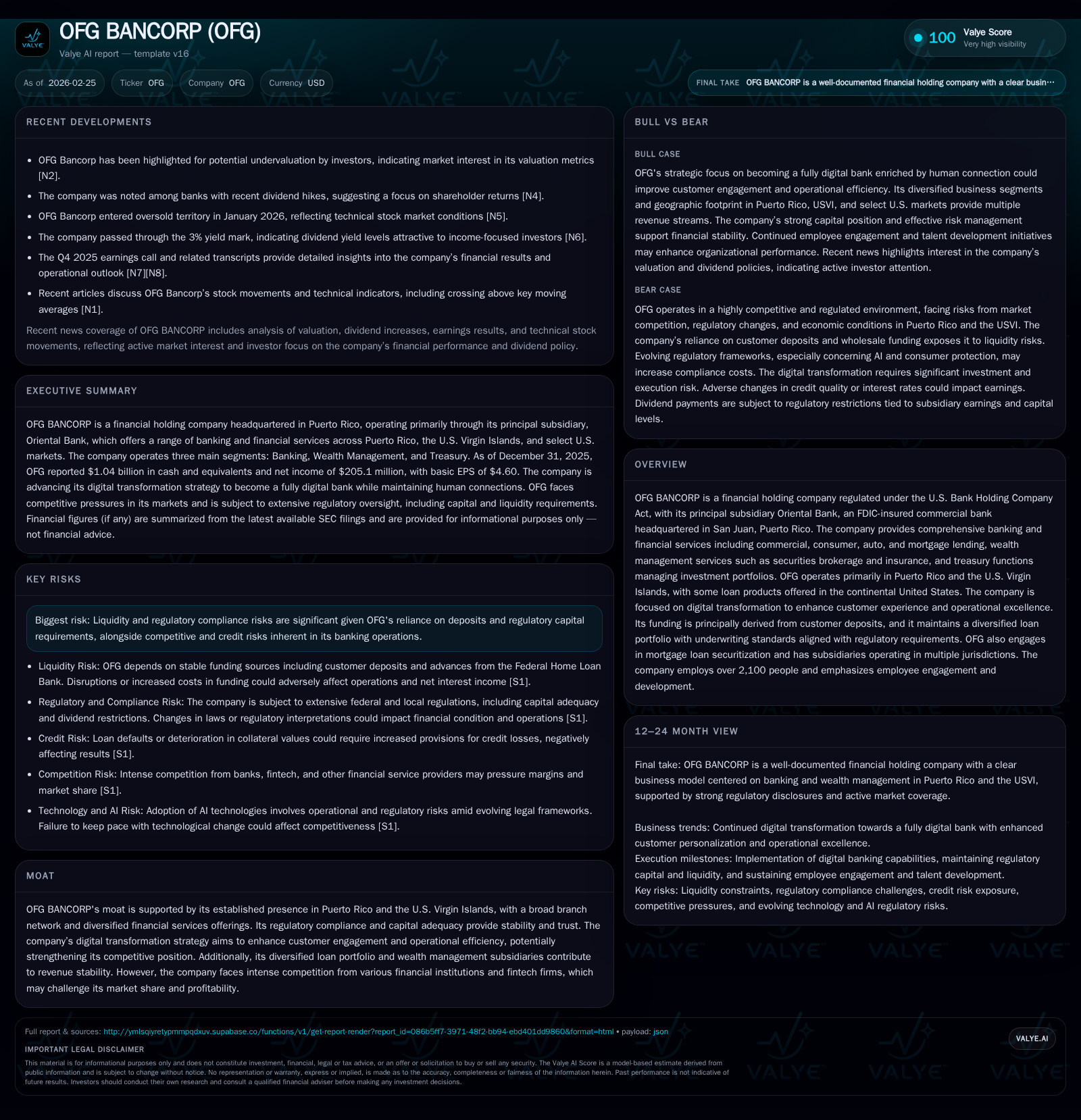

OFG Bancorp’s Financial Progress and Digital Transformation Shape Its Future

OFG Bancorp exhibits steady regional financial growth while executing a strategic shift toward an integrated digital banking model.

OFG Bancorp has demonstrated consistent profitability improvement with a net income growth rate around 3.5% annually and a robust return on equity near 15%. The company operates primarily in Puerto Rico and the U.S. Virgin Islands, combining traditional banking services with evolving wealth management and treasury functions. A pivotal element of its future trajectory is transitioning from a digital-first approach to offering an end-to-end digital banking experience that augments human advisory relationships. Capital discipline is evident through rising dividends and controlled capex, although challenges persist from regulatory requirements, localized economic risks, and intensifying competition. Market observers should focus on digital adoption rates, loan quality metrics, and deposit trends to assess operational momentum.

Steady Financial Gains Supported by Regional Focus

OFG Bancorp has shown consistent financial progress over recent years marked by stable net income growth averaging about 3.5% year-over-year from $166 million in FY2022 to $205 million in FY2025 [F1]. This steady increase emerges despite Puerto Rico’s challenging economic landscape characterized by lingering fiscal constraints and vulnerability to natural disasters [S1]. The company’s diversified loan portfolio—spanning commercial, consumer, auto, and mortgage loans—benefits from prudent underwriting aligned with regulatory mandates which underpin credit quality.

Operating cash flows (CFO) have exhibited somewhat more variability than net income but remain positive and substantial, reflecting strong core banking operations alongside cyclically adjusted investment spending [F1]. Capital expenditures have declined from nearly $31 million in FY2022 to under $19 million in FY2025 as management focuses on optimizing branch networks and digital infrastructure rather than heavy physical expansion [F1]. Shareholders’ equity increased steadily within this period reaching approximately $1.39 billion by end-FY2025 confirming retained earnings accumulation supporting balance sheet strength.

Historical performance (annual)

| FY | Rev | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 205 | 218 | 18 | +3.5% | |

| 2024 | 198 | 253 | 21 | +9.0% | |

| 2023 | 0 | 182 | 296 | 18 | +9.4% |

| 2022 | 0 | 166 | 164 | 31 |

Source: SEC companyfacts cache [F1].

Note: Some line items are omitted where multi-year comparability is limited in the structured SEC XBRL dataset; trend columns are shown only when comparable history exists.

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 52 | 199 | 14.8 |

| 2024 | 46 | 231 | 15.8 |

| 2023 | 41 | 278 | 15.2 |

| 2022 | 30 | 133 | 15.9 |

Source: SEC companyfacts cache [F1].

Compact display highlighting steady profitability growth with parallel operating cash flow trends and disciplined capex spending.

Digital Bank Transformation: From Digital-First to Fully Integrated

OFG's strategic pivot marks a clear departure from its earlier 'digital-first' posture toward becoming a fully integrated 'digital bank,' a concept wherein customers enjoy a comprehensive suite of banking activities digitally accessible without sacrificing human advisory touchpoints [S6]. This evolution is driven by deep customer insight initiatives leveraging advanced data analytics to fine-tune product personalization and deliver proactive financial coaching.

The bank employs an agile operating model emphasizing end-to-end customer journey alignment within all process redesign efforts—empowering both frontline staff with intelligence tools and enabling customers with intuitive interfaces suitable for complex decision-making scenarios [S6]. This synergy between technology-enabled automation and human connection aims to provide competitive differentiation through both operational excellence and emotional engagement grounded in trust.

Core Business Segments Reflect Diverse Revenue Streams

OFG segments its operations principally into Banking, Wealth Management, and Treasury divisions [S4][S5][S7]. The Banking segment dominates asset composition featuring broad offerings including middle-market commercial loans concentrated mainly in Puerto Rico but with expanding participations in mainland U.S. lower-middle market facilities conducted through OFG USA LLC based out of Charlotte, NC.

Mortgage banking activities comprise origination for portfolio retention or securitization into GNMA- or FNMA-backed securities providing flexibility between hold-and-sell strategies [S5][S7]. Rich underwriting standards reflect consumer-focused prudence governed by FHA/VA guidelines alongside conventional loan frameworks substantiating resilience under regulatory scrutiny.

Wealth Management capabilities are built around Oriental Financial Services for brokerage & advisory plus insurance sales via Oriental Insurance LLC complemented by captive reinsurance through OFG Reinsurance Ltd., which collectively stabilize fee revenue streams less correlated with credit cycles [S7][S23]. Treasury centers on managing investments primarily composed of U.S. government agency securities with significant holdings in mortgage-backed securities, balancing yield optimization against liquidity demands.

Competitive Dynamics within Puerto Rico and US Virgin Islands Markets

Operating chiefly within Puerto Rico’s economically volatile environment exposes OFG to heightened cyclical credit risk due to the island's history of protracted recession phases compounded by governmental fiscal challenges including restructuring processes commencing mid-2010s [S1]. The branch network also extends into the US Virgin Islands where similar natural disaster susceptibility constrains rapid growth but offers niche opportunities given fewer local competitors.

Competition arises not only from other established local banks subject to equivalent federal regulations but increasingly fintech firms leveraging nimble technology stacks that challenge traditional deposit gathering practices as well as consumer lending segments [S5][S9]. The reliance on federal disaster relief funds creates counterparty risk should delays or reductions occur affecting the broader customer base liquidity and repayment capacity significantly.

Credit concentration risks are amplified by localized economic dependencies especially given Puerto Rico’s infrastructural vulnerabilities which have necessitated ongoing capital infusion thus affecting borrower credit profiles indirectly [S1][S9]. These factors require ongoing vigilant portfolio monitoring alongside adaptive loan loss provisioning frameworks that integrate emerging climate transition risk insights.

Capital Efficiency: Returns, Cash Flow Trends, and Shareholder Distributions

OFG delivers solid capital returns boasting an approximate return on equity of 14.8% computed from its FY2025 net income over shareholders’ equity [$205 million / $1.39 billion] indicating efficient capital stewardship relative to peers [F1]. Operating cash flow remains robust despite modest declines attributable partly to normalization after elevated prior year working capital adjustments.

Capital expenditures have been judiciously curtailed aligning with strategic priorities favoring digital investments rather than branch expansion reflecting shifting customer engagement trends [F1]. Free cash flow calculated conservatively at roughly $199 million provides ample coverage for strengthening dividend payouts which have increased steadily from approximately $30 million in FY2022 to over $51 million last year affirming management commitment towards sustained shareholder remuneration [F1].

Notably, recent years show an absence of share repurchases suggesting capital allocation choices prioritize organic growth reinvestment alongside prudent balance sheet management rather than aggressive capital returns via buybacks.

Risks Rooted in Macro Conditions and Regulatory Landscape

The predominant macro risk vector for OFG centers on Puerto Rico’s uncertain economic rebound trajectory including fiscal policy volatility, prolonged recession fears, elevated unemployment rates, real estate market stressors impacting collateral valuations, all exacerbated by climate-induced natural disaster exposures such as earthquakes or hurricanes whose frequency may heighten per climate change models [S1][S9].

Liquidity risk manifests through the company’s pronounced dependency on core deposits which constitute the main funding source; competitive pressure compels periodic increases in interest rates paid to depositors driving funding cost upward potentially compressing net interest margins particularly if deposit flight occurs or if higher-cost wholesale funding substitutes are required [S11][S15].

Regulatory compliance complexity multiplies given dual supervision—Federal Reserve Board under the BHC Act coupled with FDIC oversight at bank level—and multijurisdictional consumer protection laws enforced vigorously post-Dodd-Frank Act amendments with emerging AI governance frameworks introducing new operational uncertainties around technology deployments reliant on third-party vendors [S9][S21].[N6]

Credit risk exposure remains acute due to concentration in economically sensitive sectors within Puerto Rico requiring ongoing vigilance particularly regarding loan modification needs arising after disaster events or shifts in borrower behaviors amid social factors influencing indebtedness attitudes [S21][S26].

Outlook: Growth Catalysts and Operational Priorities Ahead

Recent management commentary underscores progressing implementation milestones around the comprehensive digital banking platform rollout aiming not only at improving transactional convenience but augmenting cross-sell capability through intelligent product bundling informed by behavioral analytics [N1][N2]. Expansion beyond island borders gains traction via participation interests in middle-market loans originated mainly across select continental U.S. regions leveraging OFG USA LLC infrastructure showcasing diversification ambitions without wholesale geographic relocation risks.

Product mix evolution will focus on integrating mortgage products seamlessly within new digital ecosystems while enhancing wealth management services tailored for individual client wealth progression supported by advisory service modernization [N6]. These initiatives do not accompany explicit numeric guidance but represent directional operational thrusts validated during quarterly updates.

Observing incremental gains in deposit inflows amid ongoing rate adjustments alongside trending improvements in cost-to-income ratios will be informative proxies gauging efficiency gains.

Key Metrics to Watch in Upcoming Earnings

Analysts should monitor several critical metrics to assess OFG’s momentum including trends in loan delinquency rates signaling credit quality shifts particularly related to regional economic stressors; net interest margin trajectory responding sensitively to competitive deposit pricing; cost-income ratio developments reflecting effectiveness of ongoing digitization; pace of digital adoption quantified via active user growth or transaction volumes paralleling branch foot traffic declines; deposit base stability; provision expense levels versus historical baselines revealing emerging loss trends; along with segment-level profitability contributions confirming strategic segment priorities execution.

These indicators combined will illuminate whether OFG Bancorp successfully balances its heritage of trusted human connections with its ambition for intelligent operational excellence fueled by digital innovation adapting adeptly amid multifaceted regional challenges.

This analysis is based solely on publicly available information including SEC filings ([F1], [S#]) and recent news reports ([N#]) without any projection or financial advice obligation. Readers should consider company disclosures directly when evaluating any investment considerations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments