Okmin Resources’ Transition: From Oil Ventures to Craft Brewery Acquisition Amid Liquidity Constraints

Okmin Resources faces critical liquidity and operational hurdles as it pivots from oil and gas interests towards the craft brewery sector through a pending merger.

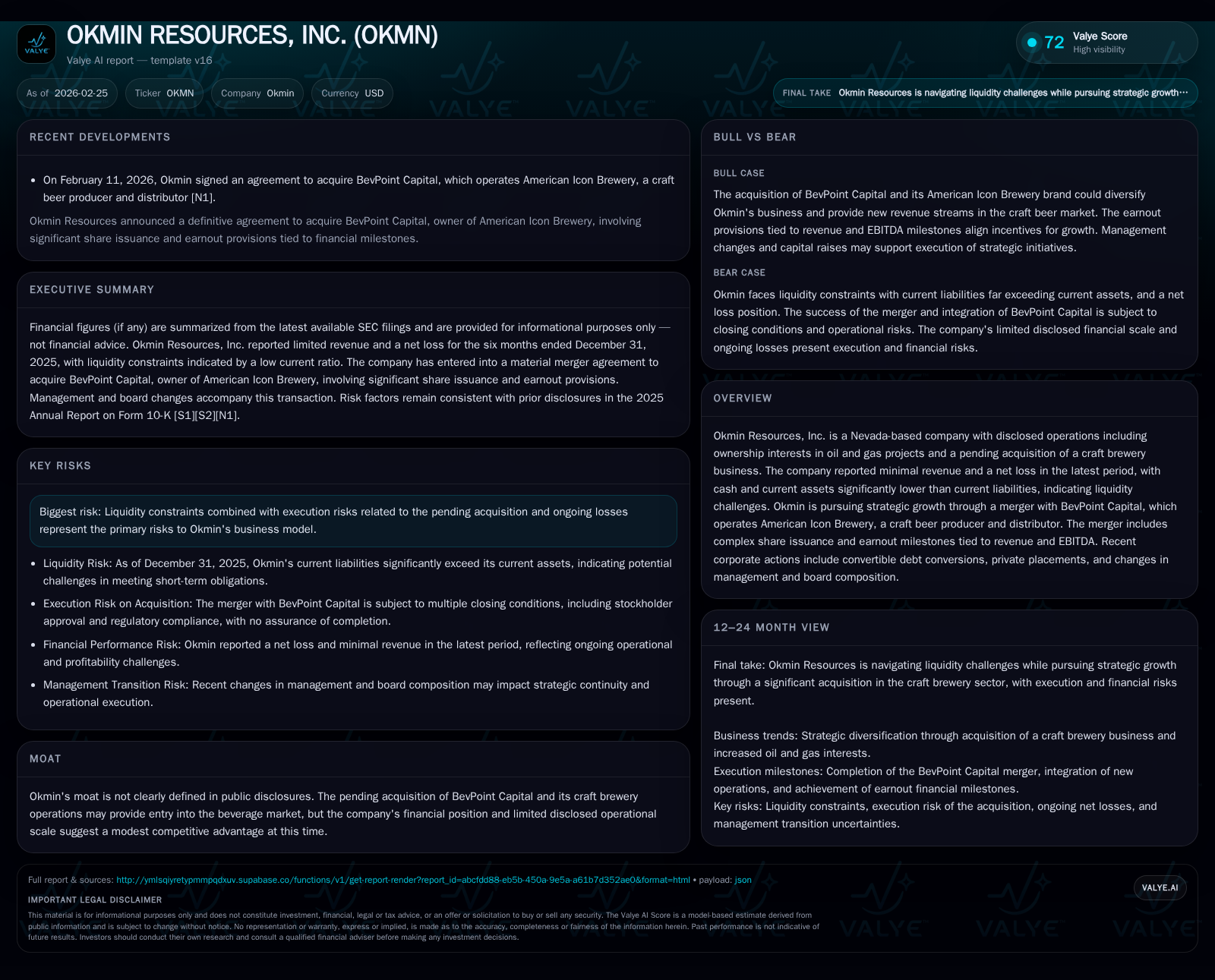

Okmin Resources, Inc. has seen steadily deteriorating financial performance with shrinking revenues and persistent losses over recent years, compounded by severe liquidity challenges. The company is undertaking a strategic pivot via a merger with BevPoint Capital to enter the craft beer market, involving complex share issuances and earnout milestones tied to future revenue and EBITDA targets. While this represents a potential growth catalyst, execution risks are substantial given Okmin's current financial fragility and limited operational scale.

Historical Financial Performance

Okmin Resources’ financial trajectory over the past several years reflects a company grappling with declining revenues and sustained losses. Revenue decreased from $114,098 in FY2023 to $22,180 in FY2025 — a steep drop of approximately 48% year-over-year [F1]. Operating income (loss) remained negative throughout this period but showed some improvement in FY2025 with an operating loss of -$581,551 compared to -$862,708 the prior year. Net income followed a similar trend, registering -$597,167 in FY2025 versus -$873,214 in FY2024 [F1].

Operating cash flow (CFO), another critical metric to gauge underlying business health, also stayed negative but improved by over 70% YOY to a deficit of -$36,793 in FY2025. However, Okmin’s balance sheet paints a stark liquidity picture. As of December 31, 2025, the company had only $705 in cash and cash equivalents against current liabilities exceeding $656K — resulting in a current ratio effectively at zero [F1]. This underlines severe short-term funding challenges threatening operational sustainability.

Historical performance (annual)

| FY | Rev ($) | Net ($) | CFO ($) | OpInc ($) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 22180 | -597167 | -36793 | -581551 | -47.9% | +31.6% |

| 2024 | 42543 | -873214 | -126035 | -862708 | -62.7% | -65.1% |

| 2023 | 114098 | -529014 | -393254 | -531387 | +24.2% | -125.7% |

| 2022 | 91838 | -234369 | -183198 | -234369 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex, Div, Buybacks, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 96.2 |

| 2024 | 524.3 |

| 2023 | -92.9 |

| 2022 | -38.3 |

Source: SEC companyfacts cache [F1].

Note: Capital expenditures (Capex), dividends paid and share buybacks are not available from provided tags.

Strategic Pivot: The BevPoint Capital Acquisition

In early 2026 Okmin signed an agreement to acquire BevPoint Capital LP and its majority-owned subsidiary American Icon Brewery (AIB), signaling a fundamental shift from natural resource assets towards consumer beverage production [N1][S3][S17]. This merger will see BevPoint merged into Okmin's wholly owned subsidiary Merger Sub which survives as BEVPT Operations Inc., thus repositioning Okmin as a craft brewery operator and distributor.

The closing is targeted by March 31, 2026 subject to standard approvals including stockholder consent and regulatory compliance [S18]. Upon closing BevPoint interest holders will receive about 220 million shares representing roughly 55.6% of post-closing outstanding common stock excluding earnouts and convertible note conversions [S17]. Additional milestone-based earnouts could issue up to approximately 300 million shares contingent upon consolidated revenue milestones ($10M and $20M) and EBITDA targets ($1M and $2M) [S17]. These milestones will be audited independently.

This transaction represents a clear growth outlook pivot leveraging opportunities within the craft brewing sector—a market characterized by niche branding and regional distribution—but entails significant integration execution risk given Okmin’s historical operational scale [N1][S17].

Prior Business Operations: Oil & Gas Interests

Prior to this strategic shift Okmin’s core operations centered on oil and gas assets including ownership interests in the Pushmataha Gas Field increased from 50% to 95% via an asset exchange transaction with Blackrock Energy LLC in August 2025 [S15][S16]. Earlier stakes included participation in the Blackrock Joint Venture.

Despite these upstream energy holdings Okmin generated minimal revenues relative to its operating losses indicating difficulty scaling or monetizing these assets efficiently [F1][S1][S6]. The company also converted outstanding convertible debt into equity during late fiscal periods reflecting constrained financing alternatives [S11][S12].

Capital Structure & Liquidity Challenges

Okmin’s liquidity profile remains highly constrained with cash balances ($705 at end-December 2025) negligible compared to current liabilities (~$656K), producing a critically low current ratio near zero [F1][S2]. To support operations and fund the acquisition it issued convertible promissory notes totaling over $530K primarily to management including incoming CEO Chris Sellers at conversion prices near $0.04 per share along with equity issuances around $0.03–$0.04 per share [S12][S14].

Stockholders’ equity turned negative at approximately -$621K by FY25 end reflecting accumulated deficits [F1]. No dividends or share buyback programs have been disclosed amid this capital preservation focus [S17]. Risk disclosures underscore ongoing losses and completion uncertainties around the BevPoint deal as material investor considerations [S4][S7].

Industry Context & Competitive Positioning

Historically lacking scale or defensible assets within upstream oil/gas exploration segments , Okmin’s pivot into craft brewing introduces exposure to an industry driven by brand differentiation and regional loyalty.

American Icon Brewery operates both brewery production and brewpubs distributing over a dozen craft beers—a footprint that may provide moderate barriers if post-merger growth initiatives succeed [N1][S17]. However margin pressures from commodity-based raw materials (e.g., barley/hops) demand efficient operations.

Successful execution will require managing production capacity expansions while controlling costs amidst Okmin’s fragile balance sheet.

What To Watch Going Forward

- Completion of the BevPoint merger by March-end deadline including all regulatory approvals.

- Achievement of earnout milestones tied to revenue ($10M/$20M) and EBITDA ($1M/$2M).

- Cash burn rates versus working capital availability given tight liquidity post-closing.

- Management’s success integrating beverage operations alongside legacy energy assets.

- Potential for further equity or debt raises impacting shareholder dilution.

- Operational KPIs such as brewery volume output and geographic expansion plans if disclosed.

Summary

Okmin Resources is at an inflection point transitioning away from modest upstream energy asset positions marked by chronic operating losses toward consumer beverage manufacturing through its acquisition of BevPoint Capital. This strategic redirection offers growth potential but carries pronounced financial risks due to near-zero liquidity buffers and significant structural changes underway.

Success depends on timely merger completion coupled with scaling American Icon Brewery’s footprint sufficiently to meet milestone-driven equity earnouts that will reshape shareholder composition significantly. Persistent net losses alongside tight cash positions highlight the delicate balancing act management faces maintaining solvency amid this transformation.

Investors should monitor milestone achievements closely as indicators whether this pivot unlocks value or amplifies risk profiles for Okmin stakeholders.

Disclaimer: This report is based exclusively on publicly available SEC filings and news disclosures as of February 25, 2026 ([N1], [S1]-[S19], [F1]). It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments