Oak Valley Bancorp: Regional Commercial Real Estate Bank Navigating Local Dynamics and Market Concentration

Oak Valley Bancorp operates a focused regional banking model centered on commercial real estate lending in California’s Central Valley and Eastern Sierras, balancing growth with geographic and sector concentration risks.

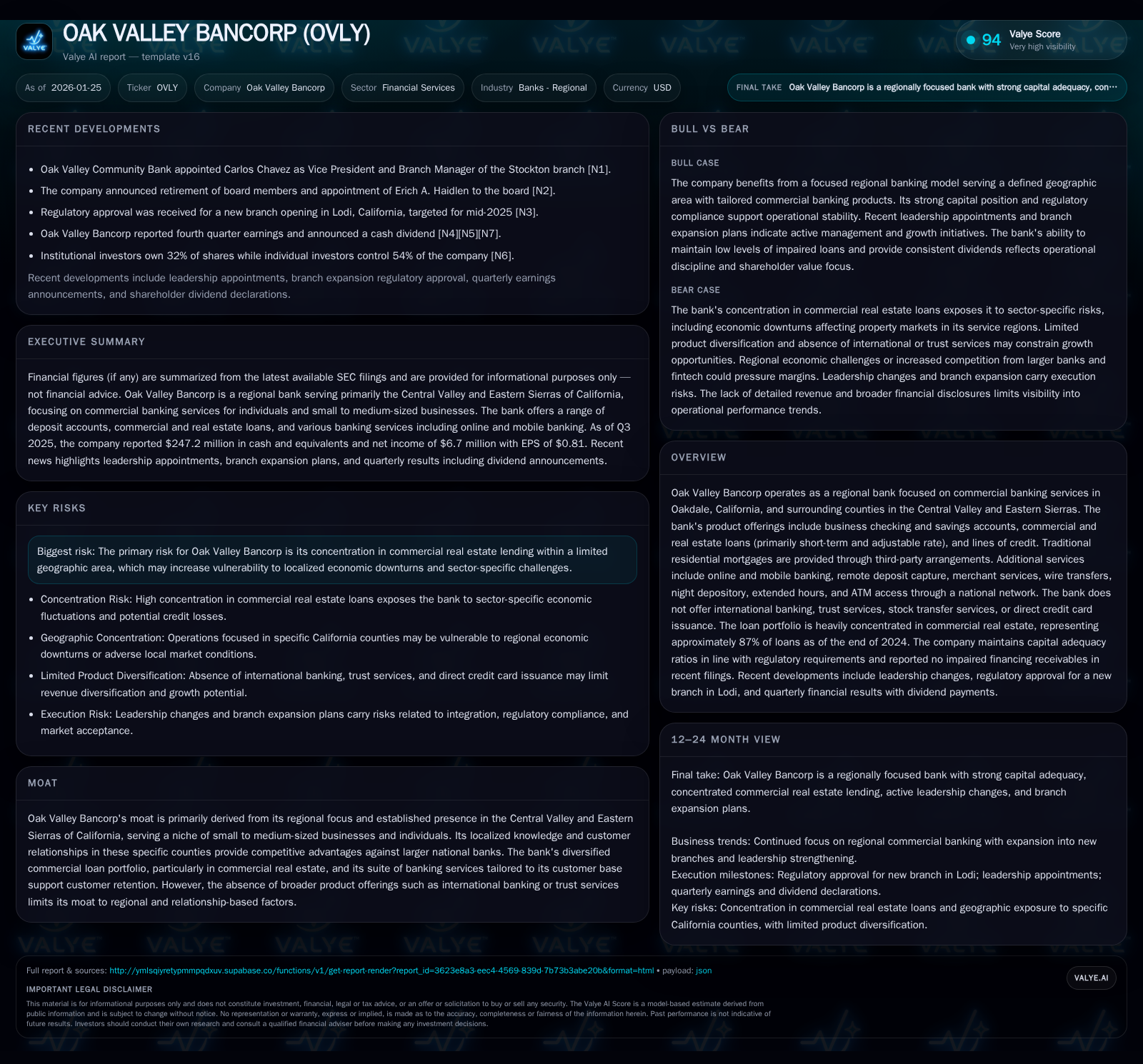

Oak Valley Bancorp (NASDAQ: OVLY) remains a regional commercial bank with a concentrated loan portfolio primarily in commercial real estate across several California counties. Recent developments include stable Q4 financial results, leadership changes, and branch expansion plans, reflecting ongoing efforts to deepen local market penetration. The bank’s business model revolves around serving small to medium-sized businesses with tailored commercial banking products, but its heavy reliance on commercial real estate loans within a limited geography poses notable risk amid evolving macroeconomic and regulatory conditions.

What Changed Recently

Oak Valley Bancorp reported its Q4 2025 earnings with steady net income, continuing its trend of consistent financial performance. The company declared a cash dividend, underscoring a commitment to returning capital to shareholders amid a competitive regional market [N1, N2, N3]. Leadership adjustments include the appointment of Carlos Chavez as Vice President and Branch Manager of the Stockton branch, signaling a managerial push to deepen regional customer relationships and possibly improve branch-level execution [N4, N8]. Additionally, there were retirements on the board and the appointment of Erich A. Haidlen, reflecting governance renewal [N5].

Strategically, the bank secured regulatory approval to open a new branch in Lodi, projected for mid-2026, expanding its physical presence in key Central Valley regions [N6]. This move complements organic growth efforts focused on local small to medium-sized businesses.

Business Model as a System

Oak Valley Bancorp functions primarily as a regional commercial bank serving Oakdale, California, and neighboring counties in the Central Valley and Eastern Sierras. Its core offerings include business checking and savings accounts, commercial and real estate loans, and lines of credit. Notably, the bank’s loan portfolio is heavily weighted towards commercial real estate, which comprises approximately 87% of total loans as of year-end 2024 [S7]. These loans are mostly short-term or adjustable-rate, catering mainly to local businesses and property owners.

The bank does not extend into international banking, trust services, stock transfer, or direct credit card issuance, instead opting for a focused product set that serves regional clients’ core commercial banking needs [S2]. Residential mortgages are offered only through third-party arrangements, keeping the bank’s balance sheet less exposed to residential real estate risk.

Digital offerings include online and mobile banking, remote deposit capture, and ATM access through a national network, facilitating customer convenience without the need for extensive branch expansion [S2]. Merchant services, wire transfers, night depository, and extended branch hours augment the commercial banking suite, catering to the operational needs of local businesses.

The bank’s localized focus allows it to leverage intimate knowledge of its service regions, including counties like Stanislaus, San Joaquin, Tuolumne, Sacramento, Placer, Inyo, and Mono. This geographic concentration brings both competitive advantages in customer relationships and risks tied to local economic conditions [S7].

Industry Map & Competitive Battlefield

The regional banking industry in California’s Central Valley is characterized by a mix of community banks, regional players, and branches of larger national banks. Oak Valley Bancorp occupies a niche as a focused regional lender with deep local relationships, particularly with small to medium-sized commercial clients.

Competition arises from larger banks offering a broader array of products and more extensive branch networks, as well as from fintech entrants targeting commercial banking with technology-driven solutions. However, Oak Valley’s moat rests on its regional expertise, personal service, and tailored lending products catering to the unique needs of Central Valley businesses.

The reliance on commercial real estate lending is both a differentiator and a vulnerability. Competing banks may spread risk across more diversified portfolios or focus on consumer segments, while Oak Valley's specialization may attract borrowers seeking local knowledge and flexible loan structures.

Regulatory oversight from the California Department of Financial Protection and Innovation (DFPI), Federal Reserve Board (FRB), and FDIC adds complexity and operational costs, common across the banking sector [S19]. Compliance with fair lending laws, privacy protections (including Gramm-Leach-Bliley Act provisions), and environmental regulations related to real estate foreclosures further shape the competitive landscape.

Where the Economics Become Real

Oak Valley Bancorp’s unit economics hinge on net interest margin generated from its loan portfolio. Interest income primarily derives from commercial and real estate loans, which are mostly short-term or adjustable rate, allowing the bank to reset yields in response to interest rate changes [S2, S7]. Interest expense reflects the cost of deposits and other borrowings.

The bank’s interest expense rose materially in 2024 compared to 2023 (approximately $12.86 million vs. $4.86 million), suggesting margin compression or a response to a higher interest rate environment [S13]. Maintaining attractive spreads between loan yields and deposit costs is critical.

Operating expenses include legal fees, which increased modestly, indicating ongoing regulatory and operational costs [S5]. The bank’s capital adequacy ratios comply with regulatory minimums, with Tier 1 leverage capital requirements around $77 million, supporting a stable capital base [S14, S15]. Cash and cash equivalents stood near $247 million as of Q3 2025, providing liquidity buffers [XBRL].

Growth economics depend on deposit gathering capacity and loan origination throughput in the bank’s core markets. The approved Lodi branch opening suggests management sees opportunity to deepen deposit and loan penetration. However, geographic concentration means economic downturns in the Central Valley or commercial real estate sector shocks could quickly impair loan performance, increasing credit risk and provision expenses.

Technology investments underpin digital banking offerings, but cybersecurity remains a material risk. Operational continuity and data protection are essential given the reliance on information systems for customer relationships and regulatory compliance [S6].

Diligence Questions / Disconfirming Signals

- How does Oak Valley Bancorp manage credit risk concentration given 87% of loans are commercial real estate in a limited geographic footprint? What is the current level of nonperforming loans or special mention credits in this segment?

- What are the detailed terms and amortization schedules of the adjustable-rate commercial real estate loans? How sensitive is the loan portfolio to rising interest rates and potential borrower stress?

- Given the lack of direct credit card issuance and trust services, how does the bank plan to diversify revenue streams or deepen wallet share with existing clients?

- How effective are the bank’s digital banking platforms in attracting and retaining younger, tech-savvy customers versus traditional branch-dependent clients?

- With branch expansion in Lodi and management changes in Stockton, what are the expected impacts on customer acquisition costs, operational expenses, and cross-selling opportunities?

- Has Oak Valley Bancorp faced any environmental remediation liabilities related to foreclosed properties, and what provisions are in place to manage such risks?

- What cybersecurity measures and incident history exist to assess technology risk exposure?

- How does the bank navigate regulatory compliance costs, and are there any pending regulatory actions or material changes anticipated?

- How stable and engaged is the shareholder base, considering the mix between institutional and retail investors?

Conclusion

Oak Valley Bancorp stands as a quintessential community-oriented regional bank with a concentrated focus on commercial real estate lending in California’s Central Valley and Eastern Sierras. Its recent financial results, leadership shifts, and strategic branch expansion reflect efforts to solidify and grow its local market presence. The bank’s moat is relationship-driven and geographic, but the heavy concentration in commercial real estate and limited product diversification pose inherent risks. Understanding how the bank manages credit and operational risks amid evolving economic, regulatory, and technological landscapes remains key to assessing its resilience and growth potential.

This analysis is based on publicly available information as of January 2026 and is not investment advice.

Comments