ORIENTAL RISE HOLDINGS Limits Margin Erosion Amid Capital Structure Reorganization

Q4 2025 results reveal shrinking revenue and profitability challenges in China's tea market despite robust liquidity and strategic equity maneuvers.

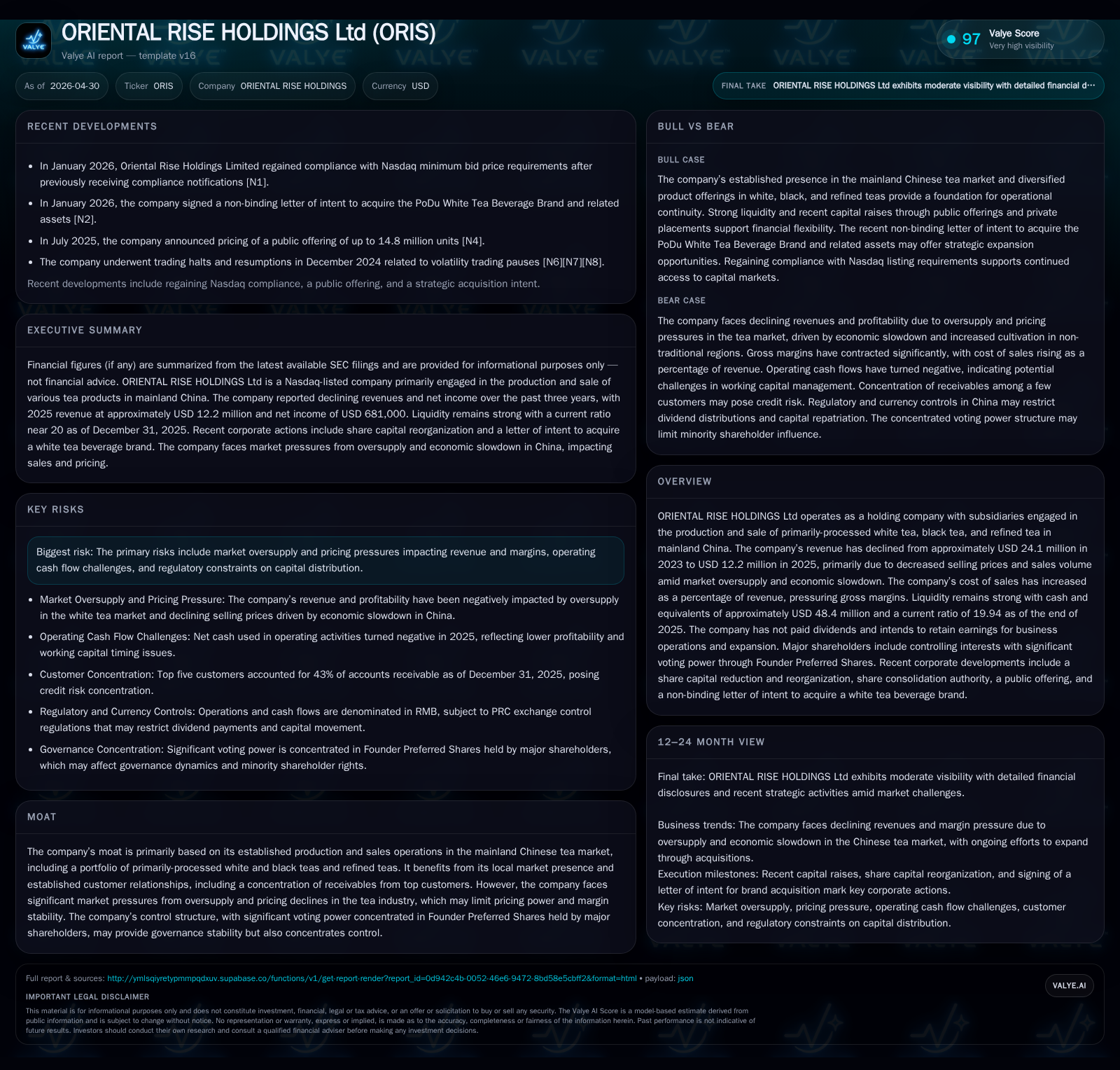

ORIENTAL RISE HOLDINGS Ltd reported a further decline in revenue to $12.2 million in fiscal 2025, down 18.6% from 2024, driven by reduced sales volumes and pricing pressure amid market oversupply. Gross profit collapsed by 66.6%, reflecting an intensified margin squeeze largely from the primarily-processed tea segment, although refined tea sales offered limited offset. Recent corporate actions include a significant reduction and reorganization of share capital alongside the establishment of high-vote Founder Preferred Shares consolidating control. Liquidity remains a bright spot, with cash reserves standing at $48.4 million and a strong current ratio nearing 20x, providing flexibility despite operational headwinds.

Recent Operating Update

ORIENTAL RISE HOLDINGS Ltd's latest quarterly SEC filing dated April 15, 2026 ([S2]) reports critical corporate restructuring developments following its fiscal year-end financial disclosures. At the Extraordinary General Meeting conducted on April 7, 2026, shareholders approved a notable share capital reduction and reorganization that restructures the company's authorized share capital from approximately $5 million divided into ~313 million shares with par value $0.016 each down to $5 million divided into an expansive pool of up to 500 billion shares at a drastically reduced par value of $0.00001 each. This maneuver substantially increases authorized shares availability for future financing flexibility while potentially diluting per-share accounting value.

Concurrently, the Board was empowered to consolidate ordinary shares within a broad range (1-for-10 to 1-for-200) over the ensuing six months, underscoring management’s discretion in optimizing share structure amidst ongoing operational challenges.

This episode closely follows November 2025 approval of Founder Preferred Shares issuance ([S3]), which carry extraordinary voting weight—1000 votes per share—granting controlling shareholder Chun Sun Wong, through his vehicle Plentiful Thriving (BVI) Limited, near-total governance influence despite comparatively modest equity stake holdings by ordinary shareholders ([S1]). These governance adjustments suggest a dual focus on preserving strategic control while positioning the company for potential equity market or financing activities ahead.

Business Model

Oriental Rise Holdings operates principally through subsidiaries engaged in cultivation, processing, and sales of primarily-processed teas (white and black) alongside refined tea products targeted mainly at mainland China's consumer segments ([S1]). Revenue is generated by selling bulk primarily-processed fresh leaves as well as packaged refined teas through established distribution relationships concentrated among top customers who collectively represent more than 40% of receivables ([S12]). Pricing is sensitive due to highly competitive domestic supply dynamics with expanded non-traditional planting outside core Fujian Province including Sichuan and Guizhou provinces intensifying supply pressure and depressing average selling prices notably for white tea—from about USD41/kg down to USD23/kg between 2023 and 2024 ([S1]).

Margins are under strain as cost of sales has increased relative to declining revenues despite stable absolute cost levels ([S1]). Volume declines coupled with persistent oversupply have impinged on both unit economics and margin stability highlighting limited pricing power often characteristic of commodity-style agricultural products where large-scale producers dilute market scarcity premiums.

Operational expenses primarily comprise plantation maintenance costs, processing labor/material costs along with administrative overheads which unexpectedly swelled by over 46% year-on-year in fiscal 2025 exacerbating profitability erosion ([S13]). This structural oversupply depresses prices broadly across premium grades undermining producer margins.

Oriental Rise’s entrenched presence in Fujian province offers geographic advantage but suffers diminished differentiation as similarly scaled producers ramp up output leveraging mechanization innovations and improved agronomy techniques accelerating regional yield expansions — a known vector compressing average selling prices in commodity segments.

Customer concentration risk is notable with reliance on a handful of major buyers representing almost half receivables exposure ([S12]) thereby concentrating credit risk yet reflecting longstanding trade relationships that provide revenue predictability if volumes recover.

Governance concentration via super-voting Founder Preferred Shares backing founder leadership enforces strategic continuity but limits broader shareholder influence creating tension between stability versus minority investor dynamics ([S3],[S1]).

Growth Drivers

Structural demand for premium Chinese teas endures driven by rising middle class health consciousness domestically and growing interest overseas though these trends face headwinds from cyclical economic slowdown evidenced since early-2020s which compresses out-of-home consumption frequencies impacting bulk sales.

Refined tea segment revenue growth partly offsets declines in primarily-processed products indicating potential margin improvement opportunities through value-added branding or downstream packaged goods development leveraging quality certifications or geographic indications ([S1]).

Capital structure maneuvers are geared towards enhancing balance-sheet agility enabling possible acquisitions or operational investments intended to capture niche premiumization trends within boutique tea markets or export channels; however scale limitations remain a constraint absent material upstream integration or downstream branded product expansion (analysis).

Risks / Watchpoints / Growth Constraints

Oversupply-induced price deflation poses the primary threat constraining top-line recovery presently reflected in stark sales declines (37.8% drop between 2023–24; -18.6% between ‘24–‘25) alongside deteriorating gross profit margins plunging nearly two-thirds year-over-year ([S1],[F1]).

Rising administrative expenses despite falling revenues could signal operational inefficiencies or investment misalignment warranting scrutiny as compounding margin pressure risks liquidity deterioration absent offsetting capex discipline or cost rationalization initiatives ([S13]).

Operating cash flow turned negative in fiscal 2025 (-$583K), reversing previous positive trends due largely to profit squeeze combined with working capital timing shifts thereby raising questions about near-term self-financing capacity prior to realizing strategic structural benefits from newly authorized share issuance capability ([S6],[F1]).

External regulatory constraints restrict PRC subsidiary dividend repatriation capabilities affecting inbound cash remittances essential for reported consolidated liquidity deployment potentially impacting capital return policies or external funding needs ([S4],[S17]).

Founder Preferred Shares wield disproportionate voting power restricting shareholder democracy introducing governance risks especially if minority interests desire strategic pivots divergent from controlling stakeholder priorities ([S3],[S19]).

What to Watch Next

Key milestones include any execution announcements related to exercise of board-authorized share consolidation programs expected within next half-year potentially affecting share count structure and liquidity profile ([S2]).

Monitoring revenue trajectory Q1/Q2 FY2026 will be critical given recent continued margin deterioration; stabilization signals or early signs of volume/pricing recovery would signify turnaround potential amid structural oversupply correction or market demand renewal ([S6],[F1]).

Tracking changes in administrative cost trajectory following significant expense increase may reveal management’s ability to adapt operating model more efficiently against shrinking top-line backdrop ([S13]).

Revisions or clarifications around dividend policy especially linked to PRC regulatory environment will provide insight into capital allocation priorities balancing reinvestment versus shareholder returns ([S4],[S17]).

Updates on customer concentration shifts either via new contract wins or losses will illuminate progress on diversifying sales mix reducing credit/concentration risk exposure inherently high today ([S12]).

Any management commentary on expanding refined tea portfolio efforts leveraging higher-margin products could signal long-term strategic inflection aimed at value migration away from commoditized primary processing segment ([S1] analysis).

Financial Profile Snapshot (Year ended December 31, 2025) [F1]

Latest financial snapshot

Liquidity indicators remain robust with a current ratio of 19.94 as of December 31, 2025, reflecting conservative balance sheet management despite earnings softness allowing continued investment optionality though operating losses underline margin repair necessities going forward.

This analysis is based exclusively on publicly available information including ORIENTAL RISE HOLDINGS Ltd’s recent SEC filings as detailed by dates up to April 30, 2026. It summarizes observed financial performance drivers without offering investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments