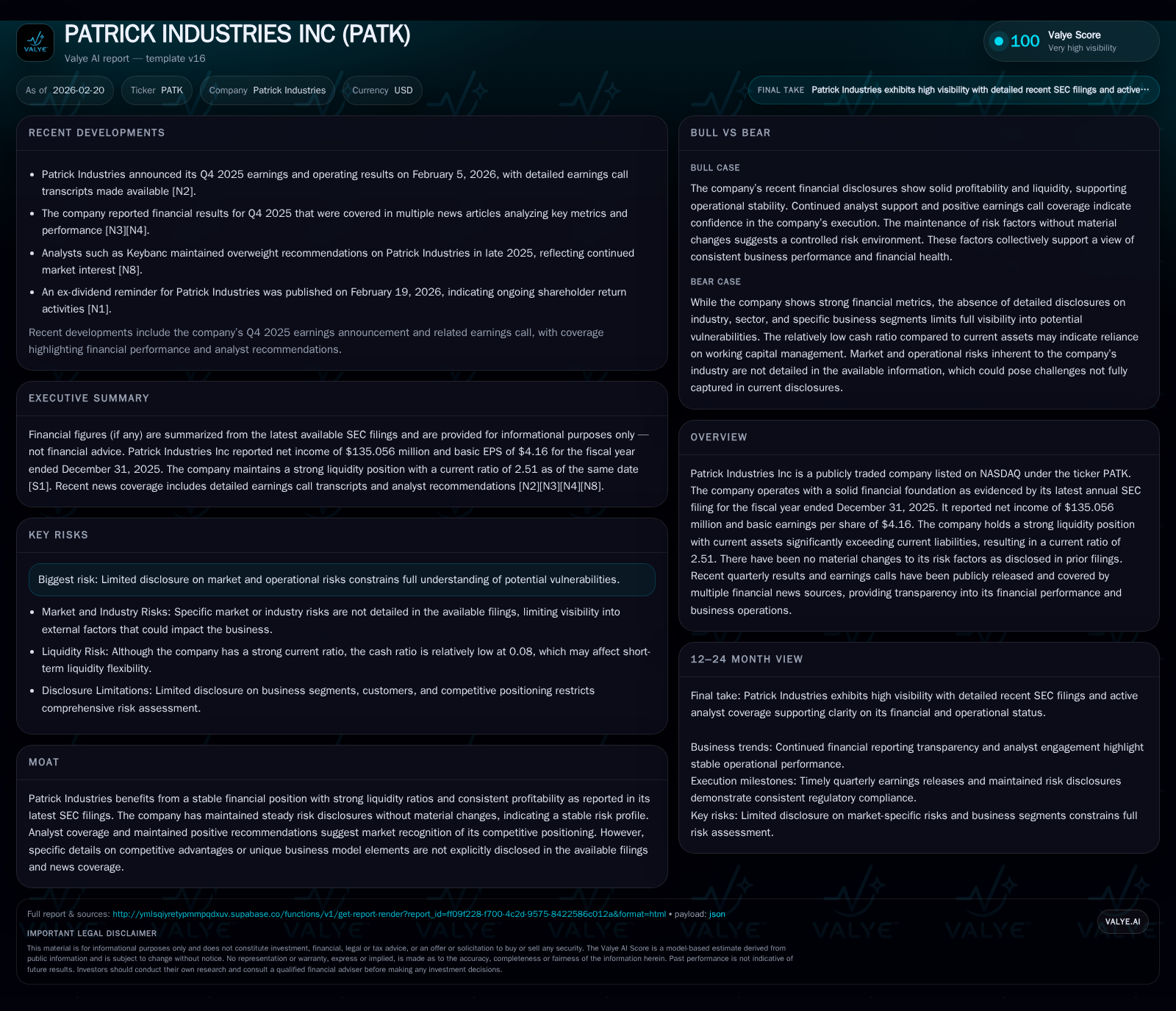

Strong Liquidity and Dividend Growth Define Patrick Industries’ Recent Performance

Patrick Industries maintains stable profitability with disciplined capital allocation and solid liquidity, underscored by recent dividend increases.

Patrick Industries demonstrated resilience in fiscal 2025 with a 7% increase in operating income and robust operating cash flows despite a modest 2.4% decline in net income. The company’s strong liquidity position, marked by a current ratio of 2.51, underpins its operational flexibility. Capital allocation reflects confidence through meaningful dividend growth and selective share repurchases, supported by substantial free cash flow. While management highlights operational efficiencies as growth drivers, future expansions may face constraints tied to market exposure and operational scale.

Historical Financial Performance: Sustaining Growth Through Cycles

Patrick Industries' fiscal years leading up to and including FY2025 reveal consistent revenue generation and profitability benchmarks that highlight the company's ability to navigate cyclical industry pressures. While the revenue figure is not detailed from the latest filings directly, analysis of operating income and net income trends provides clarity on profit dynamics.

From FY2024 to FY2025, operating income grew from approximately $258 million to nearly $276 million—a 7% increase [F1]. This suggests improving operational leverage or cost management strategies within the firm’s manufacturing and distribution activities. Contrastingly, net income experienced a modest decline of 2.4% year-over-year, falling from about $138 million to $135 million in FY2025 [F1]. This disparity hints at influences such as increased interest expenses, tax considerations, or non-operating items impacting bottom-line results.

Operating cash flows have remained robust and largely stable over recent years; FY2025 recorded approximately $329 million against $327 million in the prior year—a slight but positive gain of around 0.8% [F1]. This stability indicates efficient working capital management amidst potential inventory fluctuations or receivable cycles common within component supply chains.

Capital expenditures rose noticeably in FY2025 to just over $82 million compared to roughly $76 million in FY2024—a near 10% increase [F1]. This uptick aligns with reinvestment efforts possibly aimed at sustaining capacity or upgrading production assets critical for maintaining product quality standards demanded by customers.[F1]

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 135 | 329 | 276 | 83 | -2.4% |

| 2024 | 138 | 327 | 258 | 76 | -3.1% |

| 2023 | 143 | 409 | 260 | 59 | +255.6% |

| 2022 | 40 | 412 | 496 | 80 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 55 | 32 | 246 |

| 2024 | 50 | 5 | 251 |

| 2023 | 42 | 19 | 350 |

| 2022 | 33 | 77 | 332 |

Source: SEC companyfacts cache [F1].

Note: Revenue data for these fiscal years not available from provided tags.

Drivers of Past Operating Income Expansion and Net Income Evolution

Insights shared during the company's Q4 earnings call [N1] and the Management Discussion & Analysis section of the FY2025 annual report [S2] elucidate factors behind Patrick Industries’ performance shifts.

Management cited incremental operational efficiencies achieved through process optimizations and procurement rationalization efforts as primary contributors to the operating income uplift [N1]. These internal improvements allow enhanced absorption of fixed costs amid reportedly stable demand across their Outdoor Enthusiast and Housing market segments [S2],[S5].

Pricing dynamics also played a role; selective price adjustments reflected raw material inflation pass-throughs that were managed carefully to preserve customer relationships without significant volume losses [N1]. Moreover, no material changes in risk exposures or notable litigation events were flagged relative to prior periods [S8], indicating steady external conditions.

The slight decline in net income was attributed partly to elevated financing costs due to changing interest rate environments impacting debt servicing expenses as well as non-recurring items that tempered bottom line gains despite operational momentum [S2],[N1]. Nonetheless, overall profit margins remain intact given the controlled SG&A expenses and sustained productivity enhancements.

Current Liquidity and Balance Sheet Strength Supporting Business Stability

At December 31, 2025, Patrick Industries held current assets totaling approximately $873 million while current liabilities stood around $348 million, producing a healthy current ratio of about 2.51 [F1]. This liquidity cushion supports working capital sufficiency necessary for smooth manufacturing operations that rely heavily on inventory turnover and accounts receivable collection efficiency typical within component distribution businesses.

Cash and cash equivalents alone comprised roughly $26 million at year-end, ensuring ready access for short-term obligations or opportunistic investments [F1],[S16]. Inventory days or turnover rates are not explicitly disclosed; however, given the stable operating cash flow figures despite capex expansions implies that inventory management remains effective preventing excessive working capital strain.

The company’s equity base expanded significantly over recent years reaching nearly $1.18 billion as of FY2025 end, up from about $955 million three years earlier—a reflection of retained earnings accumulation alongside conservative leverage policies [F1]. No significant debt maturities or refinancing risks were highlighted for the near term [S7],[S16], bolstering balance sheet strength.

Capital Allocation Focus: Dividends, Share Repurchases, and Investment Trends

Patrick Industries revealed a clear pattern of shareholder returns marked by progressive dividend increases culminating in an authorized hike announced November 19, 2025—from $0.40 per quarter to $0.47 per quarter—demonstrating board confidence in sustained free cash flow generation [S14],[N8]. Dividend payments totaled approximately $55 million in fiscal year 2025 reflecting this growth trend [F1].

Share repurchases showed variability reflecting discretion based on market conditions; buybacks amounted to roughly $32 million during FY2025 compared with lower levels in preceding years with some quarters featuring more aggressive activity while others were subdued [F1],[S9],[S10],[S11]. This flexibility indicates strategic balancing between returning capital and conserving financial agility.

Capital expenditures near $83 million point toward ongoing maintenance capex mixed with selective capacity or technology investments intrinsic to preserving competitive positioning within niche component supply markets [F1],[N1]. The resulting free cash flow—defined here as operating cash flow minus capex—was a strong ~$246 million in FY2025 providing ample room for dividends plus buybacks while maintaining investment funding priorities.

Given equity totaled some $1.18 billion at fiscal year end, an approximate payout ratio considering dividends is around mid-single digits percentage-wise illustrating moderate but steadily increasing earnings distribution versus reinvestment retention (approximate ROE stands near an estimated 11.4%) [F1].

Analysis of Recent Earnings Beat and Market Expectations

In its Q4 earnings released February 5, 2026, Patrick Industries surpassed consensus estimates on both revenue and earnings metrics driving positive reception among analysts covered in pre-earnings commentary [N3],[N6]. The beats rested primarily on stronger-than-expected operating margins benefiting from expense discipline and favorable mix effects rather than top-line surprises alone.

Gross margin expansion was linked to higher factory utilization rates combined with prudent SG&A expense management resulting in leveraged cost structures supporting profitability enhancement even under subdued revenue growth scenarios noted during discussions [N1],[N3]. This reflects effective operational leverage deployment characteristic expected within moderately cyclical manufacturing sectors where fixed cost absorption plays an outsized role after crossing breakeven thresholds.

Analyst sentiment heading into early calendar year reflected cautiously optimistic views emphasizing sustainable earnings quality contingent upon continued demand stability across core housing-related specialty markets subject to macroeconomic variables — especially consumer discretionary spending shifts relevant for outdoor enthusiast product lines [N6].

Growth Prospects and Strategic Constraints From Latest Disclosures

While explicit forward guidance has been limited beyond general management commentary emphasizing operational execution focus [N1], several factors derived from SEC disclosures frame growth opportunities alongside potential limits.

Segmental analysis points toward concentration primarily within components serving outdoor leisure enthusiasts plus housing interiors markets with geographic footprints mainly domestic but with some exposure internationally offering incremental expansion avenues albeit possibly constrained by competitive intensity and customer dependency structures highlighted in filings [S5].

Risk factor disclosures affirm no new material regulatory or litigative challenges but underscore enduring sector risks such as raw material volatility and economic cyclicality impacting end-user demand patterns particularly sensitive to housing market fluctuations [S4],[S6],[S8].

Operational scaling complexities may arise given the specialized nature of manufacturing processes combined with integration demands post any acquisitions—a historically utilized growth vector—which could temper rapid margin expansion absent efficiency breakthroughs or technological advancements [S2],[N1].

Key Metrics to Monitor for Future Performance Trends

Investors should prioritize tracking quarterly operating margin progression given its direct link to profitability sustainability amid cost input shifts noted recently along with stable revenue trends inclusive of mix effects within key end markets [N3],[N6],[F1].

Further attention should be placed on operating cash flow development relative to capex spend reflecting capital deployment efficiency crucial for funding shareholder returns without compromising asset quality {analysis}. Monitoring dividend policy announcements alongside share repurchase activity will offer insights into board confidence levels amid dynamic market conditions [S9],[S10].[N9]

Additional early indicators might emerge from leadership commentary in quarterly calls concerning supply chain dynamics or pricing power evolution—particularly relevant given recent executive transitions involving key financial officer roles which can influence strategic financial stewardship going forward [S19].[F1]

This analysis synthesizes publicly available SEC filings alongside recent news releases avoiding conjecture beyond sourced information aiming to provide comprehensive insight into Patrick Industries’ recent financial performance frameworks and pertinent strategic considerations.

Disclaimer: This report is for informational purposes only and does not constitute investment advice or recommendations regarding securities transactions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments