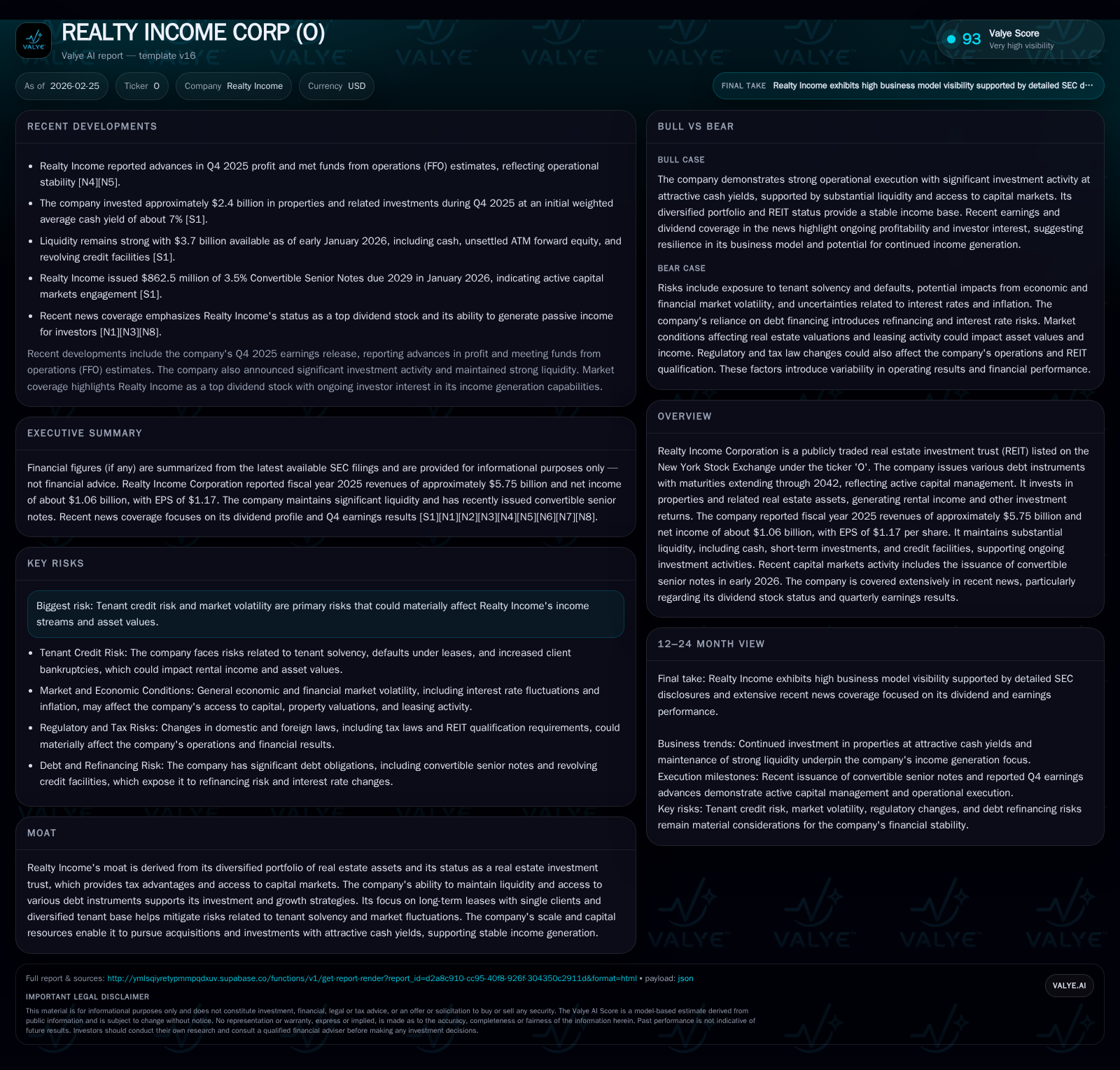

Realty Income’s Capital Expansion and Diversification Drive Growth with Dividend Stability

A look at how Realty Income Corp’s strategic geographic expansion, diversified portfolio, and capital issuance fuel robust revenue growth while maintaining liquidity and dividend strength.

Realty Income Corporation (ticker: O) has demonstrated consistent revenue and cash flow growth through a combination of strategic acquisitions and expansion into new geographies, especially across the U.K. and Europe. The company leverages its REIT structure with an active capital markets presence, including recent convertible senior notes issuance, to support acquisition activity averaging 7% initial weighted average cash yield. While net income grew 23% year-over-year in fiscal 2025, the company's return on equity remains modest at approximately 2.7%, reflecting its asset-heavy REIT model. Sustained dividend payments and sizable operating cash flows underpin Realty Income's reputation as a reliable dividend stock, but tenant credit risk and interest rate environment remain key considerations going forward.

Historical Performance: Consistent Revenue and Earnings Growth

Realty Income Corporation has recorded a strong growth trajectory over the past four fiscal years, underscored by its ability to generate rental income from a diversified property portfolio underpinned by long-term leases. The company reported revenues of approximately $5.75 billion for fiscal year ending December 31, 2025, up from $5.27 billion in FY24 — marking a solid year-over-year increase of roughly 9.1% [F1]. Meanwhile, net income improved markedly by 23% to about $1.06 billion in FY25 compared to $860.8 million in FY24 [F1]. This jump reflects both operational efficiencies as well as accretive acquisitions.

Operating cash flows have similarly trended upward reflecting resilient rent collections despite macroeconomic uncertainties — rising to just under $4 billion ($3.99 billion) in FY25 from $3.57 billion a year prior [F1]. This robust cash generation supports Realty Income's substantial dividend payouts as well as ongoing property investment activity.

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|---|

| 2025 | 5.7 | 1059 | 4.0 | +9.1% | +23.0% |

| 2024 | 5.3 | 861 | 3.6 | +29.2% | -1.3% |

| 2023 | 4.1 | 872 | 3.0 | +22.0% | +0.3% |

| 2022 | 3.3 | 869 | 2.6 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): OpInc, Capex, Buybacks, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($bn) | ROE% |

|---|---|---|

| 2025 | 2.9 | 2.7 |

| 2024 | 2.7 | 2.2 |

| 2023 | 2.1 | 2.6 |

| 2022 | 1.8 | 3.0 |

Source: SEC companyfacts cache [F1].

Note: Operating income and buyback data are not available from provided tags.

Strategic Growth Drivers: Geographic Expansion and Property Diversification

Realty Income executes growth through targeted geographic expansion and diversification across real estate segments consistent with its investment philosophy prioritizing stable, service-oriented properties with long-term leases [S1]. Since its initial U.K entry in early stages of the last decade, Realty Income has grown European holdings to represent approximately 19% of its annualized base rent by end-2025 versus roughly 14% a year earlier [S1]. This growth was heavily driven by acquisitions comprising about 60% of total acquisition volume in Europe during calendar year 2025.

In late-stage portfolio advancement, Realty Income further broadened its footprint with inaugural investments in Poland and the Netherlands plus a January-2026 launch into Mexico via joint venture partnerships with global institutional players [S1]. Such moves reduce geographic concentration risk while leveraging their proprietary net lease management expertise.

Beyond geography, the firm targets sectors showing resilient demand including retail franchises that eschew discretionary spending vulnerability—focusing on necessity-based services integrated with e-commerce strategies as part of their tenant selection criteria [S1].

Total acquisition spend for Q4 FY25 reached approximately $2.4 billion across properties, developments, unconsolidated entities, preferred equity stakes, and loans—all deployed around an initial average cash yield near seven percent [S8]. Given this metric is calculated pre-default risk adjustments it indicates attractive underwriting discipline amid competitive capital markets.

Capital Markets Activity: Convertible Debt Issuance Enhances Liquidity

Capital structure optimization remains central to Realty Income's strategy as it balances low-cost financing access with flexibility to fund expansion [S4][S5]. In early January-2026, the company raised $862.5 million through issuance of three-and-a-half percent Convertible Senior Notes due in January-2029 with an option that increased proceeds by an additional $112 million shortly thereafter [S16][S24].

These notes carry conversion terms entitling holders to shares at an approximately $69 per share conversion price initially but also feature make-whole provisions protecting investors against adverse redemption events [S24][S29]. Proceeds are earmarked primarily for share repurchase programs alongside funding property acquisitions and refinancing existing debt [S10][S11].

As of early January-2026, Realty Income reported liquidity totaling around $3.7 billion comprising cash ($0.8 billion), unsettled equity forwards ($713 million), plus unused portions of revolving credit facilities amounting to ~$2.2 billion—a substantial war chest relative to immediate investment opportunities [S5]. The company holds significant unsecured debt tranches maturing up through the mid-2040s offering duration diversity.

Dividend Policy & Capital Allocation: Sustaining Reliable Distributions

Consistent with its REIT status requiring distribution of most taxable income as dividends, Realty Income has steadily increased annual common stock dividends that totaled nearly $2.92 billion for FY25—up from $2.69 billion in FY24 [F1], supporting its widely recognized "Monthly Dividend Company" brand.

Though no explicit ROI guidance was found outside statutory filings, estimated ROE based on latest fiscal net income over shareholders’ equity stands around a modest ~2.7%, typical for asset-intensive REIT models focused more on stable yield than rapid earnings amplification [F1]. This underscores reliance on capital recycling through asset sales or joint ventures plus accretive acquisitions.

No comprehensive share repurchase details were disclosed within tags though SEC releases mentioned active share buyback programs funded partly by convertible debt proceeds aiming at EPS enhancement over time [S10][S11].

Risks: Tenant Credit & Market Volatility Amid Interest Rate Sensitivity

Realty Income acknowledges key risks chiefly involving tenant credit quality given reliance on single-tenant net leases; defaults could impair rental income significantly especially during economic downturns or sector-specific stress episodes [S1]. Market volatility may also impact property valuations and access or cost of capital.

Interest rate fluctuations represent an embedded challenge since higher rates elevate borrowing expenses directly affecting leverage strategies—though issuing fixed-coupon bonds during periods of historically low yields mitigates near-term refinancing risks somewhat [S4][S16]. Structural risks include environmental liabilities or regulatory changes impacting tax treatment relevant for REIT qualification.

Analysis: Outlook Anchored on Strategic Expansion & Yield Discipline

Absent explicit forward-looking financial guidance from recent earnings or SEC documents beyond pipeline commentary, watchpoints include progression of international diversification efforts particularly Mexico market penetration outcome; sustained investment yield metrics post-acquisition; stability of operating cash flows supporting resilient dividends; and evolving debt maturity profiles incorporating convertible securities.

The firm's strong liquidity position combined with disciplined selection criteria focusing on tenants insulated partly from ecommerce disruption suggests continued durable cash flow generation potential that can underpin incremental portfolio scaling assuming stable credit markets persists.

Despite relatively low ROE typical for diversified net lease REITs with substantial equity base deployments, Realty Income’s emphasis on long-dated leases coupled with geographic spread constitutes an explicit tradeoff favoring steady income streams over cyclical earnings volatility—a hallmark valued by dividend-focused investors but sensitive to interest rate tightening cycles.

Conclusion

Realty Income Corporation exemplifies a mature REIT employing multinational platform scale alongside rigorous underwriting to grow revenue near double-digit annual rates while safeguarding dividend consistency through robust cash flows supported by quality tenant relationships. Capital market activities including convertible note issuances and revolving credit facility access constitute vital lifelines enabling ongoing property acquisitions averaging attractive initial yields around seven percent—a key determinant for sustaining returns amid competitive real estate landscapes. The balance between expanding global footprint and managing tenant payment risks will be instrumental to preserving its market reputation as “The Monthly Dividend Company” going forward.

This analysis is for informational purposes only and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments