Nvni Group Ltd: Navigating liquidity crisis amid AI-driven ambitions and Nasdaq compliance challenges

Nvni Group Ltd struggles with liquidity constraints and Nasdaq's market value deficiency while betting on strategic acquisitions and AI projects.

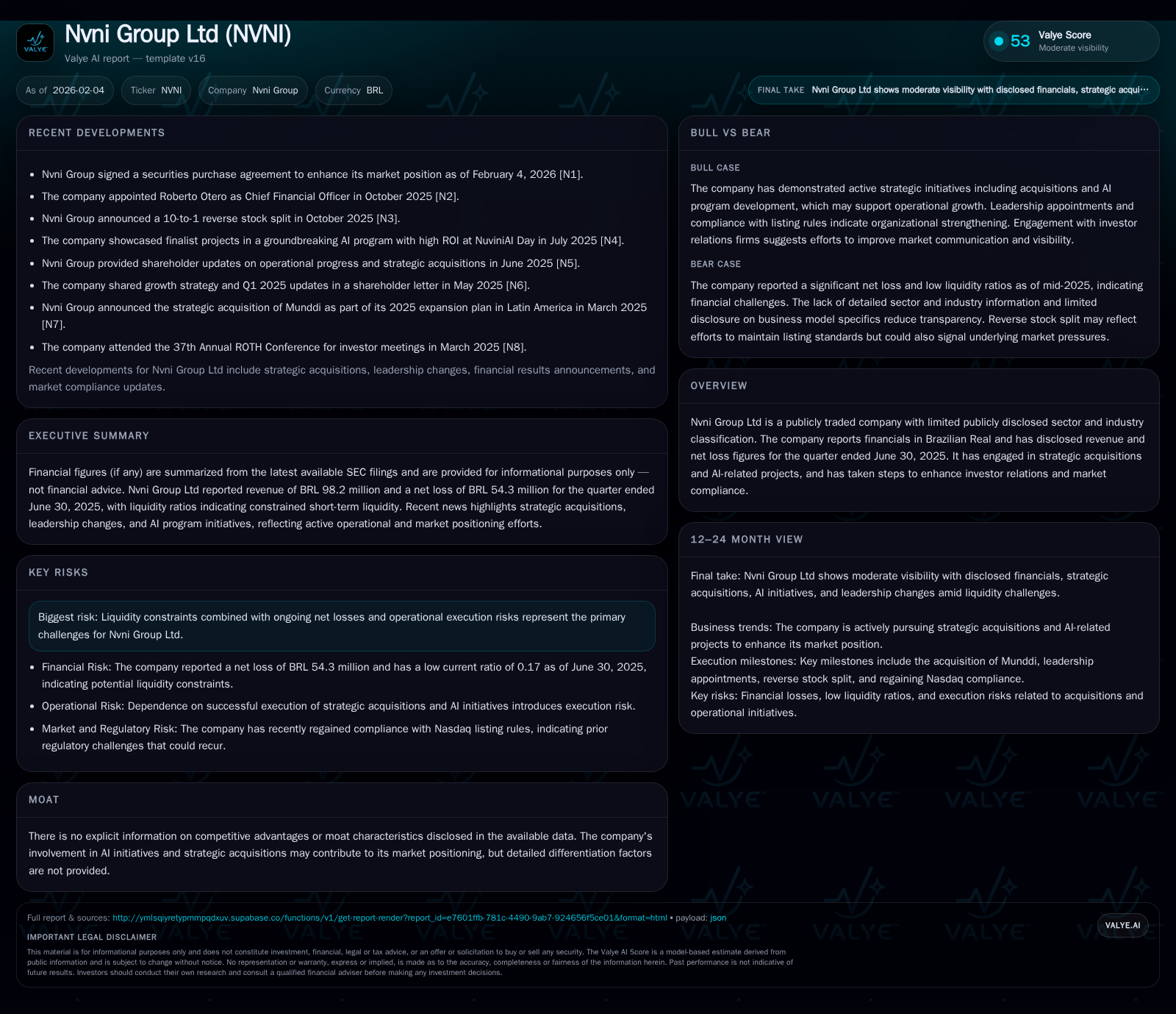

Nvni Group Ltd’s latest quarterly results reveal a stark financial imbalance: revenues of BRL 98 million contrasted against sizable losses exceeding BRL 54 million and a dangerously low current ratio of 0.17. The company faces a looming deadline imposed by Nasdaq following its market value deficiency notification, compelling urgent remedial measures. While sector ambiguity clouds the company’s precise market positioning, its strategic acquisitions and AI initiatives signal ambitions to pivot toward tech-enabled growth, albeit execution risks remain pronounced. Investor relations moves, including a securities purchase agreement, reflect efforts to stabilize and reset in the face of multifaceted pressures.

At the Crossroads: Nvni Group's Financial Landscape

The tale of Nvni Group Ltd is one marked by contrasts that amplify investor unease: the latest quarter ending June 30, 2025 reveals robust top-line generation at nearly BRL 98 million yet this was overshadowed dramatically by a net loss tallying over BRL 54 million [F1]. More strikingly, the firm's liquidity bears deep scars — current assets totaled approximately BRL 62.7 million against staggering current liabilities eclipsing BRL 376 million. This imbalance delivers an ominously thin current ratio of just 0.17, painting a portrait of short-term survival under severe strain.

This financial snapshot illuminates a company at a crossroads — propelled by ambition yet hobbled by cash flow fragility and operational challenges. The scale of losses juxtaposed with massive short-term obligations requires balancing acts rarely simple for emerging AI-driven ventures or entities in restructuring phases.

Peering Behind the Curtain: Understanding Nvni’s Sector Ambiguity

A notable enigma surrounding Nvni lies in its murky sector classification. Public disclosures shy from assigning it to a distinct industry vertical, leaving external observers navigating in informational fog [valye_report_excerpt]. However, references to strategic acquisitions along with AI-related projects suggest an orientation towards technology-driven innovation.

This opacity carries dual-edged implications: it complicates investor assessment frameworks reliant on peer comparisons or sectoral benchmarks; simultaneously it affords Nvni latitude to forge novel business models that might defy traditional pigeonholing. Yet absent clearer operational narratives or product-level detail, the company's exact footprint within competitive markets remains an open question.

The Promise and Peril of Strategic Acquisitions and AI Ventures

Nvni's disclosed strategy hinges partly on leveraging acquisitions and AI projects as engines for growth [valye_report_excerpt]. Such moves can act as pathways toward differentiation in crowded markets if executed proficiently. However, the scant public details leave critical uncertainties unaddressed — which assets or capabilities were acquired? How integrated are these new units? What specific AI applications are underway?

Execution risk looms large here. Many firms stumble converting bold M&A intentions into tangible operational synergies or scalable technology platforms. Without transparent milestones or measurable outcomes shared publicly thus far, scrutiny rightly falls on whether Nvni’s transformational bets will bear fruit or deepen resource drains.

Liquidity Under Pressure: Gauging Short-Term Survival Risks

The company’s balance sheet figures place liquidity constraints front and center [F1]. With cash & equivalents standing at roughly BRL 16.4 million juxtaposed against quarterly net losses north of BRL 54 million, burn rates hint at rapid depletion risks absent fresh capital inputs. Furthermore, current liabilities exceed current assets by an order of magnitude — suggesting impending refinancing needs or restructurings must be prioritized.

Such pressure amplifies operational execution risks; suppliers, lenders, or service providers may demand stricter terms or limits to exposure. The risk is not only that day-to-day operations become harder but that investor confidence deteriorates further.

Nasdaq Compliance Drama: MVLS Warning and Its Implications

A pivotal recent development is Nasdaq’s official notification delivered on January 28, 2026 [S2]. For over 30 consecutive trading days from December through late January, Nvni's market value of listed securities (MVLS) failed to meet the US$35 million minimum mandated for continued listing on the Nasdaq Capital Market.

This sets a compliance clock ticking — the company has until July 27, 2026 to regain MVLS compliance across at least ten consecutive trading days [S2]. Failure to do so risks delisting proceedings with all attendant geopolitical friction and liquidity consequences that ensue.

The notice itself does not impact immediate trading status but represents a material risk factor influencing share price volatility and investor sentiment sharply. This marketplace crucible adds urgency to capital strategy decisions.

Investor Relations Initiatives: Signals of Strategic Reset

In response to the Nasdaq letter and precarious liquidity state, Nvni announced entry into a Securities Purchase Agreement aimed at shoring up its market position [N1]. This move signals management’s acknowledgement of capital scarcity challenges coupled with willingness to pursue external financing avenues promptly.

Enhanced disclosures following these developments also point to efforts at rebuilding transparency bridges with shareholders and regulators alike [N1], [S2], [valye_report_excerpt]. Engaging the Nasdaq Listing Qualifications Department proactively reflects attempts at steering through compliance obstacles rather than reactive defensiveness.

Yet much hinges on execution here — both regarding timing of capital inflows and communication clarity enhancing investor confidence amid prevailing uncertainties.

Market Positioning in a Murky Competitive Field

Without clear industry classification or apparent competitive moat spelled out in disclosures [valye_report_excerpt], assessing Nvni's relative strength versus peers proves difficult. The absence of explicit differentiation attributes suggests the company either operates amid nascent market segments or is still constructing its unique value proposition.

Its AI initiatives and takeovers hint at building intellectual property or technology assets potentially central to future competitiveness; however, benchmarking against established tech players highlights substantial gaps yet to be bridged. In essence, while these initiatives represent hopeful signposts for long-term positioning they also add layers of complexity reflective of early-stage risks.

Valuation Challenges Amid Sparse Data and Heavy Losses

The interplay between recurring operating losses above BRL 50 million per quarter [F1], opaque business model delineation, and looming regulatory headwinds complicates any valuation exercise for NVNI shares profoundly.

Investors typically apply risk premiums to such profiles; moreover, compliance uncertainty stemming from MVLS deficiencies enhances discount factors significantly [S2]. Market capitalization hovering below required Nasdaq thresholds restricts liquidity further exacerbating valuation opacity.

Without clearer growth trajectories or reliable profitability forecasts public stakeholders face high uncertainty margins which reflect in share price dynamics tightly entwined with regulatory news flow rather than fundamentals alone.

Pathways to Recovery: Opportunities and Pitfalls Ahead

Looking forward, Nvni has several urgent levers to pull:

- Achieving Nasdaq MVLS compliance by sustained share price recovery or capital injections before July’s deadline remains paramount.

- The recently inked Securities Purchase Agreement offers potential fuel if successfully closed mitigating immediate liquidity pressures [N1].

- Delivering tangible outcomes from strategic acquisitions and concrete progress on AI projects could catalyze re-rating scenarios if communicated transparently.

- Operational discipline must be heightened to narrow losses and extend runway given fragile balance sheet geometry.

- Continued engagement with regulators including Nasdaq should accompany proactive investor relations strengthening trust.

However, numerous pitfalls abound — failure in any single aspect could cascade into adverse feedback loops magnifying existing distress. Execution precision coupled with favorable market conditions will be decisive in rewriting digitized fortunes for Nvni amidst multiple headwinds.

Disclaimer: This analysis provides an informational overview based on currently available public disclosures as of February 2026. It does not constitute investment advice nor an endorsement of Nvni Group Ltd’s securities. Readers should conduct independent due diligence before forming financial conclusions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments