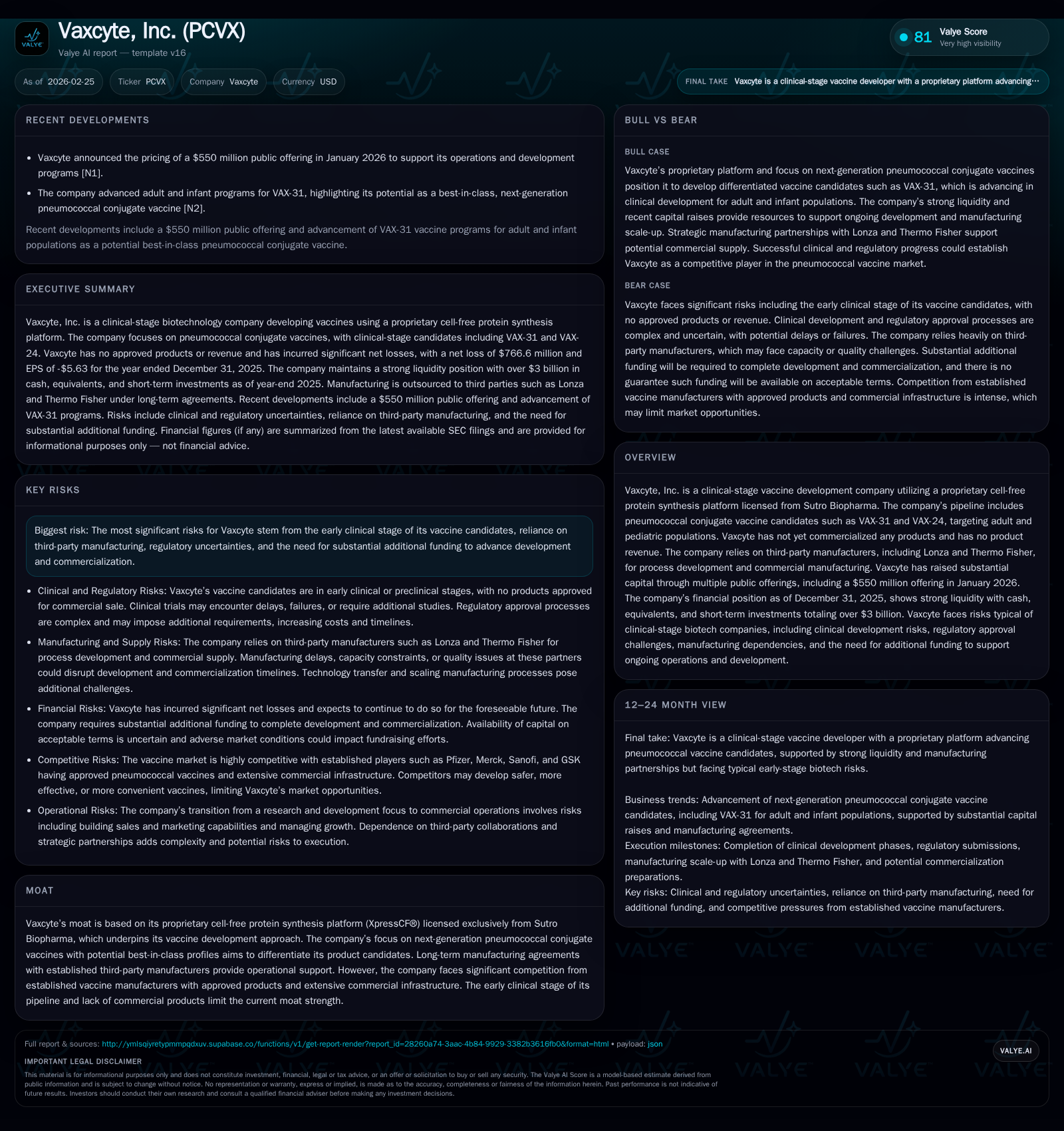

Vaxcyte’s Clinical Journey: Balancing Innovation and Financial Sustainability

Vaxcyte advances next-generation pneumococcal vaccines backed by proprietary technology amid heightened capital demands and clinical risks.

Vaxcyte, a clinical-stage biopharma focused on pneumococcal conjugate vaccines, is progressing through key Phase 3 trials leveraging its XpressCF® cell-free protein synthesis platform. Despite no product revenue to date, it has maintained strong liquidity, bolstered by a $550 million public offering in early 2026. The company faces substantial operating losses driven by R&D investments, reliance on third-party CMOs, and regulatory uncertainties. Near-term milestones like OPUS-3 trial dosing and potential BLA submissions will be critical to validate its growth trajectory.

From Lab to Clinic: Vaxcyte’s Growth Narrative

Vaxcyte has been on an aggressive development path since its inception, focusing nearly all resources on advancing its vaccine pipeline through preclinical and clinical stages. The company's operating income trajectory shows widening losses reflective of expanding research and development costs essential at this stage. Operating income deteriorated from -$232 million in FY2022 to -$924 million in FY2025, a cumulative increase exceeding 300%, with the most significant jump (62%) occurring between FY2024 and FY2025 [F1]. Net losses have followed suit, reaching -$767 million in FY2025 compared to -$223 million three years prior.

This steep escalation in losses illustrates Vaxcyte's commitment to accelerating clinical trials, manufacturing process development, and scale-up activities without any offsetting product revenue ([F1]). Operating cash flow remains deeply negative (-$656 million in FY2025), signaling persistent high cash burn typical for clinical-stage biotech developing complex biologics. Capital expenditures (though limited relative to R&D) increased from $5.8 million in FY2022 to around $13.7 million in FY2025 [F1]. The company’s ability to maintain liquidity amidst these demands rests on periodic capital raises supported by institutional markets.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -767 | -656 | -924 | 14 | -65.2% |

| 2024 | -464 | -453 | -570 | 22 | -15.3% |

| 2023 | -402 | -297 | -468 | 16 | -80.0% |

| 2022 | -223 | -171 | -232 | 6 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -669 | -28.5 |

| 2024 | -475 | -14.0 |

| 2023 | -313 | -32.4 |

| 2022 | -176 | -23.4 |

Source: SEC companyfacts cache [F1].

Note: Revenue data not available; dividends and share repurchases not reported in provided tags.

Pipeline Spotlight: Next-Generation PCV Candidates Driving Clinical Progress

Central to Vaxcyte’s value proposition is the XpressCF® cell-free protein synthesis platform exclusively licensed from Sutro Biopharma, enabling rapid antigen production with potentially improved immunogenicity profiles ([F1], ). Their current pipeline features pneumococcal conjugate vaccine (PCV) candidates designed to address unmet needs in adult and pediatric populations—primarily VAX-31 (adult/pediatric) and VAX-24 (pediatric) [N8].

Both candidates employ conjugate vaccine technology harnessing polysaccharide-protein conjugation strategies targeted against multiple pneumococcal serotypes—a standard approach among licensed PCVs but with differentiation sought via valency breadth and immune response durability [N7]. VAX-31 has advanced into the pivotal OPUS-3 Phase 3 trial dosing participants as of February 2026 [N3], marking a significant developmental milestone suggesting proximity to regulatory submission readiness.

The competitive landscape includes established players such as Pfizer, Merck, GSK, and Sanofi/SK Chemicals advancing higher-valent PCVs including recently approved PCV21 and PCV24 products ([S22]). Vaxcyte faces challenges demonstrating superior safety/efficacy profiles while addressing Chemistry Manufacturing Controls (CMC) expectations given their novel manufacturing processes [S27]. Nonetheless, their "best-in-class" objective could capture market share if successful.

Capital Infusions and Cash Burn: Funding the Development Race

Vaxcyte’s funding narrative reflects ongoing capital-intensive drug development dynamics typical for clinical-stage biopharmaceuticals without commercial products or revenues ([F1]). The company raised approximately $550 million through a public offering in January 2026 alone [N6], substantially bolstering their cash position which totaled over $3 billion when combined with cash equivalents and short-term investments at December 31, 2025 [F1]. This capital runway supports advanced clinical programs amidst significant quarterly operating outflows.

Despite strong liquidity buffers, operating cash flow burn remains a critical consideration; FY2025 CFO declined by ~45% year-over-year to nearly -$656 million highlighting aggressive resource deployment into R&D and clinical endeavors [F1]. Meanwhile, capex levels tapered compared to prior years yet remain material given facility support for manufacturing scale-up ($13.7 million in FY2025) [F1].

The sustainability of Vaxcyte's operations fundamentally hinges on continued equity financing or strategic partnerships given zero product revenue currently—a common hallmark for companies at this stage under regulatory review pressure ([S17]). Investors must balance optimism about upcoming data releases against dilution risk inherent in recurrent capital raises required for late-stage pipeline progression.

Manufacturing Partnerships and Operational Dependencies

Outsourcing vaccine production is standard for many biotech firms lacking internal large-scale GMP facilities; Vaxcyte relies principally on Lonza AG and Thermo Fisher Scientific as contract manufacturing organizations (CMOs) for process development plus commercial manufacture ([S1], [S19]). These alliances provide technical expertise but create operational leverage risks linked to capacity availability, quality controls, regulatory compliance burdens, and contractual obligations.

Non-cancelable purchase commitments toward CMOs approximate $585 million covering manufacturing services through at least end-2029 ([S1], [S7]). Termination risks involve hefty cancellation fees implying fixed-cost-like financial responsibilities even amidst uncertain product approval timelines or market launches.

While outsourcing mitigates upfront capital expenditure for wholly owned plants—key given the cash burn constraints—the dependency amplifies sensitivity to third-party execution challenges affecting supply continuity or incremental cost pressures amid scaling volumes.

Risk Landscape: Clinical, Regulatory, and Execution Challenges

Vaxcyte confronts multifaceted risks typical for vaccine developers evolving beyond discovery into costly late-stage trials ([S2], [S4]–[S6], ). Clinical-stage risk manifests via trial failures or delays impacting valuation materially; IP protection uncertainties pose challenges amid competitive patent landscapes with third-party infringement claims or invalidity disputes possible ([S18], [S26]).

Regulatory scrutiny particularly emphasizes Chemistry Manufacturing Controls (CMC), as highlighted by FDA precedent questioning novel platform-based manufacturing approaches that could delay marketing authorization ([S27]). Furthermore, ongoing compliance with extensive healthcare fraud-and-abuse laws alongside privacy mandates such as HIPAA/HITECH and GDPR imposes continuous governance burdens including cybersecurity oversight escalating incidents up to the board audit committee level ([S1]).

Additional risks extend toward reimbursement determination complexity within U.S./international markets where payor acceptance can dictate commercial success or failure; this compounds uncertainties around pricing strategy adoption post-approval ([S13], [S20]). Legal proceedings remain currently non-material but may incur unforeseen expenses if disputes arise ([S11]). Collectively these factors necessitate rigorous risk mitigation frameworks.

Roadmap Ahead: Key Near-Term Milestones and What to Monitor

While explicit guidance remains sparse (), several catalysts warrant close attention amid considerable investor scrutiny:

- Continued enrollment completion/dosing updates from OPUS-3 Phase 3 adult trial evaluating VAX-31 efficacy/safety endpoints will provide pivotal validation signals [N3].

- Anticipated BLA submissions during or following calendar year 2026 targeting initial U.S./EU registration pathways represent fundamental inflection points for transitioning from purely clinical developer status towards commercial readiness [N7].

- Phase advancement of pediatric-focused PCV candidates like VAX-24 will furnish additional pipeline depth supporting future growth avenues [N8].

- Regulatory feedback on CMC submissions critical for clearance indicating manufacturing scalability sufficiency given proprietary technology nuances.

- Monitoring how manufacturing partners execute contracted supply volumes vis-à-vis evolving global bioprocessing constraints. Given these pending events derive primarily from disclosed developmental activity without formal guidance issuance labeled forecasts are premature—the landscape remains heavily contingent on successful trial outcomes.

Financial Performance Snapshot: Losses, Liquidity, Equity Trends & Returns Metrics

The consolidated financial summary illustrates an expanding deficit profile with no commercial revenues recorded thus far while balance sheets demonstrate strengthened shareholder equity largely fueled by equity markets activity noted since FY2022:

Operating income loss accelerated from -$232 million (FY2022) to nearly quadruple by FY2025 (-$924 million), underscoring intensified R&D expense acceleration concomitant with pipeline advancement efforts ([F1]). Net loss widened similarly albeit at slightly lower absolute rate (-$767 million in FY2025).

Operating cash flow mirrors these trends revealing deeper negative cash generation reflective of outlays preceding product revenue realization (-$656 million latest year). Capital expenditures peaked mid-series before dipping slightly signifying steady plant/facility investment supporting CMOs ([F1],[S8]).

Stockholders’ equity increased materially mainly due to continuous equity financings—peaking near $3.3 billion before settling at approximately $2.7 billion at end-FY25—highlighting significant shareholder dilution offsetting retained earnings erosion caused by ongoing net losses resulting in an approximate negative return on equity near -28.5% ([F1]). Current ratio around ~7.9 affirms strong short-term liquidity cushion mitigating near-term default concerns despite heavy operational consumption.

Capital Allocation Review: Investment Focus Without Dividends or Buybacks

Explicit capital allocation policies confirm that no dividends have been declared nor share repurchases undertaken as of end-FY25 across reporting periods consistent with typical biotech norms prioritizing reinvestment into pipeline progression over shareholder distributions ([S7], [S12], [S15]). All available resources funnel toward sustaining extensive research & development programs including clinical trials financing plus strategic manufacturing capacities critical ahead of commercialization phases. Disclosed open market sale programs (ATM offerings) support flexible incremental funding sourced opportunistically amid volatile equity markets conditions enhancing treasury reserves or cushioning future cash flow gaps. This conservative payout posture reflects prudent stewardship acknowledging inherent risks attendant upon unproven late-stage assets awaiting market authorization outcomes that ultimately dictate firm valuation expansion potential.

This analysis synthesizes publicly available financial data alongside SEC filings and recent company disclosures without projecting future valuations or investment recommendations. Given Vaxcyte's early clinical-stage status coupled with volatile biotech dynamics its outlook remains subject to considerable variability dependent primarily upon clinical development success rates, regulatory agency interactions, competitive innovation pivots within pneumococcal vaccine space plus macroeconomic capital market conditions influencing funding accessibility.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments