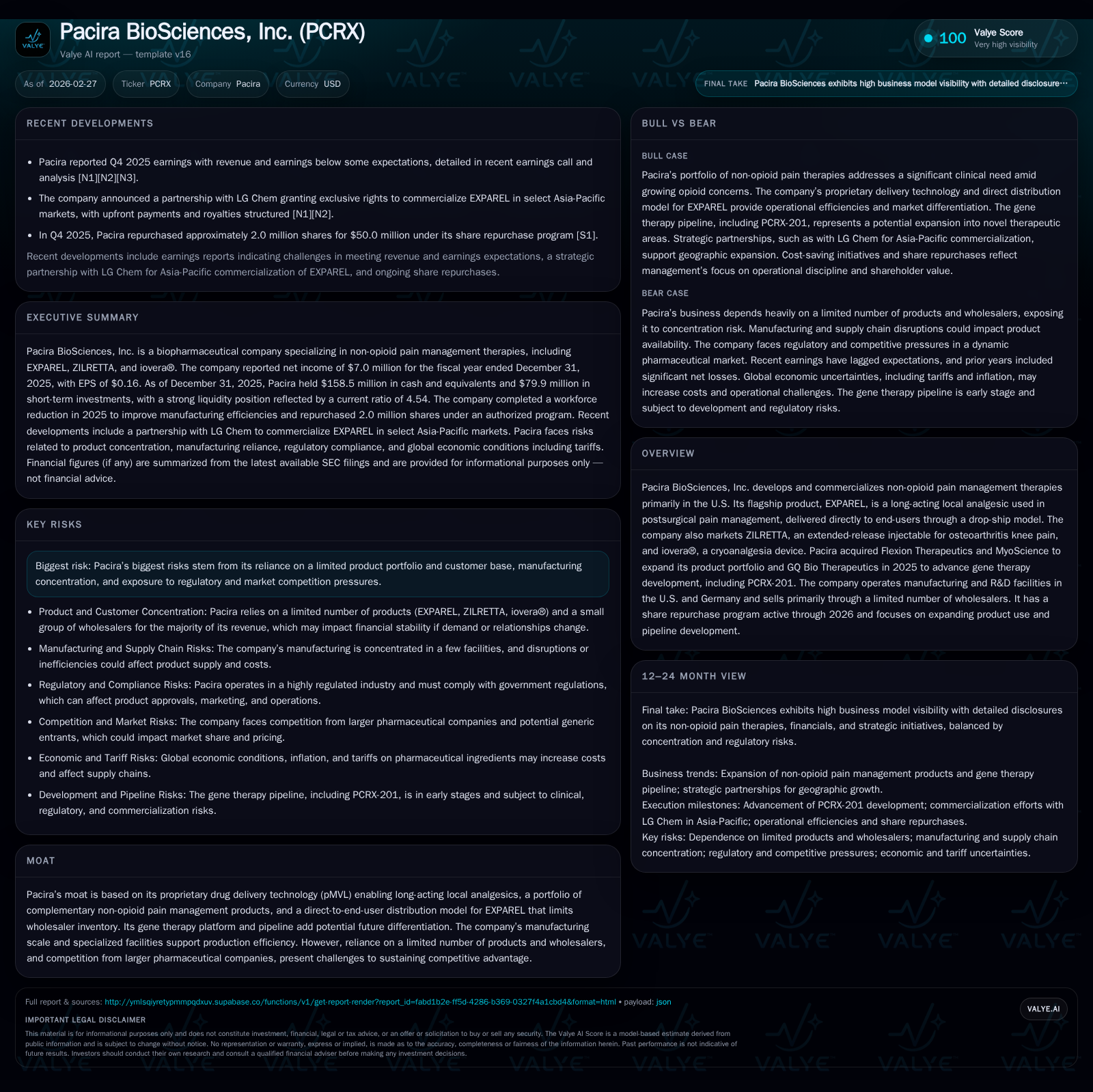

Pacira BioSciences Emerges From Profit Volatility With Robust Non-Opioid Portfolio Expansion

Pacira returns to profitability after a sharp loss, leveraging strategic acquisitions and non-opioid innovations while managing concentration risks.

Pacira BioSciences experienced significant earnings volatility between 2023 and 2025, swinging from operating losses in 2024 to modest profits in 2025 due to portfolio diversification and operational stabilization. The company expanded its non-opioid pain management offerings notably via acquisitions of Flexion Therapeutics, MyoScience, and GQ Bio Therapeutics, the latter advancing gene therapy development. Capital allocation reflects a robust buyback program alongside prudent debt management through refinancing efforts. Key risks remain in product and distribution concentration but are counterbalanced by proprietary drug delivery technology and expanding geographic reach through partnerships.

From Earnings Lows to Stabilization: Charting Pacira’s Recent Financial Trajectory

Pacira BioSciences confronted a dramatic earnings swing over recent years characterized by heavy losses followed by a cautious recovery. Revenue surged significantly from roughly $130.9M in FY2020 to an estimated level above $541M by FY2021 [F1], indicative of rapid commercial growth driven largely by its leading product EXPAREL. However, this momentum faced disruptions with operating income plunging from a positive $60M in 2022 to a steep loss of approximately -$73M in FY2024 before rebounding modestly to positive territory near $19M in FY2025 [F1]. Correspondingly, net income swung from positive figures ($15.9M in 2022) to a substantial net loss nearing -$99.6M in 2024, resuming profit with about $7M net income reported for FY2025 [F1]. This volatility depicts operational challenges possibly stemming from integration costs related to acquisitions along with pricing dynamics and competitive pressures.

Despite earnings fluctuations, operating cash flow exhibited resilience: Pacira generated approximately $152M CFO in FY2025 following stable inflows in FY2023 and FY2024 ($154.6M and $189.3M respectively) [F1]. Capex spending appears controlled at around $15.3M for FY2025, rising slightly from previous years but well below cash flow generation levels [F1]. This cash generation underpins the company's ability to sustain operations and invest in growth initiatives amid margin recalibrations.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 7 | 152 | 19 | 15 | +107.1% |

| 2024 | -100 | 189 | -73 | 11 | -337.3% |

| 2023 | 42 | 155 | 88 | 15 | +163.7% |

| 2022 | 16 | 145 | 60 | 30 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 148 | 137 | 1.0 |

| 2024 | 25 | 179 | -12.8 |

| 2023 | 139 | 4.8 | |

| 2022 | 115 | 2.1 |

Source: SEC companyfacts cache [F1].

Note: Percentage changes computed where sequential data is available; revenue YoY is particularly notable for explosive growth into early periods.

Expanding the Pain Management Frontier: Portfolio Moves Including Gene Therapy

Pacira’s repositioning strategy incorporates selectively targeted acquisitions that deepen its portfolio beyond its flagship EXPAREL franchise. Notably, the acquisition of Flexion Therapeutics brought ZILRETTA—an extended-release corticosteroid injectable targeting knee osteoarthritis pain—into the fold, diversifying the company’s therapeutic range . Complementing this was MyoScience acquisition enhancing cryoanalgesia capabilities via the iovera® device offering . In early 2025, Pacira acquired GQ Bio Therapeutics GmbH, which marked a foray into gene therapy leveraging HCAd vector platform development including pipeline asset PCRX-201 aimed at novel indications [N10].

These moves align with reducing overdependence on EXPAREL while capturing adjacent pain management segments powered by biotechnological enhancements, bridging device therapies with biologic modalities—a sector trend echoed among innovators seeking multi-front approaches against opioid reliance.

Non-Opioid Pain Therapies in Focus: Leveraging Technological Differentiation

Central to Pacira’s competitive moat is its proprietary pMVL (prolonged Multi-vesicular Liposome) drug delivery technology that enables formulation of long-acting local analgesics offering sustained postsurgical pain relief without opioids [S1]. This platform underlies EXPAREL’s efficacy profile delivering bupivacaine liposomes directly at surgical sites for prolonged analgesia up to 72 hours postoperatively.

Similarly, ZILRETTA utilizes extended-release injectable glucocorticoid technology targeting osteoarthritis pathology locally—lessening systemic side effects common with traditional corticosteroids—and iovera® offers non-pharmaceutical cryoanalgesia interventions leveraging nerve freezing techniques for pain control. These advanced formulations foster differentiated product cycles within procedural anesthesiology and chronic pain arenas where long duration effect and opioid alternatives form critical demand drivers.

Geographic Diversification via Partnerships: Asia-Pacific Market Access Strategy

Expanding beyond the U.S., Pacira announced a strategic commercialization partnership with LG Chem aiming at Southeast Asia markets including South Korea and select Asia-Pacific countries for distribution of EXPAREL [N7][N10]. This channel extension reflects carefully calibrated global market access aligning with regional demand for innovative post-surgery pain solutions while managing inventory risks endemic to wholesale distribution through direct end-user deployment models.

The partnership leverages LG Chem’s local regulatory expertise and sales infrastructure enabling more rapid penetration without heavy fixed asset commitments from Pacira itself—common practice among midsize biopharma seeking footprint expansion while retaining stewardship over stewardship over pricing and supply chain oversight.

Capital Structure and Cash Flow Strength: Navigating Debt and Liquidity with Share Repurchases

As of December 31, 2025, Pacira held cash and equivalents totaling roughly $158.5 million alongside current assets around $548 million versus current liabilities near $121 million yielding an attractive current ratio close to 4.5—highlighting ample short-term liquidity [F1].

The company enhanced financial flexibility through refinancing by retiring its Term Loan A ($98.8 million outstanding balance repaid mid-2025) via drawing on a new senior secured revolving credit facility sized at $300 million due July 2030 bearing variable interest based on leverage ratios between approximate spreads of 1.50%–3.25% over base rates or SOFR benchmarks [S4][S5][S6][S7]. This facility supports working capital and growth initiatives with covenant compliance confirmed as of fiscal year-end.

Capital return gained prominence via stock repurchase activities: In April 2025 management authorized up to $300 million share repurchase program replacing prior smaller authorizations; during calendar year '25 roughly $148 million was expended buying nearly six million shares at an average price near $24-$26 per share [F1][S8][S14][S15][S22]. Management retains discretion for timing balancing liquidity requirements amid no declared dividends historically or planned currently given reinvestment priorities [S15][S16].

Approximate ROE stands around a low single-digit rate (~1%) reflecting the company's transition phase from losses toward earnings stability juxtaposed against a sizeable equity base exceeding $693 million as of year-end '25 [F1]. Free Cash Flow remains robust given CFO minus capex approximates $137 million providing internal funding appetite.

Investor Lens: What to Watch in Upcoming Milestones and Product Launches

While Pacira refrains from issuing formal detailed forward guidance publicly recently [N2], investor focus should tune into quarterly earnings trends especially adoption curves for newer products like ZILRETTA and iovera® devices coupled with measurable progress on gene therapy pipeline candidates such as PCRX-201 currently under clinical investigation through the acquired GQ Bio platform [N6][N8].

Regulatory reviews constitute potential inflection points both for new indications approvals or patent litigations outcomes that might affect exclusivity periods notably those surrounding core patents protecting bupivacaine liposome formulations [S9][N1][N3]. Market dynamics including competitive incursions by generic manufacturers or larger pharmaceutical competitors will also merit scrutiny.

Geographic rollout efficacy tied to LG Chem partnership expansion success within Asia-Pacific defines another watch area considering regional reimbursement environments and provider adoption timelines.

Risks Rooted in Concentration and Competition: Manufacturing and Market Dynamics

Pacira faces concentrated risk exposures anchored by dependence on a narrow product suite dominated by EXPAREL sales combined with heavy reliance on a limited number of wholesalers operating under direct-to-end-user inventory models designed to limit stockpiling but increasing single points-of-failure vulnerability [S9][S18].

Manufacturing remains concentrated predominantly at their San Diego Science Center Campus alongside specialized R&D labs including German facilities serving gene therapy development efforts [S1]. Disruptions here could impair supply continuity.

Additionally, patent infringement lawsuits ongoing particularly against eVenus ANDA filers underscore pressing intellectual property defense expenditures casting uncertainty over future revenue capture duration especially as some volume-limited generic licenses commence around early next decade despite settlement frameworks mitigating immediate threats [S9][S23].

Market competition intensifies as larger pharmas develop competing non-opioid analgesics exploiting novel delivery platforms as well as biosimilar entrants potentially eroding market share over time representing structural margin pressures.

Disclaimer: This analysis is based solely on publicly available information provided through SEC filings ([F1],[S#]) and credible news sources ([N#]). It does not represent investment advice or recommendations but aims to deliver an informed perspective grounded strictly in reported data respecting compliance constraints.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments