OLB Group Advances Integrated Merchant Services Ecosystem Despite Liquidity Strains

The latest quarterly update highlights OLB Group’s ongoing operational integration across merchant service platforms while revealing liquidity challenges and regulatory risks.

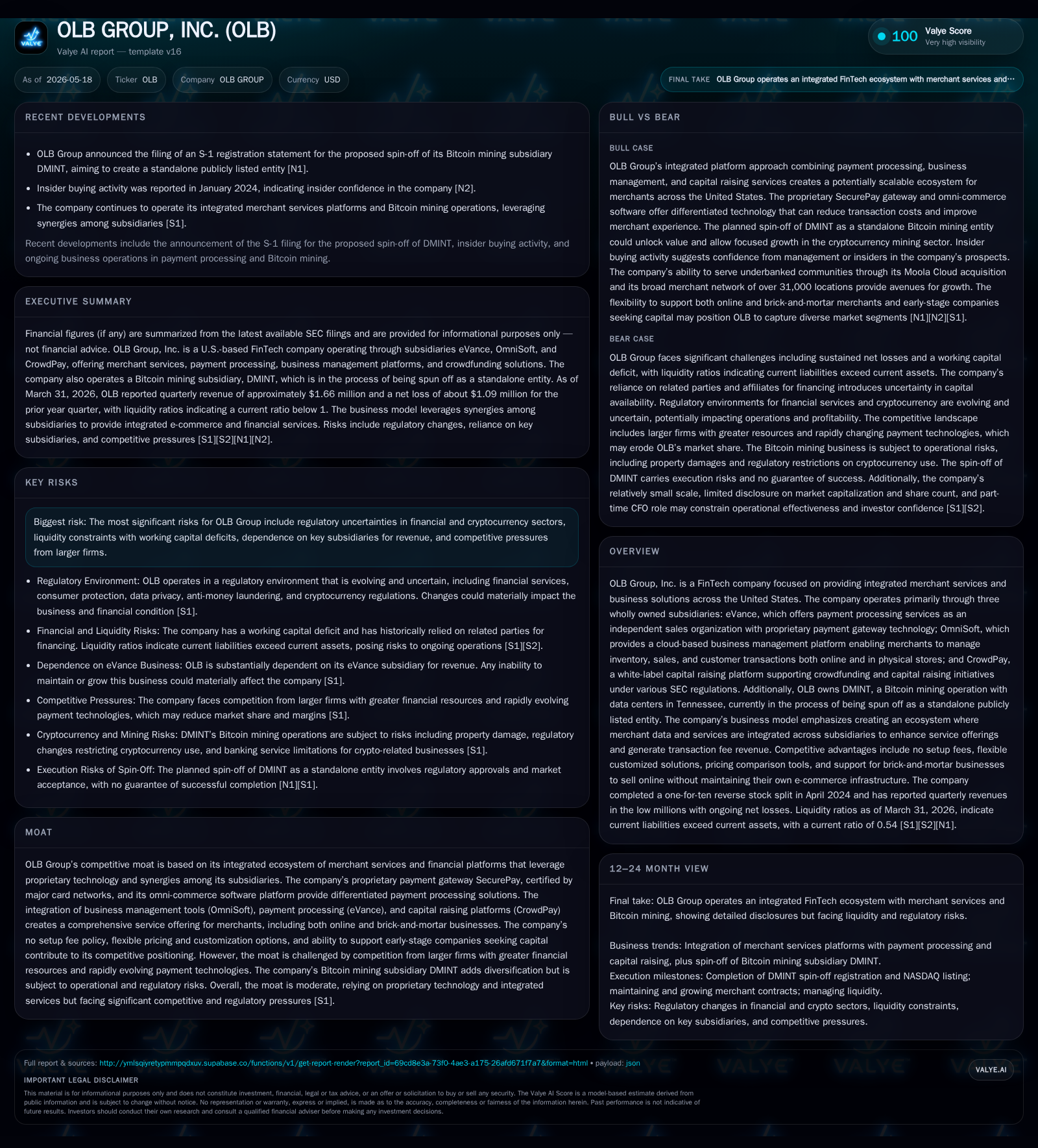

OLB Group’s 2026 Q1 filing shows continued execution of its integrated fintech strategy through its subsidiaries offering payment processing, business management software, and crowdfunding platforms. The company operates an ecosystem designed to synergistically serve online and brick-and-mortar merchants, leveraging proprietary payment gateway technology and compliance with evolving SEC crowdfunding regulations. However, OLB faces significant liquidity constraints evidenced by a working capital deficit and tight current ratio, alongside exposure to complex regulatory demands and fierce competition from larger, better-capitalized firms. The upcoming DMINT Bitcoin mining spinoff represents a strategic milestone to unlock value. Near-term growth depends on scaling its crowdfunding platform and deepening merchant service penetration amid operational and regulatory headwinds.

Latest Quarterly Operating Update: What Changed

In its May 18, 2026, Form 10-Q filing [S2], OLB Group disclosed that it did not file all Interactive Data Files timely pursuant to Regulation S-T requirements over the last twelve months. While this indicates a lapse in compliance processes for XBRL filings — a nondirect operating issue — the company affirmed the continuation of normal operations without major disruptions or material adverse changes reported. No new material event filings were made recently. This steady operating posture amid procedural compliance gaps reflects that OLB remains focused on executing its merchant service integration strategy during this period of fiscal pressure.

Business Model and Product Suite Integration

OLB Group generates revenue by delivering an integrated suite of fintech services through four principal wholly-owned subsidiaries detailed in its latest annual filing [S1]

- eVance acts as an independent sales organization providing electronic payment processing services using its proprietary payment gateway technology called SecurePay. This gateway is certified by major card networks enhancing transaction reliability for merchants.

- OmniSoft offers a cloud-based omni-commerce business management platform enabling merchants — whether online or brick-and-mortar — to manage inventory, sales tracking, transaction processing, loyalty programs including QR code payments (patent-pending), shipping coordination through third parties, and interactive sales analytics accessible via mobile or desktop devices.

- CrowdPay operates a white-label capital raising platform targeting small to midsize businesses seeking to raise funds under multiple SEC-regulated exemptions such as Regulation CF (raised cap recently increased from $1.07M to $5M), Regulation D Rule 506(b) & (c), and Regulation A+. CrowdPay facilitates broker-dealers' campaign hosting on their websites alongside ancillary compliance services like background checks and AML/KYC enforcement.

- DMINT, engaged in Bitcoin mining within Tennessee data centers, is undergoing spin-off plans intended to create a separately listed entity specializing in cryptocurrency mining operations.

These subsidiaries share merchant data within a centralized backend ecosystem allowing seamless cross-utilization across platforms—for example, merchants onboarded via eVance can process payments on CrowdPay’s platform or use OmniSoft's retail management tools powered by shared transaction data [S18]. This tightly coupled setup aims to reduce switching costs for clients by bundling payments processing alongside backend inventory management and access to startup fundraising.

Revenue is primarily fee-based with transaction fees charged per processed payment or capital raise event. Pricing strategies emphasize flexibility including no setup fees paired with volume-sensitive price comparisons allowing partners control over promotional rates [S23]. Such product bundling combined with customizability increases client stickiness within OLB's ecosystem.

Industry Positioning and Competitive Pressures

Operating within the fragmented U.S. FinTech merchant services market places OLB among numerous players ranging from dominant incumbents like Square (Block), Stripe, PayPal's Braintree division to emerging specialized firms. Larger competitors benefit from robust balance sheets enabling substantial R&D spend, broad partner networks with acquiring banks, extensive PCI compliance programs, and well-established brand trust.

OLB's competitive positioning leans on nimbleness afforded by personalized pricing models and customized software integrations which appeal distinctively to smaller merchants frequently underserved by rigid legacy players [S1]. However, scale disadvantages limit OLB's ability to absorb regulatory compliance costs or compete aggressively on interchange fee economics that benefit larger providers who fall under Federal Reserve caps for debit interchange under Dodd-Frank [S20].

CFPB scrutiny under Dodd-Frank regulation impacts processing volumes indirectly through consumer protections affecting client institutions. The interplay of evolving federal regulations introduces uncertainty requiring investment in legal/compliance expertise that may be burdensome for a lean player like OLB.

Technology Infrastructure and Product Quality

OLB's infrastructure blends proprietary payment gateway technology (SecurePay) with SaaS offerings housed in cloud architectures managed across U.S.-based data centers [S9]. The omni-commerce technology centers on integrating POS functionality catering both offline "brick-and-mortar" locations as well as online storefronts with unified inventory/sales tracking capabilities.

Notably, the patent-pending transferable QR code innovation positions OmniSoft uniquely amidst increasing consumer preference for mobile wallet-based payments—a growing vector for differentiation if successfully commercialized [S27].

Technical reliability remains paramount given that any network downtime directly impairs merchant cash flows risking churn [S21]. Thus maintaining infrastructure resilience while upgrading feature sets demands sustained R&D capital allocations despite ongoing liquidity challenges reducing available investment bandwidth.

Regulatory Environment and Risk Factors

The regulatory landscape enveloping OLB comprises multilayered U.S. federal/state financial laws plus SEC mandates particularly regulating CrowdPay's crowdfunding activity [S5], [S16], [S21]. Compliance involves navigating complex frameworks—CFPB oversight of consumer financial products affects some customer institutions indirectly; evolving Know Your Customer / Anti-Money Laundering rules raise operational overhead; varying state money transmitter licensing requirements further complicate footprint expansion strategies.

In the cryptocurrency domain housing DMINT's mining operations lie additional risks involving regulatory uncertainty around digital assets usage legality; banking restrictions imposed on crypto-related enterprises; potential policy shifts curtailing Bitcoin activities domestically or abroad [S16]

The current ratio reported in Q1 2026 stands below unity at 0.54 reflecting short-term coverage insufficiency juxtaposed against approximately $29k cash reserves reported at March-end 2025 [F1]. Historically CEO Ronny Yakov has provided short-term financing assistance but future support lacks certainty [S16].

Drivers of Growth and Expansion Potential

Several growth catalysts exist within OLB’s core markets:

- The reformed SEC crowdfunding environment enabling companies to raise up to $5 million under Regulation CF expands addressable market demand for CrowdPay’s platform—critical given only about 50 other registered competitors currently exist offering similar services [S25].

- Enhanced data analytics capabilities through OmniSoft can deepen merchant engagement fostering upsell opportunities around ancillary services like loyalty programs or integrated shipping logistics.

- Expansion efforts at eVance targeting new merchant acquisition via SecurePay development underpin incremental payments volume growth reinforcing recurring fee streams.

- The upcoming public separation of DMINT represents a potential value crystallization event unlocking investor interest specifically focused on regulated cryptocurrency infrastructure plays versus broader fintech portfolios [S24].

Operational synergy potential remains meaningful provided backend data consolidation enables seamless workflows across subscriptions; multi-channel payments acceptance; real-time compliance validations; effectively binding clients into the ecosystem.

Risks and Constraints to Scaling

Chief among concerns restraining scale advancement are:

- Persistent cash flow deficits curtail investments in critical technology upgrades needed to fend off encroaching competitor innovations especially around advanced fraud prevention algorithms or scaling secure payment gateways efficiently.

- Complexity inherent in aligning disparate subsidiary platforms behind common UX frameworks risks customer experience fragmentation undermining retention.

- Competitive price compression reduces margin available to fund customer acquisition efforts underpinning growth economies-of-scale.

- Regulatory environment volatility could impose costly operational adjustments or curtail permissible product features particularly given ambiguous crypto asset legal regimes affecting DMINT outlook [S20],[S21].

- Infrastructure reliability lapses risk sudden transactional outages potentially driving client attrition detrimental given thin overall revenue base reliant heavily on eVance transaction fees alone [S18],[S21].

Upcoming Milestones and Strategic Focus

Near-term execution priorities center on:

- Advancing DMINT’s IPO/spin-off process projected post Q2/Q3 calendar 2026 aiming to enhance strategic focus while isolating crypto-related risk profiles thereby appealing distinctly to capital markets interested explicitly in blockchain/Bitcoin exposure [N/A from recent filings but consistent prior disclosures S24,S26].

- Enhancing CrowdPay usability aligning with SEC regulatory updates facilitating smoother onboarding for broker-dealers managing multiple concurrent capital raises simultaneously.

- Strengthening OmniSoft platform features notably around patented QR code deployment expanding low-touch contactless commerce options tailored toward small/mid-size retail channels.

- Incrementally building eVance merchant base leveraging integrations linking payment authorization directly into underwriting workflows with acquiring banks improving transactable volume metrics significantly.

Concise Financial Overview

As of March 31, 2026 per Q1 filing data combined with SEC companyfacts snapshot metrics: current assets total approximately $3.7 million contrasted against current liabilities around $6.9 million yielding a current ratio near 0.54 indicating a liquidity shortfall [F1],[S2]. Cash & equivalents hover near $29 thousand reflecting constrained immediate cash buffer [F1]. Last publicly available total debt was roughly $406k reported end FY 2022 suggesting moderate leverage though updated figures are unreported given limited recent disclosures [F1].

Prior full-year results exhibited significant net losses exceeding $5.8 million accompanied by heavy operating expenses reducing free cash flows restricting reinvestment capacity into growth initiatives [F1],[S16].

Management contends operational continuity is viable through conservative expense monitoring combined with anticipated eventual improvements catalyzed by synergy realization within their integrated subsidiary model [S16].

This analysis synthesizes detailed SEC filings as of mid-2026 portraying OLB Group as an ambitious integrated FinTech platform addressing diverse merchant needs across payments processing, e-commerce management, fundraising facilitation, and cryptocurrency mining operations. While product innovation coupled with an ecosystem approach strengthens competitive differentiation against large scale rivals constrained primarily by size-dependent pricing power disparities liquidity limitations introduce tangible operational execution risks alongside layered regulatory complexities necessitating careful ongoing monitoring.

Financial position in context

Current assets of $3.7 million and current liabilities of $6.9 million imply a current ratio near 0.54x for 2026-03-31 [F1]

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments