Pharma-Bio Serv’s Revenue Retreat and Recovery Signals Among Regulatory Consultants

Examining Pharma-Bio Serv’s recent revenue decline, operational losses, and capital allocation amid client concentration risks in the compliance consulting sector.

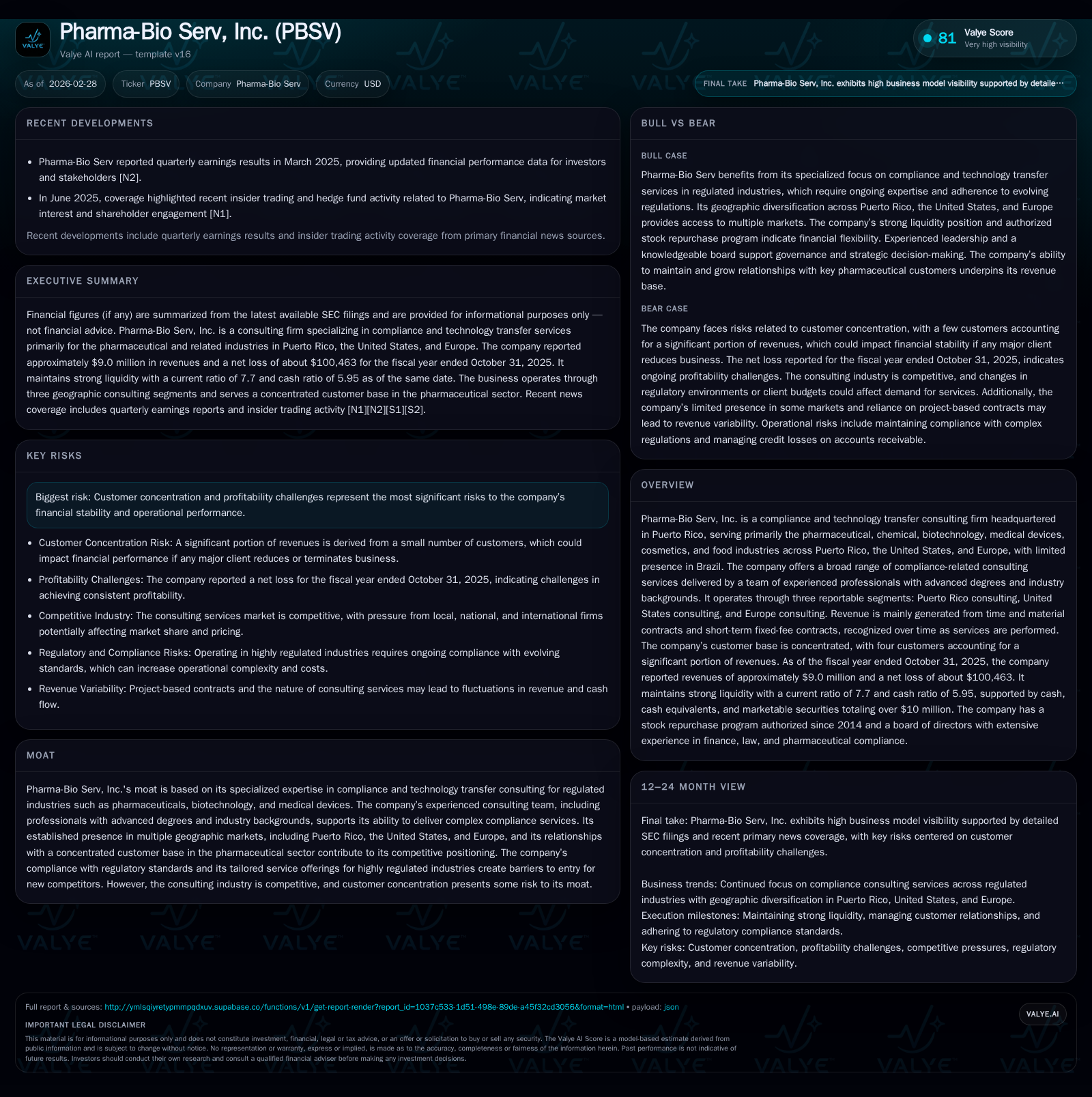

Pharma-Bio Serv, Inc. experienced a notable pullback in revenue in FY2025 after years of robust growth driven by its specialized technical compliance consulting across pharmaceutical and biotech industries in multiple geographies. Although top-line contraction of 5.3% accompanied operating losses, improvements from prior-year losses suggest early signs of margin stabilization. The firm's reliance on a concentrated client base remains a material risk factor alongside moderate capital return strategies emphasizing dividends despite profitability challenges. Going forward, segment performance disparities and external regulatory demands will shape recovery possibilities absent explicit guidance.

A Decade of Growth Meets Recent Revenue Challenges

Pharma-Bio Serv’s fiscal trajectory reveals pronounced growth peaks followed by retrenchment starting FY2023. Revenue reached $19.4 million in FY2022 before precipitous declines to roughly $17 million in FY2023 (down -12.5%) then further falling 5.3% in FY2025 to about $9 million [F1]. The Y-o-Y shrinkage stems partly from contract mix changes—majority time-and-material engagements characteristic of compliance consulting—and geographic disparities across Puerto Rico, U.S., and Europe segments [S4][S5][S6]. The Puerto Rico segment suffered the steepest contraction impacting overall consolidation while Europe showed some offset but remained relatively smaller.

This retreat interrupts an earlier expansion phase fueled by Pharma-Bio's deep specialization servicing regulated industries spanning pharmaceuticals to cosmetics with seasoned professionals holding advanced degrees [S12]. However, as regulatory projects often tied to client initiatives are discrete and project-based rather than continuous processes, revenue volatility is amplified [S5].

Historical performance (annual)

| FY | Rev ($mm) | Net ($) | CFO ($) | OpInc ($) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 9 | -100463 | -214886 | -637662 | -5.3% | +87.1% |

| 2024 | 10 | -777619 | -566701 | -1287587 | -44.0% | -159.4% |

| 2023 | 17 | 1310180 | 1890960 | 1117411 | -12.5% | +30.1% |

| 2022 | 19 | 1006684 | 592457 | 1174945 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($) | FCF ($) |

|---|---|---|---|

| 2025 | 2 | 31443 | -221530 |

| 2024 | 2 | 11263 | -726444 |

| 2023 | 2 | 34344 | 1883709 |

| 2022 | 3 | 81992 | 573188 |

Source: SEC companyfacts cache [F1].

Annual revenue reflects a sharp two-year downturn following peak activity.

Operating Profit Margins: From Historic Gains to Recent Losses

Operating income dynamics mirror revenue turbulence but depict gradual operational adjustment efforts. In FY2023, Pharma-Bio delivered positive operating income near $1.1 million, which deteriorated sharply into losses exceeding $1.28 million in FY2024 before narrowing again to a reduced loss of approximately $638K in FY2025 [F1][S2]. Net income swings correspond closely: positive $1.31 million in FY2023 gave way to losses that diminished by nearly 87% last year, down to an approximate $100K net loss [F1]. This oscillation underlines the susceptibility of consulting margins to topline contraction compounded by fixed SG&A overheads intrinsic to specialized staffing [S21].

Operating cash flow paralleled these trends with a positive $1.89 million inflow in FY2023 turning negative ($567K) in FY2024 then improving modestly but still negative at roughly ($215K) for FY2025 [F1]. Limited capital expenditures below $7K reflect a minimal asset-heavy footprint typical for service firms focused on human capital rather than equipment or infrastructure investments [S14][F1].

| Year | Operating Income (USD '000) | % YoY Operating Income Change | Net Income (USD '000) | % YoY Net Income Change | Operating Cash Flow (USD '000) |

|---|---|---|---|---|---|

| FY2022 | 1,175 | - | 1,007 | - | 592 |

| FY2023 | 1,117 | -4.9% | 1,310 | +30.0% | 1,890 |

| FY2024 | -1,288 | -215% | -778 | -159% | -567 |

| FY2025 | -638 | +50.5% | -100 | +87.1% | -215 |

Losses narrowed indicating steps toward operational leverage despite challenging market conditions.

Segment Performance Spotlight: Puerto Rico, U.S., and Europe Consulting Dynamics

Breaking down performance by geography reveals nuanced pressures within Pharma-Bio Serv’s triad reporting units [S4][S5][S6]:

- Puerto Rico Consulting remains the strongest revenue contributor historically but faced the largest decline during recent periods as local pharma manufacturing cycles shifted.

- United States Consulting showed relative stability though downtrend persisted amid contracting engagements.

- Europe Consulting, smaller by scale, delivered streaky results with some quarters evidencing higher gross margins albeit with pronounced revenue volatility.

Gross profit margins vary significantly across segments—U.S. operations sustain greater profitability percentages (31-36%), Europe peaks near ~47-52%, whereas Puerto Rico margins fluctuated lower (18-24%) over reported intervals [S21]. This suggests distinct operational efficiencies and client coverage that management must address strategically.

Customer Concentration: Revenue Driver and Risk Factor

Pharma-Bio Serv’s reliance on a concentrated customer base permeates risk considerations [S4][S5][F1]. Four clients account collectively for over 40% of total revenue and constitute nearly half the accounts receivable balance as of mid-FY25 (47%-55%). This concentration introduces pronounced counterparty credit risk compounded by the project-based nature of consulting contracts that may not renew predictably [S4]. Time-and-material contracts dominate service arrangements (>99%), emphasizing billable hours but also exposing revenues to project timing shifts.

The firm maintains credit loss allowances based on historic collection experience without significant write-offs recently, though one litigated receivable accounted for a substantial allowance set since 2021 [S7]. While high specialization limits new entrants due to regulatory barriers and technical know-how requirements, this client dependency necessitates vigilance regarding churn or contract renegotiations that could disproportionately impact results.

Capital Allocation Strategies Supporting Shareholder Returns

Despite operating losses, Pharma-Bio prioritizes consistent shareholder returns via cash dividends hovering near $1.7 million annually plus modest share buybacks (around $31K in FY25) reflecting sustained but cautious capital deployment policies [F1][S20][S26][S29]. Capital expenditure remains minimal (<$7K), underscoring little reinvestment in fixed assets consistent with consultancy services focused on intellectual capital rather than physical infrastructure.

This approach underscores a balancing act: returning excess cash where available while managing profitability headwinds—a somewhat atypical stance given persistent net losses but possibly geared at supporting shareholder confidence amid cyclical business flows.

Liquidity Standing and Balance Sheet Health

Pharma-Bio’s liquidity profile appears robust with current assets exceeding current liabilities by nearly eightfold (current ratio ~7.7x) as of late FY25 [F1]. Cash equivalents were reported around $6.8 million as part of current assets above $13 million supporting working capital needs comfortably.

Absence of significant debt obligations alongside conservative accounting for leases and provisions intimates a low financial risk posture appropriate for niche consulting operations where human resources dominate cost structures over leverage or capex intensiveness.

Future Outlook: Industry Trends and Company Constraints

Demand trajectories for compliance consultancy remain tethered closely to pharmaceutical regulatory environments which worldwide are tightening standards around manufacturing validation and technology transfer processes—a tailwind for firms like Pharma-Bio Serv possessing domain expertise and qualified personnel [S12]. However, the substantial concentration among few customers imposes ceiling constraints on organic growth potential given exposure if key clients reduce scope or shift suppliers.

Absence of explicit guidance or milestones from management amplifies importance on monitoring externally whether new regulations spur contract expansions or whether competitive pressures erode existing client relationships across continents where local regulatory nuances might affect engagement size.

What to Watch: Milestones and Performance Indicators

Upcoming performance will hinge on several critical indicators:

- Progress toward diversifying customer base beyond top four clients reducing concentration risk.

- Rebound or stabilization signals within Puerto Rico segment revenues which historically form nucleus of top-line.

- Sustained margin improvement signaling scalable consulting operations amidst fluctuating demand.

- Movement back toward positive operating cash flows facilitating reinvestment or enhanced distributions.

- Contractual mix evolution between time-and-material versus fixed-fee structures influencing revenue predictability.

- Any communicated strategic initiatives expanding presence within European or emerging markets such as Brazil.

Investors should undertake due diligence around trends in accounts receivable quality given high exposure concentrations coupled with watching EBITDA inflection points as harbingers for operational turnaround.

This report is based solely on information current as of February 28, 2026, drawn extensively from publicly available SEC filings including annual reports (10-K), quarterly updates (10-Q), and related exhibits without any additional company guidance or third-party forecasts noted within the public record at this time. Analysis provided aligns strictly with disclosed data absent extrapolation beyond provided metrics or speculation regarding future outcomes.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments