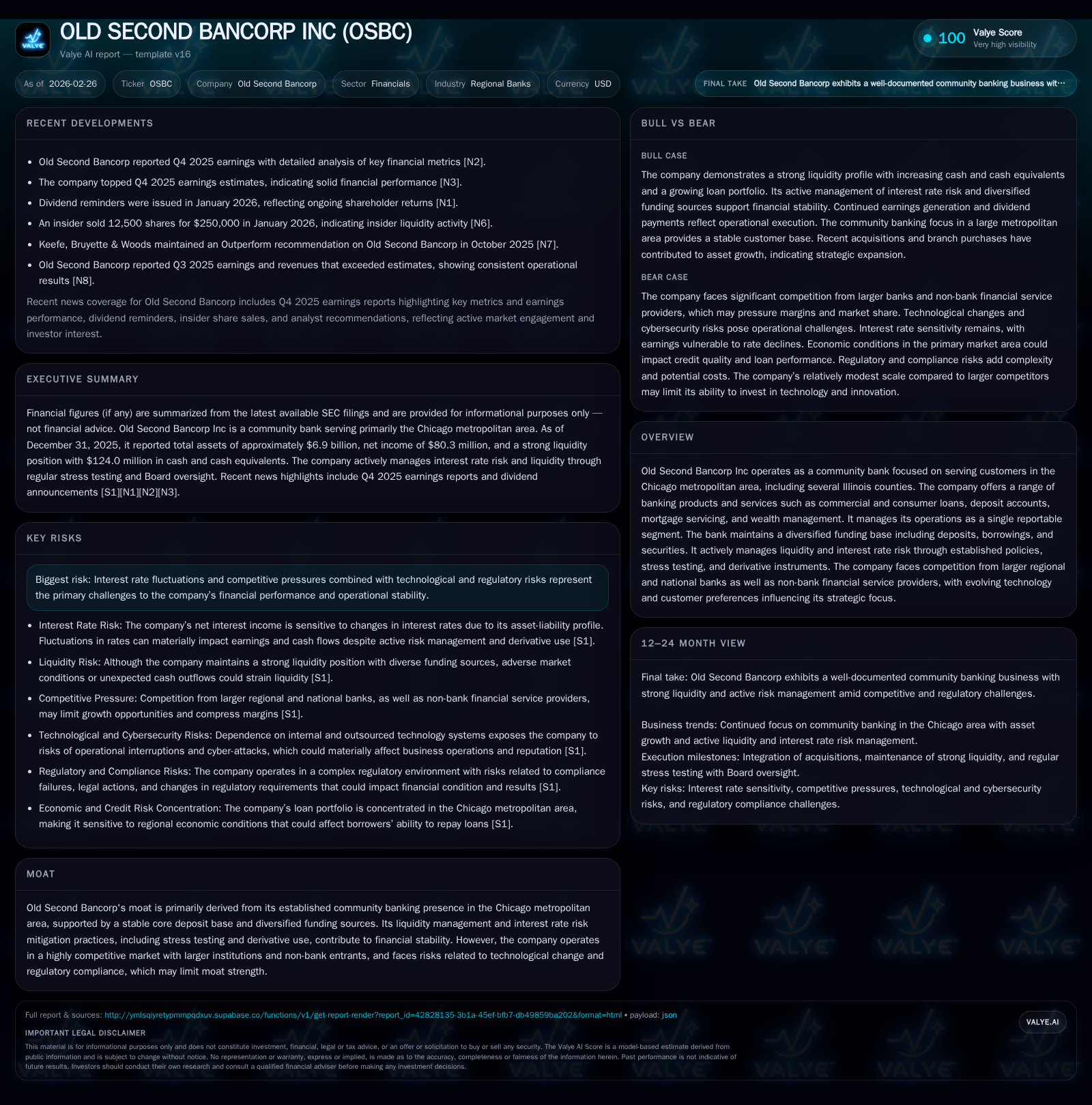

Old Second Bancorp’s Stabilizing Growth and Capital Strategies Underpin Chicago-Area Franchise

Old Second Bancorp balances local market challenges with prudent capital and liquidity management to sustain its community banking niche.

Old Second Bancorp operates a focused community bank franchise in the Chicago suburbs, delivering steady albeit modest growth supported by a stable loan portfolio concentration and a reliable core deposit base. The bank’s capital structure has evolved through strategic equity increases related to acquisitions and increased borrowings from the Federal Home Loan Bank, enhancing leverage capacity while maintaining regulatory compliance. Robust liquidity management is driven by diversified funding sources, sizeable securities holdings, and regular stress testing, underpinning its resilience amid competitive and economic headwinds. Shareholder returns reflect consistent dividends and a recently authorized $43.9 million repurchase program, signaling capital discipline alongside growth vigilance.

Legacy Performance and Drivers: Loan Portfolio, Deposits, and Income Trends

Old Second Bancorp’s financial trajectory over recent fiscal years reveals a steady build-up followed by a modest decline in profitability that reflects both operational headwinds and strategic shifts within its Chicago suburban franchise. Net income increased from approximately $67.4 million in 2022 to peak at $91.7 million in 2023 before slipping back to $85.3 million in 2024 and further declining to $80.3 million in 2025—a contraction of about 5.8% year-over-year [F1]. This softer income performance correlates with shifts in loan growth patterns and deposit dynamics.

The bank’s loan portfolio is notably concentrated geographically within Cook, DuPage, Will, Kane, Kendall, DeKalb, and LaSalle counties surrounding Chicago [S9]. It maintains diversification across commercial real estate owner-occupied/non-owner occupied loans, residential mortgages including HELOCs, construction loans, and consumer lending categories like powersport financing. No single economic sector accounts for a material concentration exceeding regulatory risk thresholds.

Deposit stability anchors Old Second’s moat as it retains a core deposit base that underpins liquidity and interest expense management [S1]. However, net deposit outflows totaled approximately $404 million during 2025—more pronounced than prior years—which exerted pressure on financing cash flows despite offsetting increases in short-term borrowings [S10]. The bank’s income is thus sensitive to shifts in deposit behaviors driven by regional economic conditions.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 80 | 122 | 5 | -5.8% |

| 2024 | 85 | 132 | 11 | -7.0% |

| 2023 | 92 | 116 | 12 | +36.1% |

| 2022 | 67 | 97 | 4 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 7 | 118 | 9.0 |

| 2024 | 1 | 121 | 12.7 |

| 2023 | 1 | 104 | 15.9 |

| 2022 | 0 | 93 | 14.6 |

Source: SEC companyfacts cache [F1].

Table: Historical Financial Summary FY2022–FY2025 reflecting net income stabilization amid evolving cash flows and capital expansion [F1]

Economic Landscape Impacting Regional Lending and Deposit Growth

Illinois’ protracted fiscal difficulties manifest as significant systemic risks for Old Second Bancorp's localized market approach [S13]. Statewide budget deficits raise the threat of tax hikes or business relocations that could depress borrower credit quality or dampen loan demand in the company’s lending zones.

Credit provisioning becomes increasingly important as borrower defaults or delinquencies could stress the allowance for credit losses (ACL). Collateral impairment risk also looms given real estate comprises roughly two-thirds of the loan portfolio mix at year-end latest filings [S20]. The economic environment – marked by inflationary pressures, unemployment variances, geopolitical tensions impacting markets globally – juxtaposes with Illinois-specific headwinds creating a complex scenario for sustained asset quality.

Removing geographic diversification amplifies sensitivity to localized downturns that may inflate nonperforming assets or constrain origination pipelines despite moderate economic recoveries nationally:

- Increased delinquency ratios would necessitate heightened ACL adjustments.

- Real estate valuation declines could impair loan recoveries upon default.

- Consumer spending shifts tied to inflation influence demand for retail banking products.

Capital Structure Evolution: Borrowings, Equity Infusion, and Regulatory Considerations

Old Second Bancorp has expanded its shareholder equity materially through acquisition-driven capital infusions: equity rose nearly $225 million year-over-year from approximately $671 million at end-2024 to nearly $897 million at end-2025 per consolidated statements [F1]. Such growth aligns with specific deals including the Bancorp Financial acquisition which brought both loan assets and associated liabilities onto the balance sheet [S10].

Borrowing activity illustrates greater leverage deployment concentrated via Federal Home Loan Bank of Chicago (FHLBC) advances—rising short-term borrowings from roughly $20 million at December 31, 2024 to $215 million one year later—with total available borrowing capacity at FHLBC near $987 million backed by approximately $1.50 billion pledged collateral across loans and securities portfolios [S4][S5][S19]. Important details include:

- Membership stock holdings at FHLBC increased significantly to over $11 million.

- Subordinated notes totaling around $60 million carry fixed rates transitioning post-April 15, 2026 to floating rates linked quarterly to term SOFR plus margin—a key factor for interest expense forecasting amid rate volatility [S5].

Regulatory compliance mandates maintenance of minimum risk-based capital levels inclusive of stress testing considerations factoring concentration risks inherent in localized operations.

Liquidity Management Practices: Stress Testing, Funding Diversity, and Contingency Lines

A hallmark of Old Second Bancorp’s financial stability is its rigorous liquidity framework linking quarterly contingency funding stress tests with monthly reviews feeding into board oversight every quarter [S1][S12]. These assessments model key liquidity risk events aggregating results bank-wide to ensure preparedness against market disruptions.

Funding sources are notably diversified beyond core deposits:

- Undrawn correspondent bank line of credit valued at $30 million ready for immediate use though unused since early 2019.[S5]

- Unencumbered securities available-for-sale portfolio exceeding $410 million providing liquid collateral.[S12]

- Overnight advances from FHLBC supplemented occasional funding requirements especially during deposit outflow periods.[S10]

Disciplined limit setting on short-term repurchase agreements secured by government-sponsored agency collateral further buffers against liquidity shocks enabling smooth operational continuity amid competitive pressures.[S4]

Shareholder Returns: Dividend Policy and Accelerated Buybacks in Context

Dividend payments continue consistently despite earnings fluctuations; while recent dividend amounts are not detailed explicitly beyond historical data dating back several years [F1], dividends remain part of the capital return framework.

Share repurchases accelerated notably with approximately $7.4 million executed during fiscal year 2025 under a newly authorized repurchase program capped at about $43.9 million following Federal Reserve nonobjection granted January 8, 2026 [S3][N6][F1]. Prior years showed much smaller buyback volumes indicating strategic scaling up intended to optimize capital use amid moderate income contractions.

Return on equity approximates nine percent based on latest annual net income relative to expanded shareholders’ equity—offering perspective on profitability aligned with ongoing capital expansion supporting operational growth objectives [F1].

Technology Adaptation and Competitive Position: Challenges from FinTechs and Large Banks

Operating as a community bank centered on western Chicago suburbs exposes Old Second Bancorp to intense competition not only from regional peers but also large national banks with advanced technology platforms alongside agile FinTech entrants innovating digital customer engagement models [S14].

While specific strategic initiatives regarding technology investment are not disclosed publicly,[S1] internal priorities likely focus on digitization of payment systems, online lending platforms, and data analytics capabilities necessary to meet evolving customer demands and counterbalance non-bank service offerings.

Strategic Outlook: Assessing Growth Drivers Amid Regulatory and Market Constraints

Growth prospects hinge on measured expansion within its core Chicago suburban franchise bolstered through selective acquisitions but remain tempered by regulatory requirements mandating robust capital buffers including liquid securities holdings against concentration risks [S13][N1][N2]. Q4-2025 earnings beat consensus estimates reflecting execution discipline yet highlighted caution due to economic uncertainties impacting borrower payment capacity and new loan demand trends[S2][N1]. State fiscal challenges combined with increasing regulatory scrutiny suggest operating constraints that may limit rapid scaling absent further capitalization or geographic diversification moves.

What to Watch: Upcoming Earnings Milestones, Repurchase Execution and Macro Signals

Key upcoming milestones include Q1-2026 earnings expected shortly which may update shareholders on loan loss provisions reflecting seasonal payment patterns as well as performance under shifting Federal Reserve rate policies affecting subordinated note resets[S3][N4]. Repurchase program progress will be closely monitored given recent approval enabling tactical open market timing potentially enhancing per-share value metrics amid constrained organic earnings growth[S3][N6]. Macro indicators such as Illinois regional GDP growth reports, local employment trends impacting borrower pools, and federal monetary policy directions remain critical variables influencing loan demand elasticity alongside interest margin dynamics[N1][N2]. These factors collectively define Old Second Bancorp’s operational landscape requiring vigilance toward competitive incursions or adverse regulatory developments.

This analysis is based solely on publicly available SEC filings, recent news releases, and verifiable company-reported financial data as of February 26, 2026; no forward-looking guidance was extrapolated beyond documented disclosures or verifiable investor communications.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments