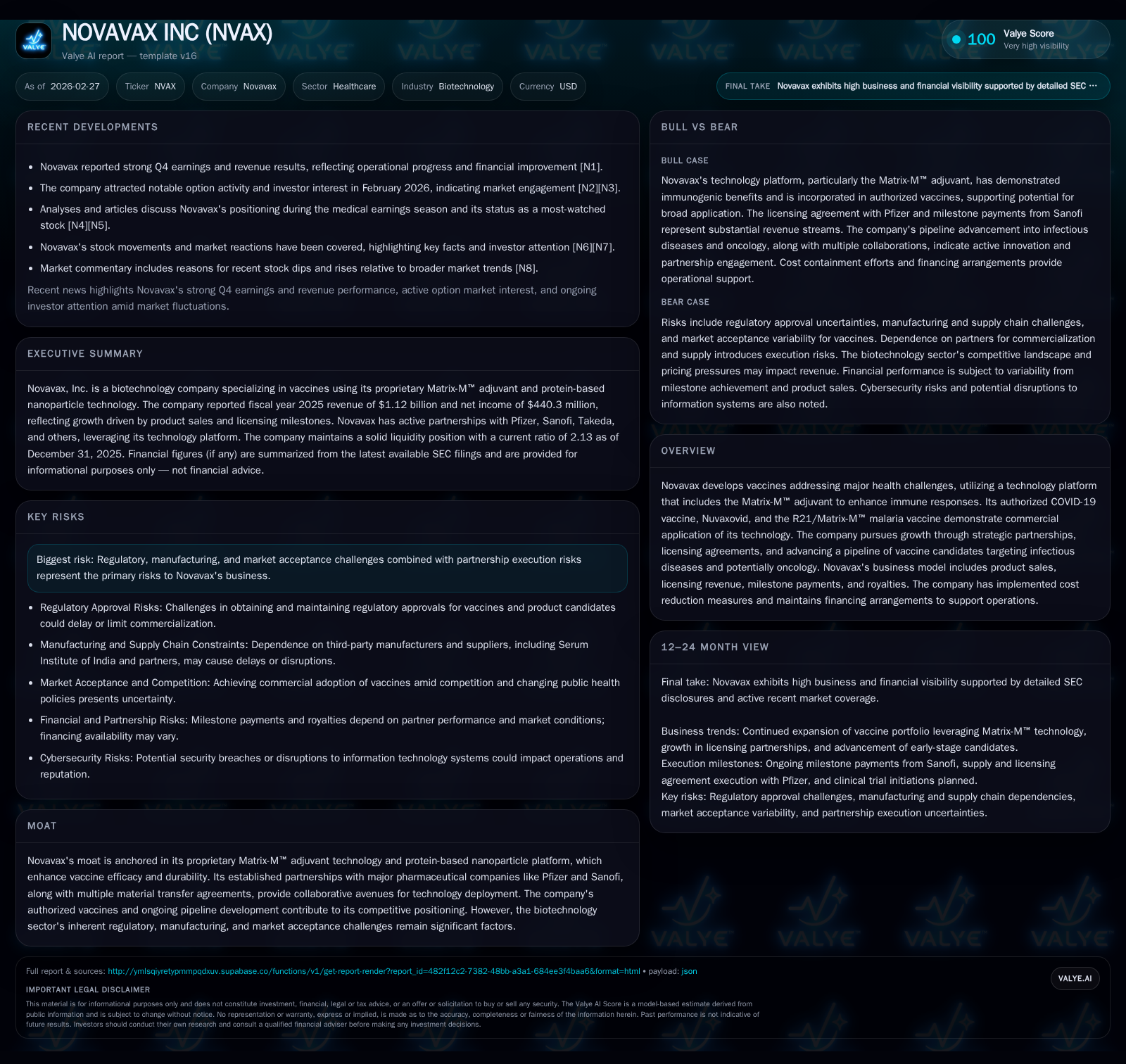

Novavax's Return to Profitability: Vaccine Innovation Fuels Growth

Novavax reversed multi-year losses in 2025 through its proprietary vaccine technologies and strategic partnerships, setting a foundation for sustained growth.

Novavax marked a significant financial turnaround in 2025, posting $1.12 billion in revenue—a 64.7% increase year-over-year—and turning operating income positive at $453 million after sustained losses. Central to this resurgence is its Matrix-M™ adjuvant and protein subunit vaccine platform, powering authorized vaccines like Nuvaxovid and the R21 malaria candidate, alongside lucrative licensing deals with industry majors Pfizer and Sanofi. Despite challenges including regulatory scrutiny and manufacturing complexities, Novavax’s capital structure adjustments and strategic collaborations underpin expectations of continued pipeline advancement and potential revenue expansion.

From Losses to Earnings: Tracing Novavax’s Recent Financial Transformation

Novavax delivered a remarkable financial turnaround in fiscal year (FY) 2025 compared to prior years marked by heavy losses. Revenue accelerated by 64.7% to approximately $1.12 billion [F1], principally fueled by increased sales of its COVID-19 vaccine Nuvaxovid along with licensing income from collaborators. Operating income flipped from a negative $249 million in FY2024 to a positive $452.8 million in FY2025 [F1], epitomizing improved operational leverage and cost optimization initiatives embedded within its restructuring plan [S1]. Net income also reversed sharply from a loss of $187.5 million to a gain of $440.3 million [F1]. The company attributes this inflection largely to higher product sales scaling combined with milestone payments realized under license agreements and disciplined expense management [N1][S1]. Despite these earnings gains, operating cash flow remained negative at -$244.6 million reflecting continuing investments in production capacity, R&D efforts, and inventory working capital changes [F1][S6].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 1123 | 440 | -245 | 453 | +64.7% | +334.8% |

| 2024 | 682 | -187 | -87 | -249 | -30.7% | +65.6% |

| 2023 | 984 | -545 | -714 | -567 | -50.4% | +17.2% |

| 2022 | 1982 | -658 | -416 | -645 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -344.7 |

| 2024 | 30.1 |

| 2023 | 76.0 |

| 2022 | 103.8 |

Source: SEC companyfacts cache [F1].

Table shows pronounced recovery across top- and bottom-line metrics from FY2024 to FY2025 [F1].

Matrix-M™ Technology and Key Vaccines: Innovating the Competitive Edge

At the core of Novavax’s resurgence is its proprietary protein subunit nanoparticle platform augmented by the Matrix-M™ adjuvant technology [S21]. This adjuvant enhances immunogenicity by improving antigen presentation and immune responses while maintaining favorable tolerability profiles. Matrix-M™ powers the authorized Nuvaxovid COVID-19 vaccine and the R21 malaria vaccine commercialized by Serum Institute of India, which has sold over 30 million doses since mid-2024 achieving more than an 80% market share in target territories [S21].

The company licenses Matrix-M™ broadly: Pfizer secured a non-exclusive license for two infectious disease indications with an upfront payment of $30 million plus potential development milestones up to $500 million along with tiered royalties [S20][N14]; similarly, Sanofi holds rights through their collaboration agreement enabling milestone payments and royalties linked to COVID-19 vaccine commercialization progress [S20][S28]. These partnerships validate Matrix-M™’s applicability across diverse vaccine candidates leveraging protein subunit platforms.

Growth Catalysts in 2025: Licensing, Milestones, and Market Dynamics

Principal revenue streams driving growth combine product sales—predominantly Nuvaxovid vaccine doses—supply sales including adjuvant, licensing fees, milestone payments, royalties, and technology transfer fees under strategic collaborations particularly with Sanofi Pasteur Inc., Takeda, Pfizer, Serum Institute of India among others [S25][N1][S28].

Sanofi payments alone totaled approximately $225 million in milestones recognized during full year 2025 linked to U.S FDA approvals for pre-filled syringes and corresponding European Medicines Agency marketing transfers [S11][S29]. Other partners contributed increasing revenues notably Takeda following expanded rights for Japan with upfront fees plus royalties surpassing previous periods by sizeable margins [S25][S27]. Analysts responded positively to these catalysts prompting share upgrades reflecting confidence in expanding booster label approvals globally enhancing demand outlook for updated COVID-19 formulations going into vaccination seasons [N5].

Barriers Ahead: Regulatory Hurdles, Manufacturing Risks, and Market Penetration Challenges

Despite promising growth trajectories anchored by Matrix-M™ innovation, material risks persist that could challenge sustainability.

The regulatory pathway entails rigorous process qualification activities including assay validation essential for lot release consistency meeting FDA or EMA standards—potential points of delay or audit scrutiny must be continuously managed given evolving variant-strain formulations [S11][S13][S14][S23]. Manufacturing scale-up reliance on contract manufacturing organizations introduces complexities around fill-finish operations affecting capacity utilization; costs related to excess or unused capacity previously incurred highlight operational risk exposures requiring optimized supply chain coordination [S9][S18]. Moreover, global health policy shifts such as modifying vaccine mandates or reimbursement models could influence market acceptance dynamics especially for booster dose demand seasonality uncertainties [S13][N5]. Execution risks around collaborative agreements—ensuring technology transfer milestones are achieved timely between partners—also remain notable factors impacting near-to-medium-term commercial forecasts.

Capital Strategies: Convertible Notes, Credit Facilities, and Share Offerings

Novavax’s financing moves underpin operational runway amid ongoing R&D commitments.

In August 2025, the company issued $225 million aggregate principal amount of convertible senior notes due in 2031 at an interest rate of 4.625%, including an exchange element replacing older convertible notes due in 2027 plus new cash proceeds enhancing liquidity [S4][S5][S7]. Complementing this was a February 2026 senior secured term loan credit agreement providing up to $330 million across four tranches with initial availability booked at $50 million; these loans carry an interest rate comprised of Term SOFR plus five percent subject to floor provisions maturing in March 2031 [S4][S6][S10]. Equity financing also features via strategic placements such as the private stock offering completed in May 2024 raising approximately $68.8 million from Sanofi [S5]. These capital sources collectively afford Novavax financial flexibility supporting planned clinical trial expansions while navigating volatile biotech funding conditions.

Performance Metrics Spotlight: Operating Income, Cash Flow, and ROE Insights

While profitability returned solidly in the latest period reflecting roughly a 40% operating margin based on revenues of $1.12 billion versus operating income of about $453 million [F1], cash flow indicators present a contrasting view.

Operating cash flow was negative approximately $245 million for FY2025 despite net income positivity due mainly to working capital effects including timing variances on receivables from advance purchase agreements across regions supplied directly or via partners [F1][S6]. Negative free cash flow continues when factoring capital expenditures supporting infrastructure rationalization and R&D facilities scaled down yet maintained for pipeline advancement initiatives [F1][S9]. Furthermore, equity remains deeply negative at about -$128 million reflecting accumulated historical losses partially offset by new capital raises; consequently computed ROE stands near negative -345%, signaling balance sheet strains common among emerging-stage biotechs transitioning toward consistent earnings generation [F1].

This dichotomy underscores that earnings quality may yet be susceptible to external funding cycles despite operating leverage gains.

Outlook Signals: Pipeline Progress, Partnership Expansion, and Investor Watchpoints

Looking forward into early-to-mid-2026 horizons:

- Novavax continues advancing Phase 2b/3 clinical trials such as the Hummingbird™ program targeting COVID-19 variant strain adaptations positioning itself for Biologics License Application filings ahead of upcoming vaccination seasons [N1][S28].

- Development of combination COVID-19/influenza candidate vaccines progresses alongside standalone influenza programs under partnership frameworks primarily executed through Sanofi collaboration pipeline efforts with encouraging early data releases reported recently [N1][S28].

- The Pfizer Matrix-M™ license arrangement signed January 2026 unlocks new infectious disease product opportunities along with significant milestone payment potential totaling up to half-a-billion dollars plus royalties if development/commercial success materializes; supply obligations regarding adjuvant provision place additional importance on manufacturing scalability capacities being met reliably [N14][S20].

- Preclinical research is expanding into oncology applications leveraging adjuvant immunomodulatory properties aiming toward initiating clinical investigations as soon as calendar year 2027 per management disclosures—representing potential strategic diversification beyond solely infectious diseases [N5][S20].

Investors should monitor regulatory filings progress including post-marketing study completions required under current approvals plus any changes in global vaccination program uptake particularly amid shifting epidemiological landscapes [S28]. Partnership cadence updates involving new material transfer agreements or licensing expansion may also presage further value inflection points.

This analysis synthesizes publicly filed financial data and corporate disclosures without expressing investment advice or recommendations concerning Novavax Inc.’s securities or business prospects.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments