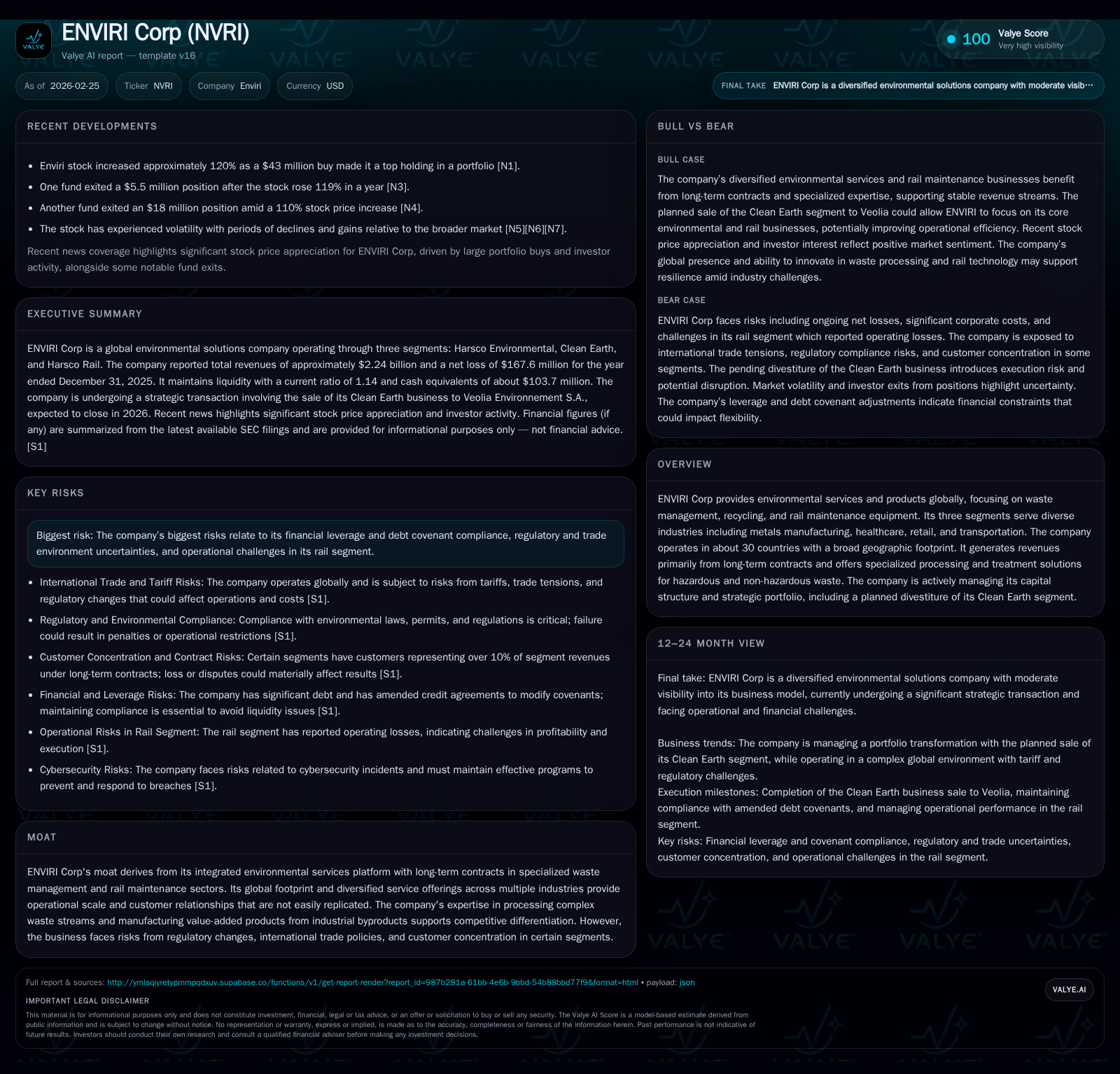

ENVIRI Corp’s Profit Squeeze and Strategic Portfolio Shift Amid Regulatory and Debt Pressures

Despite steady revenues from long-term contracts, ENVIRI Corp confronts operating income collapse and heavy leverage as it prepares to divest its Clean Earth segment.

ENVIRI Corp sustained consistent top-line revenue supported by a diversified, global platform with stable long-term contracts. However, operating income plunged over 85% year-over-year in 2025, pressured by cost inflation, regulatory challenges, and performance issues in its rail segment. Leverage remains elevated near covenant limits, prompting credit agreement amendments and a strategic evaluation that includes a Clean Earth segment divestiture aimed at improving capital structure. Operating cash flow improved notably but failed to offset heavy capital expenditures, resulting in negative free cash flow. Regulatory risks and customer concentration intensify uncertainties as the company navigates debt compliance and portfolio repositioning into 2026.

Revenue Growth Trends and Operating Margin Compression Through 2025

ENVIRI Corp demonstrated resilient top-line performance in fiscal 2025 with revenues of approximately $2.24 billion, representing a modest decline of -4.4% compared to $2.34 billion in 2024 [F1]. This stability was underpinned primarily by the company's extensive base of long-term contracts across its environmental services platform serving metals manufacturing, healthcare, retail, and transportation industries globally [S1]. The geographic diversification—spanning roughly 30 countries—and integrated service offerings have helped maintain consistent customer engagement despite challenging macroeconomic conditions.

However, this revenue consistency masks significant margin deterioration. The company reported a steep operating income decline of approximately -86.6% year-over-year to just $4.25 million in 2025 from over $31.7 million in the prior year [F1]. The collapse stems largely from rising input cost inflation—including energy prices and labor costs—heightened by the impact of new tariffs emanating from US and EU trade policies enacted during the year [S2]. Additionally, operational difficulties within the Rail Maintenance segment contributed disproportionately to margin pressure through unexpected costs and inefficiencies.

This confluence eroded operating margins substantially; the previously profitable years reversed into near breakeven territory by end-2025 [F1]. Net income followed suit with an increased loss reported at -$168 million in 2025 (versus -$128 million in 2024), reflecting limited offset from non-operating items and higher interest expense reflective of elevated leverage [F1]. The resultant approximate ROE stands deeply negative at -65.7%, underscoring poor profitability during scale.

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 2.2 | -168 | 101 | 4 | -4.4% | -31.0% |

| 2024 | 2.3 | -128 | 78 | 32 | +13.2% | -48.6% |

| 2023 | 2.1 | -86 | 114 | 111 | +9.5% | +52.2% |

| 2022 | 1.9 | -180 | 151 | -57 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex, Div, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -40 | -65.7 |

| 2024 | -59 | -31.1 |

| 2023 | -25 | -16.5 |

| 2022 | 13 | -31.6 |

Source: SEC companyfacts cache [F1].

Note: ROE calculation approximated as Net Income / Stockholders’ Equity; Buybacks/Dividends omitted due to lack of recent distributions [F1].

Segment Performance Spotlight: Environmental Services, Clean Earth, and Rail Maintenance

Four major themes dominate the operational narrative across ENVIRI's segments:

Harsco Environmental (HE): Core provider of on-site environmental services handling waste and byproduct streams mainly for metals manufacturing sites worldwide generating stable recurring revenues from long-term contracts supplemented by value-added ecoproducts like road surfacing materials and metallurgical additives [S10][S11].

Clean Earth (CE): Focused on specialty waste processing including hazardous/non-hazardous treatment primarily across US industrial/retail/healthcare sectors facing heightened regulatory compliance costs especially lawsuits/civil penalties involving EPA actions, contributing substantial restructuring considerations impacting segment profitability [S14][S19][N1].

Harsco Rail: Supplier of specialized railway track maintenance equipment—an asset-heavy capital goods business providing aftermarket parts/services targeting large railway systems but challenged operationally by project delays coupled with customer concentration issues possibly affecting quarter-to-quarter earnings volatility [S14].

While HE sustains relative stability due to entrenched contracts with steel mills globally—even contending with risks tied to customer consolidation—the CE division is clearly grappling with mounting costs arising from environmental investigations and remedial responsibilities especially at key hazardous waste facilities in Kentucky and California with EPA settlements recorded [S19][S27]. The Rail segment’s engineering-intensive track maintenance solutions constitute a competitive moat via high technical barriers but simultaneous execution risks are apparent due to complex logistics inherent to maintenance-of-way equipment deployment.

November 2025 marked a critical juncture when management announced plans evaluating strategic alternatives for the Clean Earth business including tax-efficient sale or separation transactions signaling priority portfolio reshaping aimed at unlocking shareholder value while addressing capital structure rigidity [N1][S2].

Debt Profile and Leverage: Navigating Credit Agreement Amendments and Covenant Compliance

ENVIRI entered fiscal year-end December 31, 2025 carrying approximately $1.48 billion of total debt comprised primarily of senior secured revolving credit facilities ($526M), term loans ($478M), plus senior notes totaling $475M [S8][F1]. The company operates under covenant constraints defined notably by a net debt to consolidated adjusted EBITDA ratio capped at varying levels contingent on amortization schedule and negotiated amendments.

Following projected strain on covenant ratios owing to margin compression forecasts during late-2025 Q3/Q4 periods, ENVIRI proactively negotiated several credit agreement amendments between late-2024 through early-2026 permitting flexibility including raising acceptable net leverage thresholds temporarily up to 5.50x before scheduled step-downs toward a more normalized ~4.00x target by mid-2027 [S7][S16][S13]. As of December end-2025 balance sheet measures indicated compliance with covenants showing net leverage at roughly 4.93x alongside an interest coverage ratio near minimum permissible levels (2.79x) indicative of tight liquidity headroom but not breach scenarios so far.

Importantly, these amendments explicitly accommodate the planned distribution/divestiture of the Clean Earth business which upon consummation would immediately reduce net leverage covenant ceilings substantially—from about ~5x down to approximately ~3x—reflecting the anticipated deleveraging effect of this portfolio move along with related indebtedness repayment expected as part of transaction structuring [S2][S21][S29]. Given that senior secured credit facilities are guaranteed by essentially all major domestic subsidiaries secured against most assets subject to mandatory prepayments on asset sales/cash flow triggers managing balances against such covenants stays critical.

The company also maintains an accounts receivables securitization program capped currently at $160 million aimed at accelerating working capital turnover that supports liquidity needs amid operating cash flow volatility common in service-heavy businesses.[S6]

Capital Allocation Patterns: Cash Flow Generation Versus Negative Free Cash Flow Trends

A noteworthy dynamic for ENVIRI is divergence between growing operating cash flow versus persistent negative free cash flow generation owing chiefly to stable investment demand.

Operating cash flow rebounded strongly (+29.9%) to approximately $101 million in FY2025 following controls over working capital coupled with steady contract collections compared to $78 million in prior year [F1]. This healthy cash inflow reflects management's efforts on accounts receivable optimization including expanded factoring arrangements facilitating conversion efficiency up the balance sheet.

However, capital expenditures remained elevated near historic run-rate levels ranging broadly between $136–141 million annually throughout financial years ’22–’25 signifying ongoing requirements tied predominantly to heavy equipment upkeep especially within Rail segment alongside facility upgrades within Environmental Services businesses ensuring compliance standards adherence [F1][S14]. Consequently, the free cash flow after capex turned negative (~-$40 million) highlighting persistent reinvestment needs exceeding internal cash generation capacity despite improved earnings scenario.

In parallel, neither dividend distributions nor share repurchases have been reported recently indicating capital allocation priorities skewed heavily towards debt reduction or strategic investments rather than shareholder returns given financial leverage considerations prevalent over past several years.[F1]

Strategic Portfolio Moves: Implications of the Planned Clean Earth Divestiture

Management announced explicit evaluation of multiple value creation alternatives for its largest US-centric specialty waste processing unit—Clean Earth—including potential tax-efficient sale or spin-off transactions aligning with industry trends focusing portfolio razor-sharpening for strategic coherence [N1][N3][S2].

The divestiture underscores two pivotal objectives:

- Achieving meaningful deleveraging will enhance flexibility on credit covenants given CE’s sizable contribution toward overall gross debt burdens;

- Mitigating growing regulatory/legal risk exposure tracked chiefly within hazardous waste handling functions where EPA enforcement actions as well as state-level penalties remain ongoing concerns affecting profitability outlook negatively.

Also relevant are anticipated proceeds estimated around mid-hundreds million USD range (market speculation), which will be partly directed toward prepaying term loans thus improving maturity profile alongside reduced interest charges potentially enhancing longer-term financial health.

Completion timing hinges on regulatory approvals plus buyer/transaction structure complexities given environmental liabilities entwined within cleaned earth assets requiring continued operational diligence even during transition phases.

Risks from Regulatory Changes, Tariffs, and Customer Concentration

ENVIRI faces multilayered external risks that complicate future growth trajectories:

- Regulatory pressure from environmental agencies across key jurisdictions including EPA investigations into hazardous waste operations plus local state regulators demanding corrective capital projects impose escalating compliance costs threatening margins directly [S19][S23];

- Trade tensions principally between US/EU have triggered tariff implementations affecting cost inputs mainly raw material imports leading indirectly to price pass-through challenges against highly competitive customer dynamics within metals manufacturing sector where HE is significant supplier [S2];

- Customer base exhibits pockets of concentration albeit none exceed >10% revenue alone at consolidated level; however loss or nonrenewal of large multi-contract customers particularly within steel markets or rail could provoke material earnings swings quarter-to-quarter due to contract-driven revenue recognition nature typical for maintenance-of-way equipment[S10];

- Legacy affairs such as DEA investigations into controlled substance disposal procedures inherited via Stericycle acquisition bear latent reputational/legal risks albeit management currently does not anticipate material accruals hereunder based on contractual indemnities available[S25];

- Environmental litigation like Newtown Creek Superfund Site involvement remain contingent risk factors requiring ongoing litigant monitoring in provisioning assessments[S19];

These external pressures require continued strategic agility alongside proactive regulatory engagement combined with robust internal compliance regimes led under dedicated executive leadership emphasizing cybersecurity/internal controls fostering risk mitigation effectiveness overall[S1].

What to Watch: Future Milestones, Debt Refinancing, and Segment Repositioning

Looking ahead through calendar years ‘26–‘27 key benchmarks provide important focus points:

- Timely execution on Clean Earth business divestiture remains paramount potential catalyst impacting both leverage metrics dramatically plus strategic refocus message conveyed toward investors committed keeping tighter control over risk exposures[N1][N3];

- Ongoing compliance trajectories regarding amended credit agreements particularly net leverage trending closely monitored given slim cushion afforded provides market signals tied closely with future refinancing opportunities or necessity thereof[S4];

- Operational improvement programs underway within Rail segment represent critical vector for margin restoration if successfully implemented coupled with opportunity pipeline expansion specifically through aftermarket parts/customized diagnostics solutions increasing recurring component revenue streams;

- Market volatility exemplified by significant fund buying/selling activities observed recently may be partly attributed to anticipatory positioning relative to aforementioned strategic developments hence share price dynamics serve as proxy indicator concerning sentiment shifts tabletop scenario developments[N6];

- Quarterly reporting cadence throughout ‘26 essential transparency moments evaluating corrective initiative effectiveness amid macroeconomic uncertainties particularly considering inflationary environment impact relevance on cost models[S3];

Collectively these milestones will shape near-to-medium term interplay between profit recovery efforts harnessed under leaner portfolio constructs against a backdrop complicated by structural indebtedness sensitivity requiring vigilant financial stewardship integrating sound capital allocation practices.

This analysis synthesizes publicly available regulatory filings including annual (10-K), quarterly (10-Q), current reports (8-K) filings along with recent news coverage without purporting any form of investment advice or recommendation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments