enVVeno Medical's Quest to Transform Severe CVI Treatment with Next-Gen Valves

enVVeno Medical pivots from a non-approved surgical valve to a minimally invasive venous valve technology for severe Chronic Venous Insufficiency.

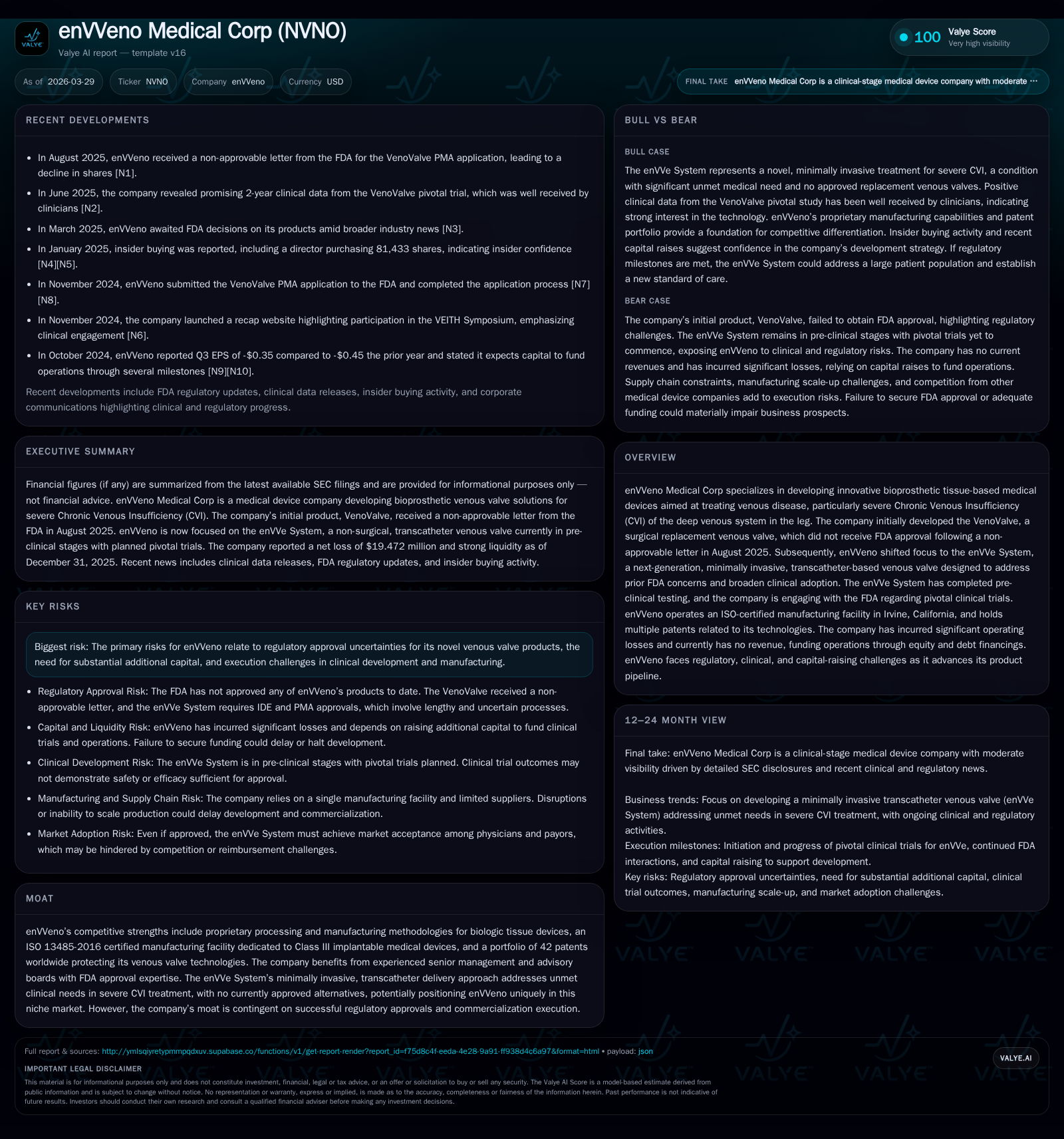

enVVeno Medical has endured significant financial losses driven by intensive R&D investments aimed at correcting the FDA setback received in August 2025 for its inaugural VenoValve device. The company's strategic shift towards the enVVe System, a transcatheter-based minimally invasive venous valve, responds to unmet clinical needs in treating severe CVI and addresses prior regulatory concerns. Although regulatory approval remains uncertain, the company’s ISO-certified manufacturing infrastructure and broad patent portfolio position it uniquely in this niche market. Ongoing dialogues with the FDA regarding pivotal clinical trials and a robust balance sheet with strong liquidity offer support but underscore capital sufficiency challenges amid the path toward commercialization.

Financial Trajectory: Losses Amid R&D Investment

Since its inception, enVVeno Medical has operated at a significant loss driven primarily by expansive research and development efforts focused on pioneering venous valve therapies. The company's latest fiscal year (FY2025) operating income was negative $20.9 million, improving modestly by approximately 12.3% year-over-year from the prior year's $23.8 million loss [F1]. Net losses followed a similar narrowing trend, arriving at $19.5 million in FY2025 compared to $21.8 million in FY2024.

Operating cash flow remains negative at $15.6 million in FY2025 but improved by 7.5% year-over-year, reflecting operational tightening even as product development escalates [F1]. Capital expenditures contracted steeply by over 80%, down to just $5 thousand, consistent with limited fixed asset investments typical of a pre-commercial medtech firm focusing on prototype refinement over infrastructure expansion [F1]. Equity declined noticeably from $42.2 million in FY2024 to $27.1 million in FY2025 – illustrating ongoing capital consumption amid no revenue generation [F1].

These financial dynamics encapsulate an early-stage medical device company's familiar profile: ongoing losses fueled by clinical development and regulatory processes, with gradual strides toward profitability contingent on product approval and commercialization.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -19 | -16 | -21 | 5000 | +10.8% |

| 2024 | -22 | -17 | -24 | 37000 | +7.2% |

| 2023 | -24 | -19 | -25 | 33000 | +4.7% |

| 2022 | -25 | -16 | -25 | 115000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -16 | -71.8 |

| 2024 | -17 | -51.8 |

| 2023 | -19 | -50.9 |

| 2022 | -16 | -63.7 |

Source: SEC companyfacts cache [F1].

FY figures reflect full-year periods ending December 31 per SEC filings [F1]

Addressing the Unmet: Innovation in CVI Treatment

Chronic Venous Disease (CVD), affecting roughly 70% of U.S adults with the most severe subcategory being Chronic Venous Insufficiency (CVI), presents profound clinical challenges often culminating in venous hypertension and non-healing ulcers [S1]. CVI severity is clinically classified using CEAP taxonomy; enVVeno targets patients categorized C4 through C6—those with skin changes and active venous ulcers.

The company’s initial innovation—the VenoValve—was a first-in-class surgical replacement valve implanted via open surgery designed to restore valve competence in the deep venous system of the leg [S1]. However, safety issues related to the invasiveness of this approach contributed to its failed FDA PMA submission.

Pivoting from this setback, enVVeno developed the enVVe System—a proprietary bioprosthetic tissue-based valve deployed through a minimally invasive transcatheter approach [S1]. This design innovation aims to mitigate complications inherent in open surgery by enabling percutaneous implantation via catheter-based delivery systems that precisely position the one-way valve within deep leg veins.

This transcatheter method aligns with vascular intervention trends favoring reduced procedural morbidity and enhanced patient recovery times seen across cardiovascular device sectors.

By directly addressing difficult-to-treat severe CVI cases lacking approved valve replacement therapies today, the enVVe System serves an unmet medical need with potential to redefine treatment paradigms for C4-C6 CEAP patients.

Regulatory Roadblocks and FDA Interactions

In August 2025, enVVeno received a not-approvable letter from the FDA concerning its PMA application for the VenoValve device [S1][S19]. The agency cited unresolved safety concerns mainly related to adverse events from open surgical implantation requiring rehospitalizations.

Furthermore, the FDA indicated deficiencies in demonstrating effectiveness without hemodynamic measurements correlating convincingly with clinical symptom improvements—raising concerns about possible bias linked to study design rather than genuine device benefit [S19].

Following an unsuccessful supervisory appeal upholding these decisions as recently as November 2025 [S16], enVVeno intensified focus on developing the enVVe System designed explicitly to overcome such concerns through minimized invasiveness.

Currently, the company is engaged in ongoing discussions with the FDA regarding design and launch of pivotal clinical trials for enVVe [S1]. These trials will be critical regulatory milestones testing manufacturability and clinical efficacy hypotheses within new safety frameworks tailored to transcatheter valves.

However, significant uncertainty persists given no precedents exist for approved replacement venous valves in either surgical or catheter-delivered forms, and thus regulatory pathways must be negotiated while ensuring compliance with evolving Center for Devices and Radiological Health standards [S16]. This regulatory uncertainty constitutes a primary risk factor affecting prospective commercialization timelines and capital needs [S4].

Capital Allocation and Balance Sheet Health

enVVeno’s cash position stood at approximately $3.07 million as of FY2025 end against current liabilities near $2.12 million producing an exceptionally high current ratio of approximately 13.58x indicating operational liquidity sufficiency amid contractual short-term obligations [F1][S7].

Operating cash flows remain negative at approximately $15.6 million annually reflecting ongoing investment into trials and device refinement absent product sales cash inflows; capex outlays are minimal consistent with maintaining existing lease facilities rather than plant expansion [F1].

The company's equity base contracted from approximately $42 million end-FY2024 down to about $27 million end-FY2025 reflective of cumulative net losses decreasing shareholder value while no dividends or share buybacks have been undertaken — typical for firms prioritizing capital preservation during development phases [F1][S29].

Approximate return on equity based on net loss over equity yields roughly negative 72%, underscoring profitability constraints intrinsic to pipeline-stage medtech entities reliant on external funding rounds for sustained operations [F1].

Overall, enVVeno displays prudent capital stewardship preserving substantial liquidity buffers whilst emphasizing financing necessity ahead including possibilities for equity raises or strategic partnerships given their comprehensive development commitments [S7].

Operational Capabilities: Manufacturing and IP Strength

enVVeno operates an ISO 13485-2016 certified manufacturing facility situated in Irvine California dedicated exclusively to Class III implantable tissue-based medical devices ensuring adherence to rigorous quality system regulations necessary to produce implantables capable of meeting stringent FDA expectations [S1].

This facility supports proprietary processing methodologies integral to fabricating bioprosthetic valves distinguished by tissue preservation approaches enhancing durability and biocompatibility — core components of their technological moat alongside precision assembly suited for transcatheter delivery systems.

Their intellectual property portfolio comprises multiple granted patents globally including United States patents together with active patent applications further entrenching competitive barriers around unique device designs and manufacturing processes pertinent to venous valve replacements [S23].

These assets collectively reinforce structural advantages that could maintain market exclusivity pending successful regulatory approvals — yet are contingent upon overcoming legislative scrutiny risks impacting durability of patent rights as well as competitive entry considerations prevalent throughout medtech sectors.

Risk Overview: Regulatory, Financial, and Commercial Execution

enVVeno faces multifaceted risk exposures intrinsic to medtech innovators developing novel Class III devices under complex regulatory regimes including:

- Prolonged uncertainty surrounding FDA PMA approvals heightened by prior non-approvable determinations linked mainly to safety perceptions from surgical approaches raising questions about equivalently rigorous evidence thresholds for new transcatheter modalities [S4][S19].

- Significant capital requirements coupled with continuous operating losses necessitating timely access to funding sources; failure may result in delays or cessation of development programs impacting liquidity outlooks profoundly [S7][S21].

- Execution risks encompassing manufacturing scale-up challenges inclusive of third-party component dependencies that could impede clinical trial supplies or future commercialization volumes risking reputational damage if quality standards slip [S27][S28].

- Need for market acceptance among vascular surgeons accustomed to alternative care procedures entails extensive education efforts; lack of broad clinician buy-in may limit uptake undermining revenue growth prospects despite market need intensity [S22][S24].

- Evolving healthcare policy landscapes affecting reimbursement dynamics including Medicare payment reductions contributing downstream pricing pressures potentially diminishing economic incentives for adopters [S4][S18].

- Legal risks from product liability claims inherent in implantable device usage requiring robust insurance strategies amidst potential adverse event incidences post-market approval stages [S22][S25].

- Intellectual property litigation threatened by larger incumbents within a litigious medtech environment where invalidation or infringement suits could materially impair competitive positioning despite patent counts achieved so far [S26][S23].

These interwoven risks underscore the high stakes involved in translating cutting-edge biomedical engineering advances into sustainable commercial ventures within regulated healthcare ecosystems.

Disclaimer: This analysis is based exclusively on publicly available filings as referenced herein; it does not constitute investment advice or recommendations regarding enVVeno Medical’s securities or business prospects but aims solely to provide informed commentary rooted in disclosed information as of March 29th, 2026.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments