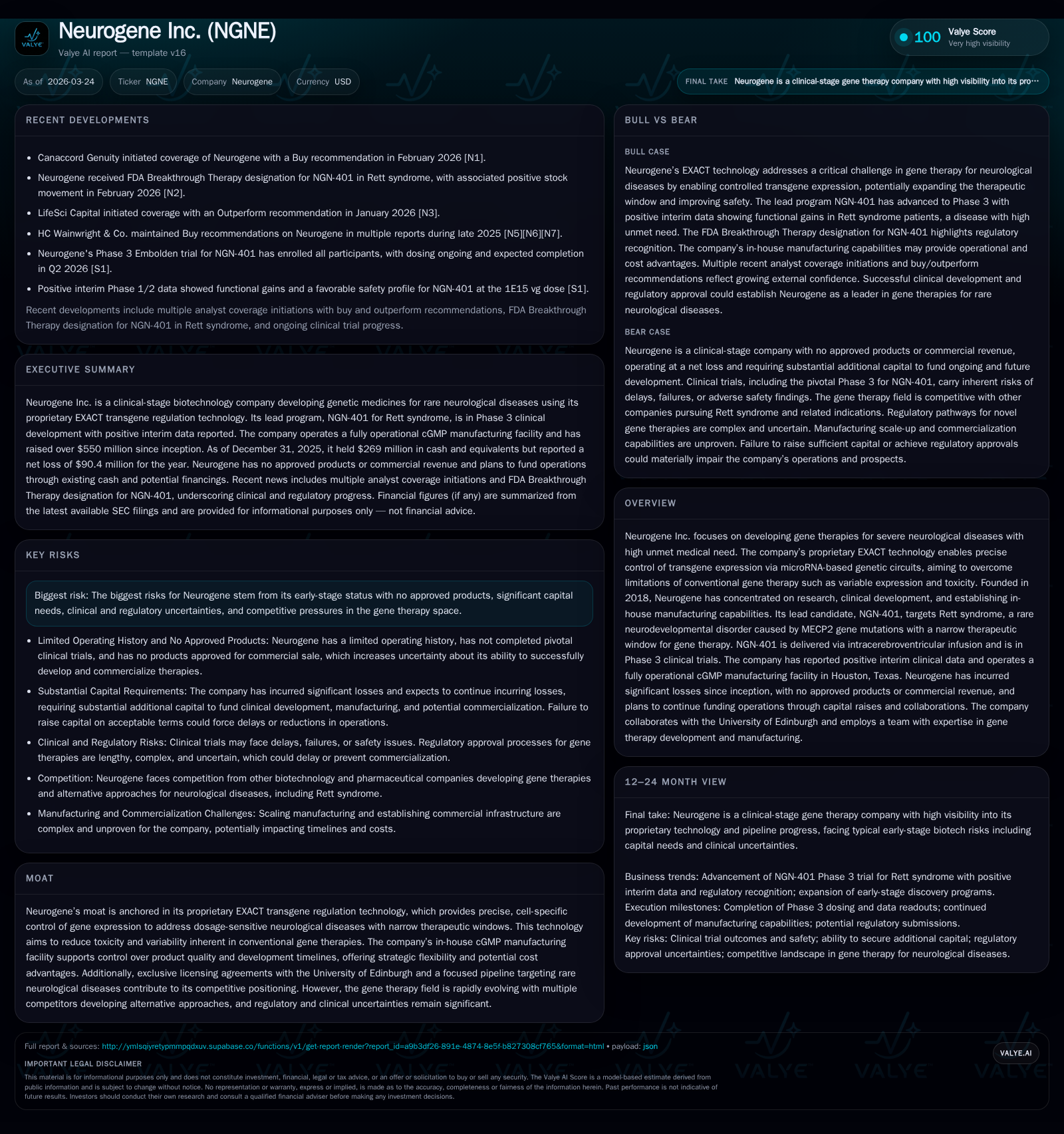

Neurogene's EXACT Technology and Clinical Pipeline Fuel Next-Gen Neurological Gene Therapies

Neurogene leverages proprietary microRNA-based gene regulation and integrated manufacturing to address rare neurological disorders with high precision and controlled expression.

Founded in 2018, Neurogene Inc. has concentrated its efforts on developing gene therapies using its patented EXACT platform, which employs microRNA genetic circuits to finely tune transgene expression—an innovation essential for dosage-sensitive neurological diseases like Rett syndrome. The company’s lead candidate NGN-401 is currently in Phase 3 registrational trials with encouraging interim clinical data, supported by an in-house cGMP manufacturing facility that enhances control over quality and timelines. Despite sustained operating losses driven by clinical advancement and R&D investment, Neurogene maintains a strong liquidity position but faces typical early-stage biotech risks including capital demands, regulatory uncertainties, and competitive pressures.

Foundations of Growth: Historical Financials and R&D Investment

Since its inception in 2018, Neurogene has primarily directed its resources to research and development activities aimed at advancing its gene therapy pipeline. The fiscal years 2022 through 2025 illustrate a trajectory marked by increasing investments aligned with its clinical programs' progress. Operating income steadily declined from a loss of $59.1 million in FY2022 to $103.3 million in FY2025, representing a compounded depletion as the company ramps up expensive late-stage clinical development activities [F1]. Net income follows a similar trend, deepening to a $90.4 million deficit by the end of 2025.

Operating cash flow reflects significant burn increasing from -$45.6 million in FY2022 to almost -$77.2 million in FY2025, consistent with investment in clinical trials and infrastructure buildout [F1]. Capital expenditures remain modest but show a late uptick to $1.18 million in FY2025, signaling incremental spending likely associated with manufacturing facility enhancements or scale-up [F1]. Equity expanded sharply especially from FY2022 to FY2023 — nearly doubling — due to capital raises (notably a $200 million private placement closed in late 2024) providing critical funding for ongoing operations [S19]. This robust equity base cushioned the balance sheet leading to a solid current ratio near 16.6x at the close of 2025 driven by $272 million current assets against roughly $16 million current liabilities [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -90 | -77 | -103 | 1183000 | -20.2% |

| 2024 | -75 | -71 | -83 | 808000 | -650.3% |

| 2023 | 14 | -51 | -56 | 321000 | +123.7% |

| 2022 | -58 | -46 | -59 | 1110000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -78 | -34.1 |

| 2024 | -71 | -24.2 |

| 2023 | -52 | 7.3 |

| 2022 | -47 | -61.0 |

Source: SEC companyfacts cache [F1].

Note: Yield calculations are approximate based on reported yearly net income to equity.

The widening losses year over year correspond with advances through clinical milestones such as IND clearance (January 2023) and initiation/enrollment of registrational Phase 3 trials for NGN-401, illustrating typical capital intensity for biotechnology companies at this stage [S1][S15].

EXACT Platform: Transforming Gene Therapy for Dosage-Sensitive Neurological Disorders

The centerpiece of Neurogene's differentiation resides in its proprietary EXACT technology (Expression Attenuation via Construct Tuning), which employs microRNA-based genetic circuits to finely modulate transgene expression within precise brain regions implicated in neurological disorders [S1]. Unlike conventional gene therapies characterized by variable transgene uptake leading to uncontrolled expression levels and potentially toxic outcomes — especially problematic when treating dosage-sensitive CNS diseases — EXACT implements engineered miRNA sensors that attenuate transgene output post-transcriptionally.

This approach achieves “transgene uptake control” by leveraging intrinsic cellular miRNA signatures to selectively suppress off-target expression while maintaining therapeutic levels in target neurons or glial subtypes (cell specificity). Such "microRNA genetic circuits" enable dosage titration within narrow therapeutic windows crucial for monogenic neurodevelopmental conditions where over- or under-expression can have detrimental effects [S1].

EXACT's innovative transgene expression attenuation mitigates risks of toxicity common in traditional AAV-based therapies that lack such feedback regulatory mechanisms, thus potentially enabling safer long-term treatment paradigms for devastating disorders like Rett syndrome.

NGN-401 for Rett Syndrome: Registrational Trial Status and Interim Clinical Outcomes

Neurogene’s lead candidate NGN-401 utilizes the EXACT platform delivered through adeno-associated virus (AAV) vectors via a one-time intracerebroventricular (ICV) injection — chosen strategically for optimal biodistribution across critical brain regions affected by MECP2 mutations causing Rett syndrome [S1]. The ICV route addresses challenges related to blood-brain barrier penetration and ensures effective delivery directly into the cerebrospinal fluid pathways.

The ongoing single-arm, open-label Phase 3 Embolden trial enrolls twenty female patients aged three years and older, representing the potential FDA-approved label population aiming for broad indication coverage from one pivotal study [S1][N2]. Over half the participants have been dosed already with completion of dosing anticipated by Q2 2026 [S1][N2]. Prior Phase 1/2 data involving ten patients at the therapeutic dose level demonstrated positive interim results—with all pediatric participants exhibiting functional improvements measured by developmental milestone gains across domains including motor skills, communication, and ambulation [S1]. These milestones were durable without reported regression through last follow-ups.

Further statistical highlights include four out of five patients meeting primary endpoint responder definitions at one year post-treatment alongside favorable safety profiles supported by ten participant datasets inclusive of varied age groups [S1]. The FDA granted Breakthrough Therapy designation reflecting recognition of NGN-401’s promising benefit-risk profile within this underserved patient population [N2]. This designation typically facilitates priority review pathways and increased regulatory engagement.

Manufacturing Edge: The Strategic Role of In-House cGMP Production

Strategically integral to Neurogene’s business model is its fully operational current good manufacturing practices (cGMP) facility located in Houston, Texas – responsible for producing clinical-grade NGN-401 material used across both Phase 1/2 studies and ongoing Phase 3 trials [S1]. This vertical integration provides multiple advantages uncommon among early-stage gene therapy developers who often rely heavily on third-party contract manufacturing organizations (CMOs).

Control over product quality ensures consistent drug substance integrity vital given EXACT’s complex genetic circuit design requiring precise vector construct fidelity; it also enables tighter oversight throughout development timelines minimizing delays linked to external dependencies common in the sector . Furthermore, maintaining dedicated capacity supports scalability prospects facilitating seamless transition into commercial manufacturing post-regulatory approval without major tech-transfer bottlenecks — a recognized historical challenge in gene therapy commercialization landscapes.

This approach potentially reduces supply chain risk while balancing cost efficiencies absent when outsourcing solely to external manufacturers prone to capacity constraints or variable quality issues—a notable consideration given the stringent cGMP requirements governing biologics production [S15].

Evaluating Forward Catalysts: Trial Milestones, Regulatory Breakthroughs, and Commercial Potential

Looking ahead, critical milestones shaping Neurogene’s near-term outlook revolve around full dosing completion for Embolden expected mid-2026 followed by pivotal efficacy data readouts aligned with twelve-month endpoint assessments [N2][S1]. Subsequent regulatory filings for NGN-401 will be benchmark events given current FDA Breakthrough Therapy designation status enhancing dialogue opportunities with authorities and possibly expediting review timelines.

Commercial potential hinges on demonstrating clear functional benefits corroborated by durable safety supporting broad label claims covering wider pediatric populations—a strategic advantage simplifying market access compared to fragmented indication targeting typical for rare disease gene therapies [N1][N2][S1]. Monitoring reimbursement frameworks amid evolving healthcare cost-containment reforms will also be important barriers to market penetration post-launch [S4][S16].

While no explicit guidance has been issued regarding launch timing or pricing strategies yet—reflecting typical early-stage biotech discretion—the industry-standard sequence implies pivotal data releases will inform partnering/collaboration decisions alongside internal planning for sales infrastructure development.

Capital Efficiency and Returns: Funding the Pipeline Amid Persistent Losses

Neurogene’s financial management reflects classical early-stage biotech dynamics—where substantial upfront losses coexist with robust capital reserves enabling continued clinical progression without immediate revenue streams [F1][S17][S19]. Year-end cash & equivalents stood at approximately $104 million supported by low liabilities culminating in an exceptionally healthy current ratio exceeding sixteen times sustains near-to-mid term runway assuming steady expenditure rates.

Despite sizable net losses approximating $90 million in fiscal year 2025 (down ~20% YoY), capital adequacy enables uninterrupted R&D investments particularly into NGN-401-driven trials leveraging firm cashflows from prior substantial equity raises—notably the November 2024 private placement contributing nearly $190 million net proceeds before expenses [F1][S19]. Operating cash flow burn rate moderated slightly from prior years but remains significant reflective of scale-up activity alongside fixed operating costs intrinsic to cGMP facility maintenance [F1].

Return metrics such as ROE currently sit near negative thirty-four percent consistent with pre-revenue status; dividend payments or share repurchases are absent aligning logically with reinvestment priorities focused on value creation through pipeline advancement rather than short-term returns distribution during this stage [F1][S17][S19].

Risk Landscape: Navigating Clinical Uncertainty and Competitive Innovation Pressure

Key risks confronting Neurogene reflect hallmark challenges inherent to pioneering novel gene therapies targeting rare neurological indications [S4–S13][S16–S29]. With no products approved commercially yet the company is substantially dependent on successful NGN-401 development—a single point of failure exposure amplified given limited diversification beyond initial pipeline candidates at present.

Clinical trial outcomes remain uncertain particularly due to narrow therapeutic window disease biology mandating exact dosing achievable only through proprietary EXACT control; ineffective modulation or unforeseen adverse events could jeopardize regulatory filings.

Manufacturing scale-up risks persist given reliance on Houston facility which although offering strategic strengths is subject to geographic catastrophe hazards (e.g., hurricanes) substantiated historically—such as disruption during July 2024 Hurricane Beryl necessitating contingency power measures impacting production flow albeit without material effect ultimately noted [S9].

Collaborative dependencies include exclusive licensing interactions with University of Edinburgh providing preclinical innovation pipelines introducing potential operational risks if partnership terms falter or collaboration slows innovation velocity.

Regulatory complexity is heightened amid evolving frameworks governing gene therapy products globally including post-marketing pharmacovigilance requirements adding compliance burdens post-launch while pricing pressure environment tightens due to government healthcare policies aimed at drug cost containment increasingly influencing reimbursement scenarios broadly across biopharma sectors [S16– S20].[](https://www.sec.gov/Archives/edgar/data/1404644/000140464426000019/ngne-10k.htm)

Competitive arena encompasses other gene therapy developers pursuing alternative vector designs or delivery modalities addressing similar monogenic CNS disorders necessitating continuous scientific differentiation efforts maintaining intellectual property strength protecting technological edges from infringement challenges or generic biosimilar entrants [S22].

Disclaimer: This report is for informational purposes only reflecting data available as of March 24, 2026; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments