New Mountain Finance Corp’s Portfolio Volatility Dampens Earnings Despite Strong Cash Flow

NMFC’s 2025 results reveal portfolio depreciation pressures and leveraged capital management amid stable distribution commitments.

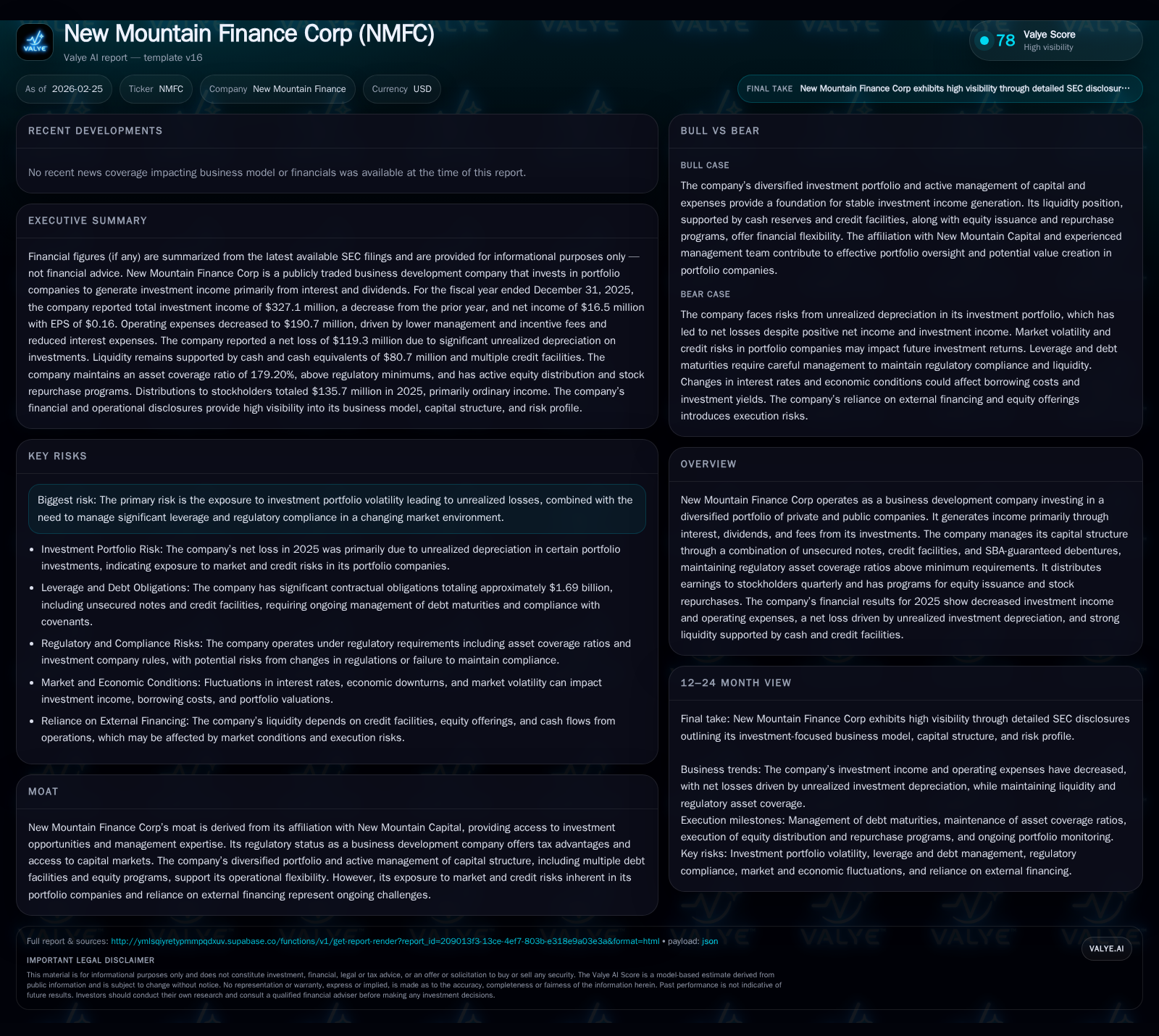

New Mountain Finance Corp (NMFC) reported a significant net income decline in 2025 driven chiefly by unrealized investment losses despite stable operational earnings and robust operating cash flow. The company's affiliation with New Mountain Capital and its diversified portfolio strategy underpin its investment approach, but market and credit volatility have introduced considerable fluctuations in fair value adjustments. NMFC maintains a strategic liquidity position supported by multiple credit facilities and equity programs, allowing it to continue regular shareholder distributions and pursue opportunistic share repurchases. Future growth hinges on portfolio performance stabilization, effective capital structure management, and the broader private credit market environment.

Historical Performance and Growth Drivers

New Mountain Finance Corp (NMFC) operates as a business development company (BDC), investing across a diversified portfolio of private and public companies with primary income from interest, dividends, and investment-related fees [S1]. Over the past four years through FY2025, NMFC experienced volatile net income owing largely to fluctuating realized and unrealized gains or losses on its investments.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Net YoY |

|---|---|---|---|

| 2025 | 16 | 379 | -85.5% |

| 2024 | 113 | 42 | -16.2% |

| 2023 | 135 | 333 | +81.1% |

| 2022 | 75 | 35 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, OpInc, Capex, Buybacks, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | ROE% |

|---|---|---|

| 2025 | 136 | 1.4 |

| 2024 | 147 | 8.4 |

| 2023 | 151 | 10.3 |

| 2022 | 121 | 5.7 |

Source: SEC companyfacts cache [F1].

Note: Revenue and operating income metrics are not available in provided data tags.

In FY2025, NMFC's net income contracted sharply by approximately $97 million relative to FY2024, driven largely by an extensive unrealized loss of $162.6 million related to fair value declines in certain portfolio companies (notably TVG-Edmentum Holdings and ACI Parent Inc.) partially offset by realized gains including those from OA Topco [S1][S20]. This contrasts with FY2024 where unrealized appreciation was positive at $15.7 million.

The total investment income for FY2025 dropped about $44.6 million versus the prior year due to lower invested assets and reduced portfolio yields—cash interest declined by over $36 million and dividend income also fell notably [S1][S15]. However, strong realized cash flows from operations manifested in an extraordinary increase of operating cash flow (CFO) to nearly $379 million in FY2025 from only $42 million in FY2024, underscoring robust underlying portfolio cash generation despite valuation headwinds [F1].

Net operating expenses decreased by approximately $35 million in FY2025 compared to FY2024 mostly due to management fee reductions tied to asset declines and an incentive fee waiver that halved incentive expense [$17.9M vs $36.4M] [S23]. Interest expense benefited from both lower SOFR rates on floating rate debt facilities and reduced total borrowings following refinancings of the NMFC Credit Facility and Holdings Credit Facility [S15][S23].

Portfolio Composition and Investment Strategy

A key structural advantage for NMFC is its affiliation with New Mountain Capital, providing access to proprietary deal sourcing capabilities and operational expertise which broadens the investment funnel . The portfolio spans senior secured loans, subordinated debt, preferred equity, common equity positions, as well as dividend-bearing investments across diverse sectors.

Investment income sources split roughly as follows: cash interest ($201M), payment-in-kind interest ($30M), dividends (both cash $49M plus non-cash ~$29M), other fees ($8.8M) contributing to total investment income of $327 million in FY2025 [S1]. However, a noticeable reduction in preferred equity holdings contributed to lower dividend income relative to past periods.

The company prudently manages its asset coverage ratios abiding by Section 61(a) of the Investment Company Act of 1940; as of December 31, 2025, the asset coverage ratio stood at a comfortable 179.2%, well above the regulatory minimum of 150%, enabling additional leverage capacity if prudent opportunities arise [S4][S8].

The diversified capital structure consists predominantly of unsecured notes nearing $1 billion face value across maturities from January 2026 through November 2028; revolving credit facilities offer flexible liquidity ($446 million capacity undrawn under the NMFC Credit Facility alone), alongside SBA-guaranteed debentures maturing staggered through September 2028 [S8][S14][S18]. This multi-source funding approach provides operational agility amidst market cycles.

Capital Allocation & Returns

NMFC has demonstrated consistent capital return commitment through quarterly distributions totaling approximately $135.7 million in fiscal year 2025 ($1.28 per share), slightly below prior years’ payouts but supported sustainably by high net investment income cash flows [S10][F1]. The tax character disclosed shows distributions predominantly comprising ordinary income (91%), with modest returns of capital (~8%) indicating preservation of capital base.

Significantly, NMFC pursued active share repurchases during FY2025 under board-authorized programs; approximately $52 million worth of common stock was repurchased combining completion of an older program ($47 million) plus accelerated buying under a new program launched late in the year [$95 million remaining capacity] [S12]. Such repurchases suggest management views current valuations as opportunistic while balancing liquidity needs.

Return on equity remains modest at about 1.4% for FY2025 calculated as net income over average equity base reflecting the drag from unrealized losses despite solid operational cash generation [F1]. This ratio is atypically low given recent valuation reversals but may rebound pending portfolio mark-to-market recovery.

Risks & Challenges

NMFC’s principal risk stems from volatility inherent to its credit-focused private equity investments which carry non-public valuations subject to market sentiment shifts causing large unrealized swings impacting reported earnings though less so on underlying cash-producing ability [S20]. Managing leverage prudently under regulatory coverage requirements remains crucial especially amid tightening debt markets or increased issuer distress.

Additionally, reliance on external financing through unsecured notes and revolving credit agreements means funding costs are exposed to prevailing interest rate environments; however, recent refinancing efforts have lowered spreads mitigating some risk [S15][S23]. Operationally, maintaining disciplined underwriting standards amidst competitive deal markets will be essential going forward.

Regulatory compliance with BDC-specific rules combined with governance around affiliated transactions (notably co-investment policies governed by SEC exemptive orders) adds another layer of oversight complexity but also opportunity for aligned investing alongside related parties within stipulated safeguards [S22].

Future Outlook: Catalysts & Monitors

No explicit forward guidance was issued for upcoming periods; analysis suggests key watch points include:

- Stabilization or reversal of unrealized depreciation trends in core portfolio companies,

- Continued maintenance or expansion of asset coverage ratios enabling prudent leverage deployment,

- Further refinancings or expansions of credit facilities to keep funding costs competitive,

- Outcomes from existing co-investment arrangements enhancing deal flow access,

- Trends in distributions sustaining payout levels aligned with net investment income,

- Market environment for private credit (including default rates trends).

Equity issuance activity paused in FY2025 with no shares sold under ATM offerings contrasting prior years when proceeds funded investments/debt paydowns implying balance sheet discipline presently [S7]. Liquidity remains robust supported by undrawn revolvers exceeding $400 million coupled with substantial operating cash inflows affording financial flexibility for opportunistic deployments or capital returns.

Conclusion

New Mountain Finance Corp’s latest annual results reveal an underlying business grappling with marked private investment valuation challenges amid otherwise strong operational performance showcased by rising cash flows supporting distributions and capital management activities like share buybacks. The combination of asset coverage well above regulatory minimums alongside a multi-faceted debt platform provides financial resilience while leveraging affiliation advantages via New Mountain Capital enhances sourcing capabilities. Resultant short-term earnings compression appears tied mainly to non-cash factors — anchoring medium-term prospects on portfolio recovery trajectories and ongoing disciplined capital stewardship within volatile credit market conditions.

This report is based solely on publicly available information cited herein without any forward-looking harm assumptions beyond disclosed data points or insights inferred from sector context. It does not constitute investment advice or recommendations regarding securities issued by New Mountain Finance Corp or any other entity.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments